The reputation around the alternative space is that Managed Futures is an asset class you need for diversification when the stock market goes into crisis. After all, it was one of the only investment strategies out there that not only showed a positive return, but showed double digit returns (Newedge CTA Index) during the 2007/2008 financial crisis.

But that type of thinking about diversification leads to a dangerous mindset, where investors see Managed Futures as negatively correlated to US stocks (going up while stocks go down, and down while stocks go up). We don’t have a problem with the first part of that, managed futures going up while stocks go down… but the other part isn’t always true. Managed Futures aren’t always down when stock go up.

Statistically – this is because they are NON-correlated versus negative correlated. What’s that mean? It means that managed futures goes up and down independently of the stock market, at times doing the same thing, at times doing the opposite – to average out as doing something different, and tending to do the exact opposite when there’s a violent or prolonged move down, because that tends to cause a sell off across various markets from Crude Oil to Aussie Dollars.

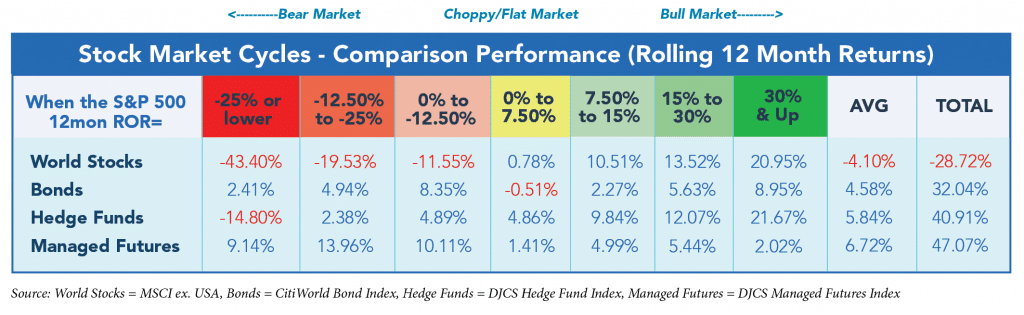

So, if investors are aware of the managed futures profile during down markets – how familiar are they with the profile during up markets (beyond the small sample size that is the past 4 years), and moderately up markets, and sideways markets? In our recently updated, “Managed Futures: Performance Profile,” we broke down stock market performance based on 12 month rolling rates of return of the S&P 500 going from 1994-2014, and then created different “buckets” of performance representing seven different market environments – ranging from the very good (rolling 12 month returns of over 30%) to the very bad (rolling 12 month returns of -25% or lower). From there, we simply looked at the rolling 12 month rates of return for managed futures on those dates which fell into each “bucket,” and averaged across all such dates. And because we’re overachievers, we analyzed world stocks, bond, and hedge fund performance in the same manner.

Disclaimer: Past performance is not necessarily indicative of future results)

Disclaimer: Past performance is not necessarily indicative of future results)

Data Span = 1994-2014

Our takeaway from the Whitepaper:

There are a few important takeaways here. For starters, the other so called diversifiers out there-hedge funds and world stocks- aren’t exactly the diversifiers you think. World Stocks, on average, lost more than the S&P 500 during down periods, and, in most instances, underperformed during the good times. Hedge funds posted positive returns on average during the down periods, but when the down periods were really down, the numbers weren’t exactly impressive. For those looking to diversify based on market cycle performance, these may not be the magic bullets you were hoping for.

Managed futures, on the other hand, on average, posted positive returns in each of those stock market cycles- the only asset class outside of bonds to do so. For those into such cycle period performance, the takeaway equation should be:

Managed Futures = Good when stocks are bad + OK when stocks are good.

To learn more about Managed Futures performance, its track record with consistency, and our rankings, download our “Managed Futures Performance Profile.”