Not so long along we tried to “un-convince” (not a word) you that commodities are dead (is that the same as convincing you commodities are un-dead), given that a majority of commodities have been selling off since the end of 2008-2009 and the contrarian move started to believe in a bounce versus continued weakness. And while it’s been particularly bad for long-only commodity strategies this year, let’s face it, commodities aren’t going to zero – people will still pay something to fill up their car or eat some bread.

And wouldn’t you know it – we’re starting to see a few markets bounce lately. Take Sugar:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Barchart

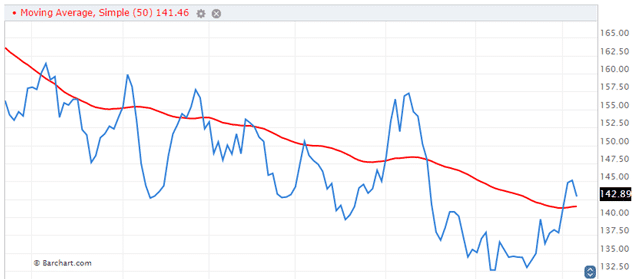

Or Coffee:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Barchart

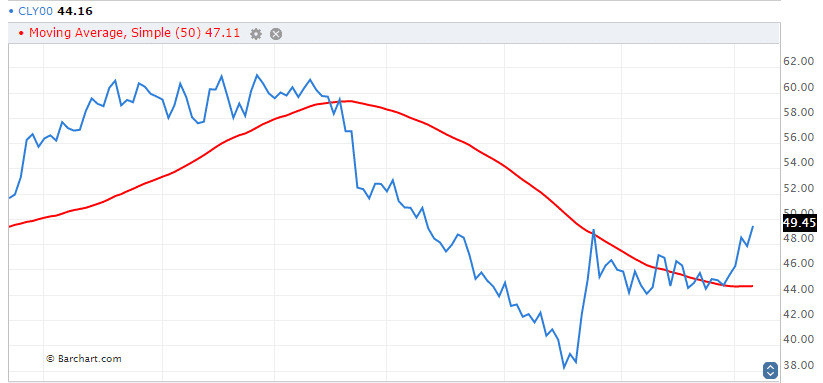

Or everyone’s favorite Crude Oil:

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Barchart

Of course, while technical traders are seeing bounces and reacting as needed, there are others who are betting that there’s more downside to come. Take the recent Bloomberg piece titled: Caution: More Commodity Price Weakness Ahead, which argues there are tons and tons of supply out there:

“Meanwhile, supplies of almost every commodity are huge and growing. China joined the World Trade Organization in late 2001 and, not by coincidence, commodity prices took off in early 2002. As manufacturing shifted from North America and Europe to China, it sucked up global commodity output. From 2000 to 2014, China’s share of global copper consumption leaped to 43 percent from 12 percent. China’s portion of iron ore purchases similarly zoomed to 43 percent from 16 percent, while aluminum went to 47 percent from 13 percent.

….Similarly, Brazil subsidized the export of sugar, which is down 67 percent in price since February 2011, and no doubt will be forced to pour more money into the industry. Already, 80 of 300 sugar mills in the South Central region, where 90 percent of Brazilian sugar is produced, are closed. Stockpiles are at a 35-year high. Insolvent mills are trying to sell as much sugar as possible to generate cash, which has depressed world sugar prices.

But the bottom line to us is that it’s missing the point to think it’s just about when commodities will go up again. As the past few years have proven, it’s quite dangerous to invest in long-only commodity exposure where you can only make money when the market is going up. But it’s not just the fact that commodities sometimes go down (sometimes in dramatic fashion); there’s a whole lot more going on in the commodity space, which makes the game quite difficult (just ask Glencore). So be sure to check out 9 Things to Know Before Playing the Commodity Sell Off, if you’re so inclined to in fact play.

As you’ll read among those 9 things – there’s a little problem of futures contracts expiring and the ETFs that invest in such contracts having to pay to ‘roll’ to the next contract, which can cause mismatches between the commodity’s actual performanc and what you get in the ETF… Which conveniently leads us to our monthly look at Commodity ETFs versus the futures markets they track. (maybe we need to add an inverse ETF part with short futures exposure… stay tuned!)

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Sugar uses the October contract, Soybeans the November contract.)

Long/Short Ag Trader CTA = Barclayhedge Ag Traders Index