We couldn’t help but take interest in this Investment News headline, which prompts a question we hear all too often from high net worth individuals, to sophisticated advisors, and multi-billion dollar pension plans, what is the right number percentage allocation to alternatives?

While many may understand that putting alternatives in their portfolios is a good move from all sorts of perspectives (diversification, crisis period performance, tax advantages, and exposure to unique markets, just to name a few), the more nuanced question of how much to invest in alternatives, is as clear as mud.

Bad News = There is No Right (Allocation) Answer

So assuming you understand the need for alternatives, what should you expect from your alternative investment, performance wise, in order to fit it into your allocation framework? And more specifically, what type of performance are you expecting from your alternative investment during the time you want it most, and does that align with your expectations for the rest of your portfolio? As a firm registered to introduce alternative investments to clients ranging from high net worth investors to pension plans, we couldn’t agree more with Investment News’ answer as what’s the best percentage to allocate.

“The trouble is, unlike more homogeneous long-only stock and bond products, alternatives come in a lot of different flavors. And unlike the oversimplified asset allocation strategy that loosely divides a portfolio of stocks and bonds based on an investor’s age, so far there is no such rule when it comes to alternatives.”

“How much to allocate is both an unanswerable question in general and one that absolutely needs to be addressed for each client.”

The general rule of thumb we see from clients is a very big thumb, ranging from 5% to 50%; with people basing that on everything from how much of the rest of their portfolio they’re willing to make room for an alternative allocation, to a more statistical approached, like the efficient frontier.

Matching Allocations with Return Expectations

What we don’t see a ton of investors doing is matching their allocation percentage with their return expectations. What are return expectations? If you’re familiar with pensions, they are rather well known for having target return numbers, so they can meet their liability stream (pension payments), and equally well known for missing those targets terribly.

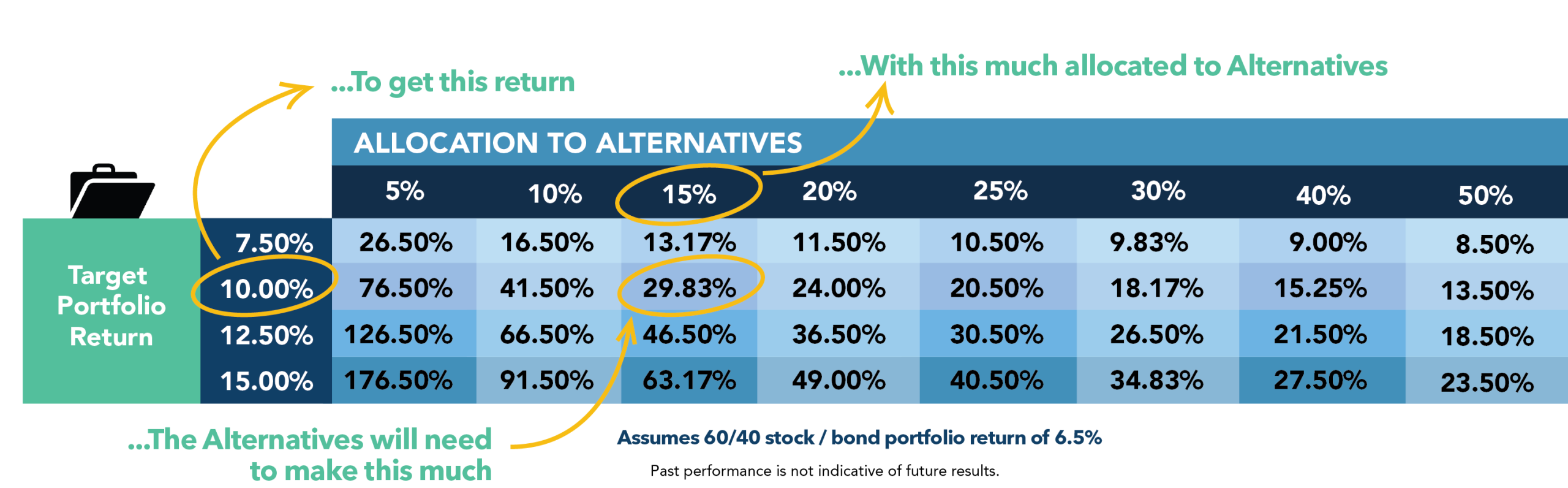

The issue for individual investors is that there is no committee or in-depth tables by the Wall Street Journal evaluating their return expectations. Because of this, most investors are left disappointed their alternatives are not providing the cushion they thought it would. We previously went into this, highlighting a great piece by Welton Investment Corporation, and it bears repeating just how much return you need from your Alts allocation to achieve your overall target portfolio returns. If I ask you right now, off the top of your head, how much return you need from a 5% allocation to alternatives to hit your 10% target portfolio return, assuming stock and bond returns are 6.5% annually, do you know?

The answer is an annual return of 76.50%… Wowsers. That means your institutionalized, low vol, alternatives investment targeting 8% annual returns is going to leave you rather short on your target return. Here’s the full table, where you can see some outrageous numbers needed to achieve target returns.

This is just math (all of us can do it), but we’d like to think when we’re presented with this type of information, our expectations change. It isn’t understood nearly enough that a nominal 2% or 5% allocation to alternatives isn’t really moving the needle at all. Perhaps that’s the real reason Calpers got out of the game, knowing that they could never allocate as much as they needed to in order to move the needle. Perhaps that’s why other institutional investors are getting closer to the 50% level.

And what about alternatives being non-correlated and showing up in a crisis? Well, we’ve talked about how not all Alternatives are actually “alternative” in that regard, in our Truth and Lies white paper, and thought we would take it a step further here to see just how much of an allocation to alts (assuming certain alts return levels) is needed for alternatives to keep the overall portfolio at certain bear market target return levels.

For example, don’t want to be down more than -5% in a bear market when the 60/40 portfolio is off -12.5%? Then you’re going to need a 34% allocation to an alts product designed to make 10% during such a crisis period (hmm, hmm, better look up managed futures for that one).

Here’s the table on that one. Again, it’s just math… but worth while to put down on paper:

If the Glove Fits

The bottom line – if you want more return, you need to take on more risk – there are no two ways about it. That risk can come in the form of an increased allocation to alternatives, increased expectations out of your stock/bond/cash allocation (perhaps shifting into small cap stocks, foreign markets, junk bonds or something else to bump that expectation (and risk) up a bit), or increased expectations out of your alternatives allocation (perhaps using notional funding to turn a 10% return into a 30% return on cash, for example). [Disclaimer, the use of leverage greatly increases the chance of loss]

The bigger takeaway for us is the point that investors may need to both allocate more and in order to have realistic expectations for their alternatives returns. You see, in the spirit of “you can’t get something for nothing,” it’s important to remember that there just isn’t a way to turn a bunch of sub-10% returns across assets into a total portfolio return of more than 10%. The power of a diversified portfolio having alternatives may mean 3 + 3 + 3 equals 10… but this analysis shows us not to expect 3+3+3 to equal 20 or more.

This takes a little of the magic out of investing, where we dream of getting in on the next Apple or being a seed investor in Facebook. We want to believe that a small allocation to something risky can turn into something big – but it’s very hard to escape the math on this one. The simple truth is that the smaller your allocation to alternatives is, the larger the alternatives return has to be to move the overall needle.

The question now is, will your allocation to alternatives move the needle, or is it just there because you know you need “alternatives” in your portfolio?