With the S&P 500 showing triple digit returns since the financial crisis, we’ve noticed there have been more and more publications denouncing hedge funds as under performing the S&P 500. We even got in on the trend too, but in a slightly different way than most.

And in other news…oranges don’t taste like bananas RT @finalternatives: Hedge Funds Trail S&P 500 YTD https://t.co/Ch4d5a3RQH

— Attain Capital (@AttainCapital) May 13, 2014

The problem with saying hedge funds are underperforming the S&P 500 is that the grand majority of them aren’t even trying to beat the S&P 500 in returns, for any set period. They are trying to deliver better risk adjusted returns than the stock market, but that doesn’t make for as good of a headline. “Hedge funds post .026 better Sharpe ratio over trailing 36 month period” just doesn’t have that ring to it.

The problem is, as more and more hedge fund like products make it into so-called ‘liquid form’ via a mutual fund or ETF or the like; more and more everyday investors will be able to access them, and more and more websites and other portfolio tools which compare performance to stocks by default will be serving up the S&P 500 as the benchmark for the Alternative Funds performance. It turns out more than a few people are picking up on this apples and orange comparison, with Joe Light from the Wall Street Journal weighing in recently with his article “How Do You Measure the New ‘Alternative’ Funds?”

“If a fund intentionally hedges its exposure to stocks, it isn’t really fair to say that the fund did well in 2008 or poorly in 2013, says Jonathan Boersma, head of professional standards and a benchmarking expert at the CFA Institute. The problem is that it wasn’t really designed to beat the S&P 500 during up markets in the first place.”

So what should investors in Alternatives benchmark their investments against? Mr. Light has two key factors to look at before attempting to compare a hedge fund to anything.

“The first step: Figure out what you might have invested in instead. Another yardstick: What does the fund manager say his ultimate goal is?”

Once you know what’s under the hood of your hedge fund, and know the ultimate goal, there are many possibilities for a proper benchmark.

1. Measure against 0

Most hedge funds market themselves as “absolute return” vehicles, being able to make money in many different economic environments; and in the strictest sense of that phrase – the benchmark to use would be the 0% line. A positive gain. This is the sort of benchmarking a lot of investors do unknowingly, saying if the investment is making money (is up >0), it is doing well, and if not – it’s under performing – no matter what the stock or bond markets are doing.

2. Hedge Fund Indices

What about a hedge fund index? Yes, there are such things, and while they are plagued with complaints of survivorship, backfill, and other biases – they appear to act quite well as a benchmark for alternative investments in… you guessed it – hedge funds. We prefer the DJCS Hedge Index, which just happens to have multiple sub-indexes covering Emerging Markets, Event Driven, Long/Short Equity, Global Macro, and Managed Future; just to name a few.

3. Managed Futures Indices

You’ll see that managed futures is one of the listed hedge fund indices, and for those in the space we specialize in – it is more than a fair comparison to measure up your alternative investment in the managed futures space to the various managed futures indices. While they differ month to month and have different compositions, we’ve found the average of them to be quite consistent with the actual gains and losses seen in actual managed futures accounts of our clients. It’s also worth noting that there are sub indices here as well – where you can dive down and compare different styles with the short-term trader index, ag index, and trend following sub-index.

4. Commodity Index

It’s hard to get too far down the alternative investment spectrum without running into commodities – and comparing your alternative investment (especially if it is a commodity heavy managed futures investment or energy fund or the like) to one of the original alternative investments makes a lot of sense. You can get more granular here as well, with indices on energy, agriculture, and so forth – just be careful you’re not looking at an index of energy companies.

Now, comparing an investment to an index which is most similar to the strategy or you investment seems logical enough, but even then your investment is likely to be much more volatile (both on the upside and downside) than the index due to the index gaining the advantage of a smoothing effect by combining many managers. This makes it important to normalize the performance in some manner, which is where risk adjusted ratios come in:

1. Sharpe Ratio

The most popular risk adjusted ratio is the Sharpe. The Sharpe Ratio measures return over volatility. But as we’ve discussed, the largest issue of using volatility of returns, and more technically the standard deviation of returns, is that using such a calculation assumes a normal distribution of returns.

2. Sortino Ratio

Then there’s the Sortino ratio, which measures risk over both the upside and downside volatility.

3. Mar and Calmar Ratios

The Mar and Calmar Ratios measures Compound ROR over Max DD.

4. Sterling Ratio

The Sterling ratio is slightly different, which measures Compound ROR overage the average drawdown, instead of max drawdown.

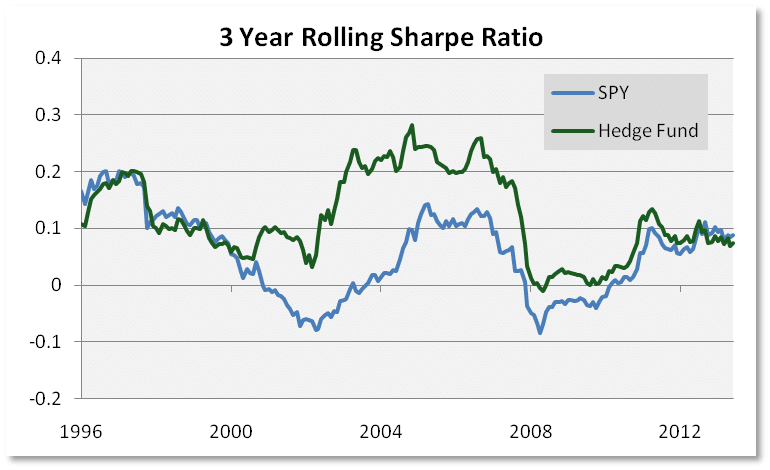

And just how do hedge funds look against the S&P when considering their normalized behavior – their Sharpe ratios? As joked about earlier – when you plot the rolling 3 year Sharpe ratio of Hedge Funds and the S&P 500, there isn’t the same sexy headline of hedge funds underperforming the S&P 500. They’ve been about the same lately, after being handily ahead for the better part of the 2000’s.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)Data: Hedge Fund = DJCS Hedge Fund Index SPY = S&P 500 ETF via Yahoo Finance

So the next time there’s an article claiming Hedge Funds (or other Alternative Investments) as underperforming the S&P 500, realize they are telling you that the Filet tastes meatier than the Salmon. The Salmon is half the calories and half the fat content… if it doesn’t taste as meaty – that’s usually on purpose.