If you haven’t had the chance to check out the work of Ben Carlson over on his blog, “A Wealth of Common Sense,” we highly suggest it. We’ve written about his thoughts and ideas a couple times (here and here) and we couldn’t help but notice the subject of his musings on doing what works for you in his latest post, “The Importance of Intellectual Honesty in the Markets” is of Managed Futures.

“Managed Futures is a trend following strategy that trades futures contracts both long and short depending on the direction of the markets. The strategies are typically diversified across stocks, bonds, interest rates, commodities and currencies and follow a systematic approach. Also called CTAs (commodity trading advisors), these funds got a ton of attention following the 2008 crash because they were one of the few places to earn positive returns when stock markets around the globe sold off anywhere between 35-55%.

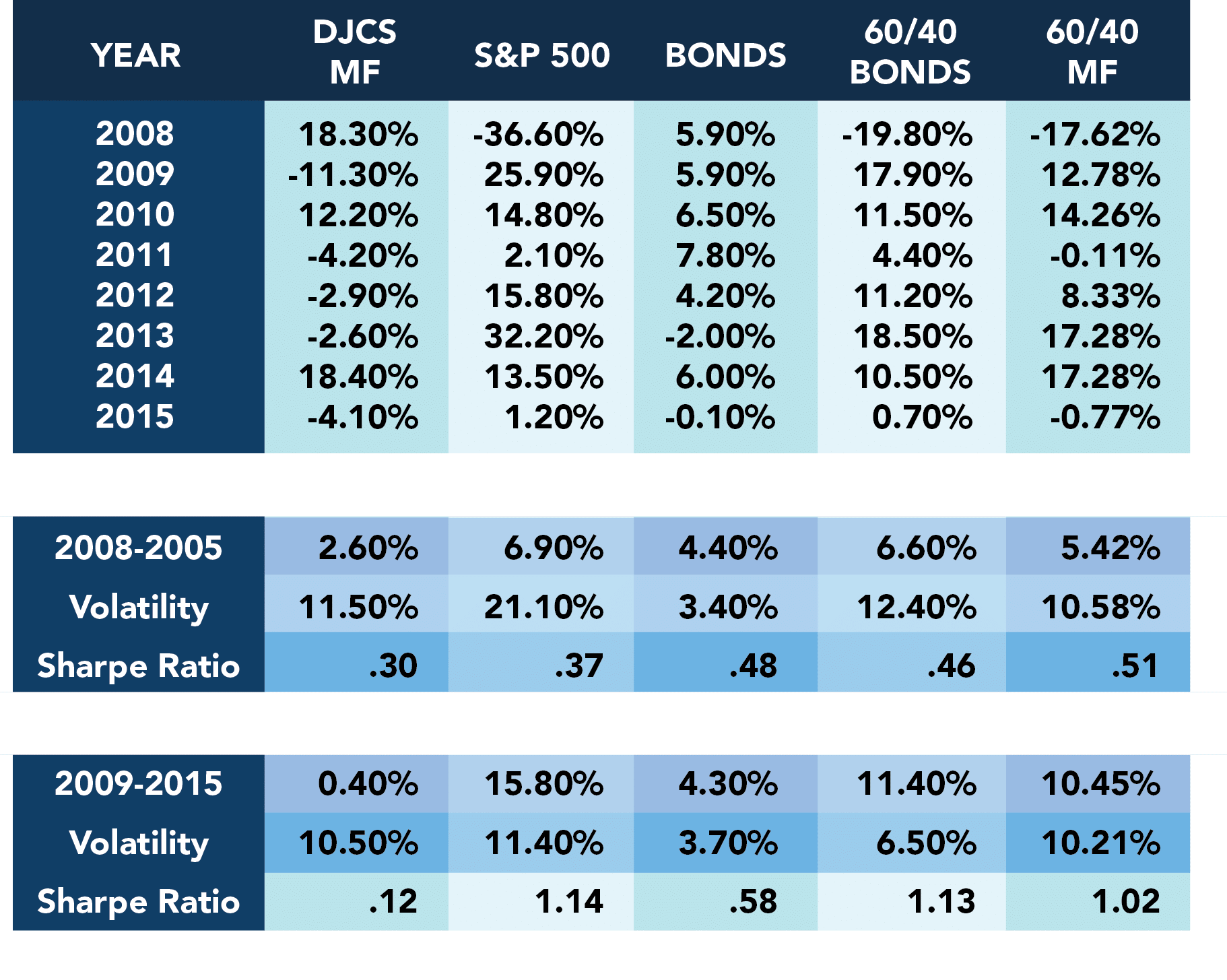

I looked at the Credit Suisse Managed Futures Index going back to 2008 and compared it to the annual returns on stocks, bonds and a 60/40 stock/bond portfolio through June of this year:

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: A Wealth of Common Sense

But it wasn’t just his feature of explaining the asset class of Managed Futures, it’s about how investors tend to chase performance, getting in at the highs and out at the lows. As Ben puts it:

“The biggest problem most investors face is that they invest in something like managed futures after they see the impressive results it had in 2008. Then they bail when it falters. Or they change their strategy to a low cost indexed buy and hold approach after seeing how well it’s done since 2009. Once again, many will bail during the inevitable down period.”

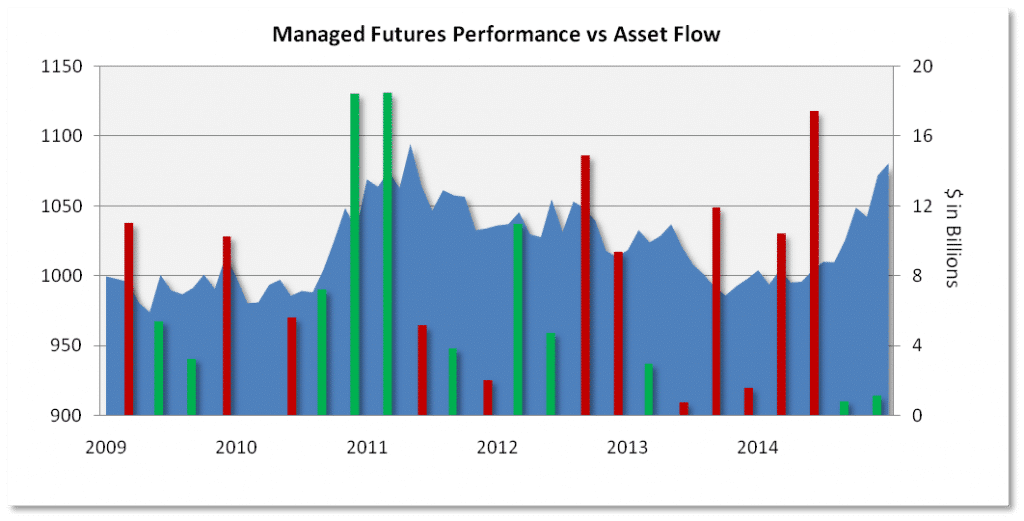

Which fits quite nicely with our “In at the Highs out at the Lows” Managed Futures chart.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: In at the Highs, Out at the Lows

Back to Ben Carlson:

“Despite these numbers, I don’t think it makes sense to completely write off (or pile into) a strategy simply because it’s had a poor (or good) run over the past cycle. This is just one fairly short time frame. I’m all about intellectual honesty when discussing the markets. I don’t believe in disparaging someone else’s strategy just because I don’t invest that way. My motto has always been, ‘do what works for you, as long as it helps you reach your goals and allows you to sleep at night.”

We couldn’t have said it better ourselves, but since we’re in the Managed Futures space, we can’t help but take it a step further. We want to add one of Ben’s sentences.

“It’s worth noting that the Credit Suisse index isn’t representative of all trend following strategies, but it does give you an idea about the struggles the space has endured following the crash.”

The fact that the index isn’t representative of all trend following strategies is definitely worth noting, and shows Mr. Carlson is no newcomer to this game. But here’s where things get even a little more interesting. Because not only is the index not representative of all trend following- but trend following is not representative of all Managed Futures. As we talk about in our Managed Futures strategy review every year, there’s also Short Term, Multi-Strategy, Specialty, Agriculture, Spread, and Options strategies. Not to mention the managed futures-like Global Macro programs. Which is why those who find managed futures ‘works for them’, in Ben’s parlance; may not have found it to be as much of a struggle as the chart suggests.

For instance, in 2013, the Barclayhedge Agricultural Traders sub index was up 5.71%, when the Credit Suisse index was down -2.6%. In 2011, The Barclayhedge Discretionary Traders Index was up +2.75%, while Credit Suisse was down -4.2%. In 2012, the Attain Short Term Fund was up 10.29%% while the Credit Suisse was down -2.9%. {Disclaimer: Past performance is not necessarily indicative of future results}. Of course, you would need a crystal ball to know which of those sub strategies was going to perform each year and which weren’t; but you get the point. Just like small cap stocks can diverge from large cap, or Asian stocks be up while US stocks down; different types of managed futures strategies can, and will (and have), diverge from the poster child trend following strategy. That’s why our Philosophy is to surround a core allocation to trend following with these other strategies to ‘diversify the diversifier’.

How about a Longer View:

Which brings us to a tweet asking for a little more data – something we’re happy to dive into.

@awealthofcs managed futures are all about diversification vs returns. Curious how a 60% stock / 40% managed futures allocation compares?

— Jake (@EconomPic) July 27, 2015

Here’s what a 60/40 portfolio looks like using Carlson’s same table, with the Sharpe ratio added in to compare the different return and volatility levels (although you know we’re not huge fans of the Sharpe):

(Disclaimer: Past performance is not necessarily indicative of future results)

Data = (60/30 MF) is 60% SPY & 40% DJCS Managed Futures Index

Other data from: A Wealth of Common Sense

But as Mr. Carlson said, this is a “fairly short time frame.” What does it look like if we push it out back to the inception of the Credit Suisse index? And while we’re at it, we’ll be the first to tell you managed futures isn’t meant to replace bonds (although that might not be a terrible idea in a rising rate environment). So what does it look like when diversified into managed futures and Bonds with an allocation of (45% Stocks / 28% Bonds / 30% Managed Futures)? Here you go:

(Disclaimer: Past performance is not necessarily indicative of future results)

Data: DJCS Managed Futures Index

S&P 500 = SPY Bonds = Barclays Global Aggregate Bond Index

You can see argument for a managed futures allocation in these longer term stats, which speaks directly to Carlson’s main point:

“I don’t think it makes sense to completely write off (or pile into) a strategy simply because it’s had a poor (or good) run over the past cycle.”

For more information on Managed Futures Performance, check out our Whitepaper highlighting the “Performance Profile: Managed Futures”