Here we are one month into January, and all the sudden Managed Futures is getting name dropped in a “I know a guy” sort of way. Today, Business Insider called Managed Futures the dominating Hedge Fund strategy in 2016, all while the Morningstar Managed Futures Mutual Fund Category has received 20 straight months of inflows (receiving $1.5 Bil in Jan alone).

What’s not to like – with Managed Futures offering up an average gain of 2.25% in a month where stocks lost -5.21% and global stocks lost -6.71%. Obviously, it’s because at some level, we’re all performance chasers, while we don’t like to admit it (unless we apply strict discipline in our portfolio), and the financial biz is following suit.

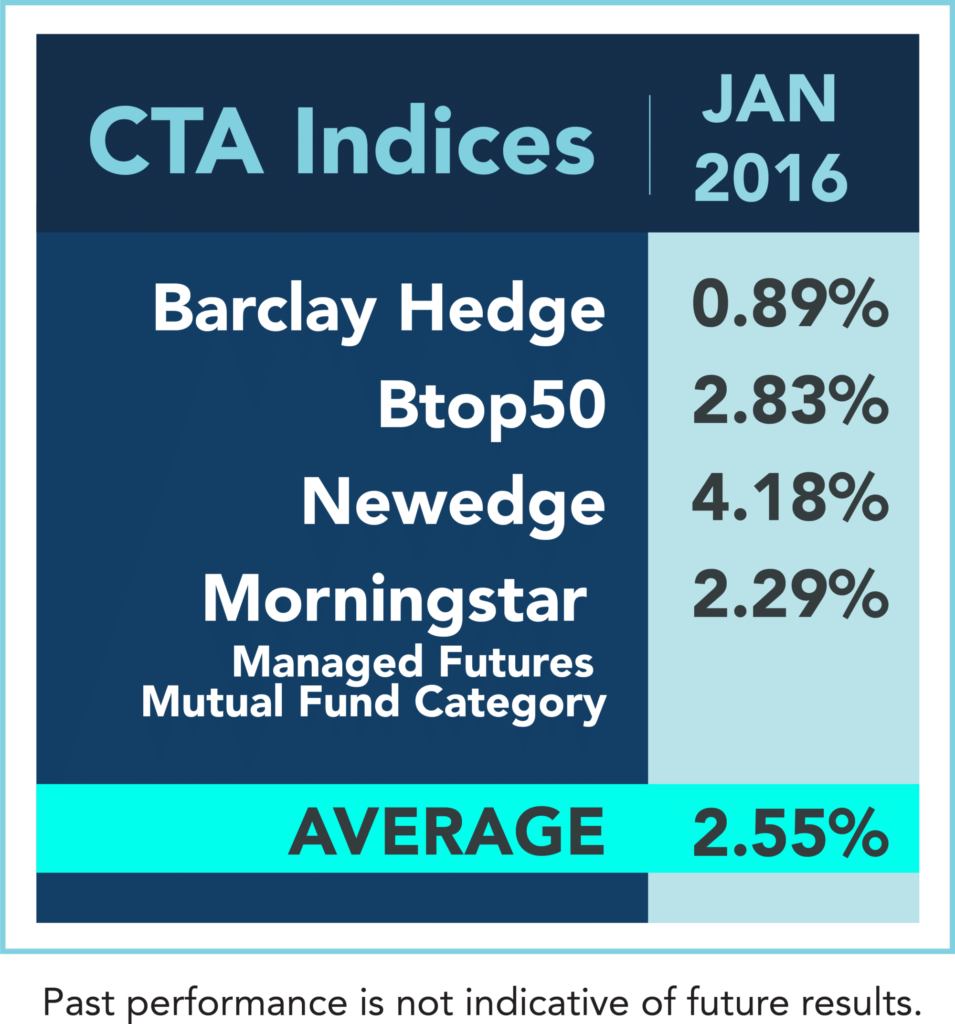

(BarclayHedge reporting 74% of funds, numbers subject to change)

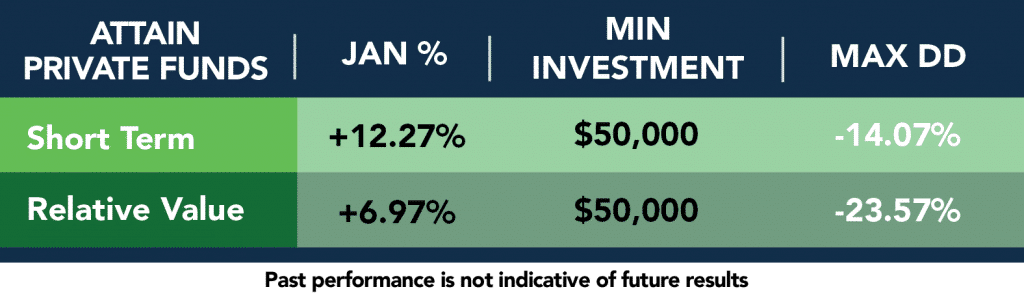

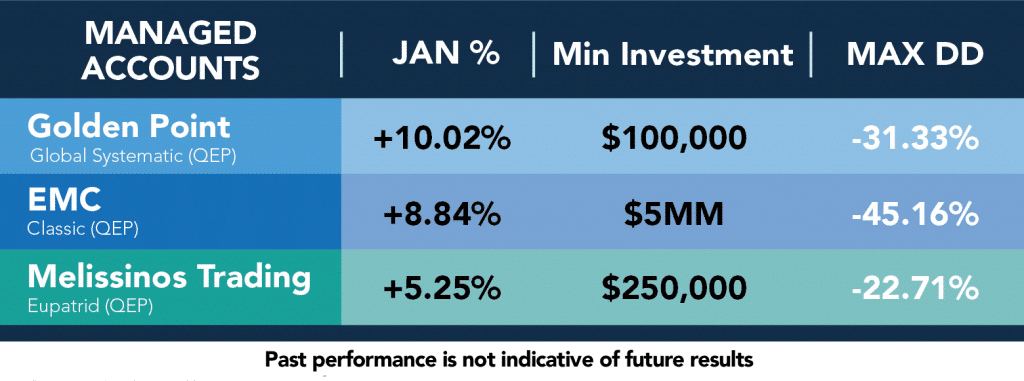

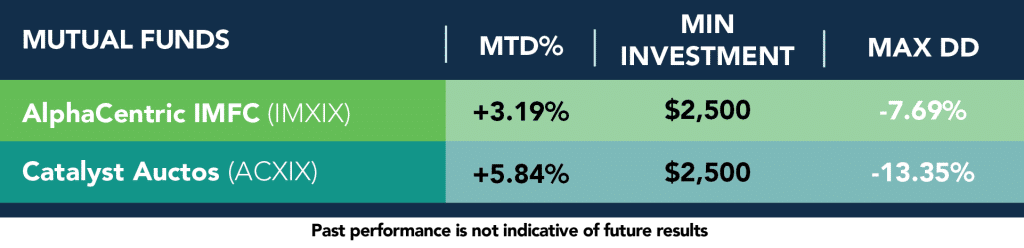

Those numbers sure look good from the outside, but as experts who perform due diligence on the hundreds on managers in the Managed Futures space, this performance is, well… average. Take a look at the net (estimate) performance of some of the managers we follow.

Of course we don’t know if this market uncertainty will continue or subside. We could be staring another 2008 in the face, or markets could pull a reversal and erase these gains. We do know that every day it continues is better and better for managed futures, both in terms of upside, and in reducing future downside (as systematic models typically move their exit points down over time to lock in more and more of the gain to that point).

Wherever we’re headed the rest of February and beyond, what we’re excited about is seeing the diversification in real time. We’re seeing non correlation in real time. Just consider managed futures made money while stocks made money in 2014, were flat to down slightly while stocks were about the same in 2015, and now are making money while stocks are losing lots of it. That’s a year of positive correlation, a year of no correlation, and now a year of negative correlation. Non correlation is a bit of an abstract concept, but there it is in black and white. It means sometimes you’ll do the same, sometimes you’ll do differently – resulting in differences, on average.

If you’re wondering just what things could look like the rest of the year, check out our Managed Futures 2016 Outlook, which you can download here.