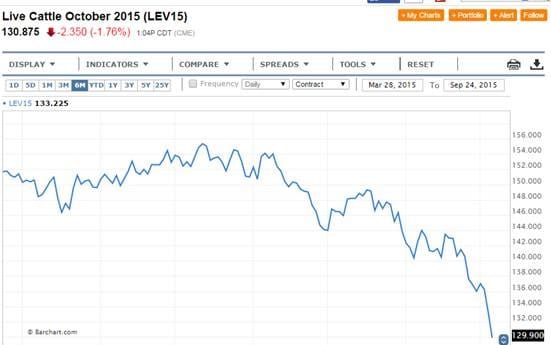

While the world has been busy paying attention to the Fed minute meetings, the Pope’s visit to the U.S., and Donald Trump’s latest gaffe, the Live Cattle market experienced a limit down day (what’s a limit move?) in the markets yesterday. With a closer look, we can see the October contract is down 12% since the beginning of August (and 5% of that coming in the last 4 trading days). {Disclaimer: Past performance is not necessarily indicative of future results}.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Barchart

For answers to this move, we turned to RCM’s newest addition, Thomas Chavez, who has experience in these markets.

“The long and short of the sharp down move in live cattle….an unexpected surge in production. The trade was bullish, and assumed a continuing tight supply situation in the 4th quarter, but it was the opposite.

The past week’s steer and heifer slaughter, at 469,000 head, was the largest weekly kill thus far in 2015. The last time the slaughter reached year-to-date high levels in the month of September was more than 30 years ago (1983). Seasonally, slaughter levels peak in the June – August time frame, so having such a supply surge in the fall is unusual.

According to the USDA, overall feedlot inventories as of September 1 were up 3% from a year ago, but they were up 7% in Iowa, and the Iowa number might be underestimated.”

Chavez goes onto say that the smaller herders might actually be the ones that are contributing the most to this influx in kills.

“The bigger surprise that most didn’t see coming, was a developing backlog of finished cattle, and underestimating the influence that smaller (under 1000 head), corn-belt cattle feeders, would have on the overall market.”

The unique twist to this story, however, isn’t just that there are more cattle kills but that these cattle are overweight while demand is feared to continue to go down. The Wall Street Journal reports that the weights for the cattle are at near record levels.

“The U.S. Department of Agriculture has reported beef prices down nearly $16 per hundred pounds in the past five days, though costs for retailers are still nearly three times as much as pork at the wholesale level.

At the same time, weights of cattle being marketed to beef packers remain near-record heavy levels, adding to the volume of beef available to grocery stores and restaurants.”

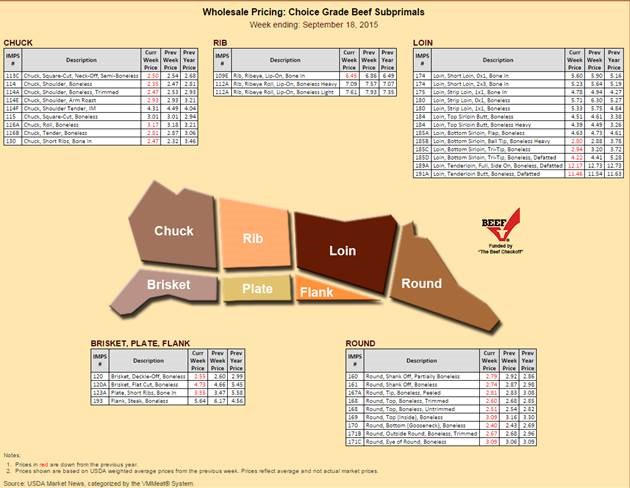

On the demand side, we’re seeing lower prices for all cuts of beef across the country.

Source: Beef Retail

Source: Beef Retail

Those tables around the different cuts of meat are the prices dating back the previous week and year. If the numbers are red it means those current prices for those cuts of meat are lower than they were the year prior.

Next time you visit your favorite high-end steak house, you may want to ask the proprietor for a discount on that $60 N.Y Strip!

(P.S – If you’re wondering about the difference between the live cattle and the feeder cattle market, we talked about that here).