One of the main benefits of investing in managed futures is the ability to do so through Notional Funding in a separately managed account – whereby you don’t have to put up a cash deposit equal to the program’s minimum investment amount in order to invest in that program. For example, it is possible to trade the $1,000,000 in program X with a cash deposit of just 200k.

If you are saying, so what…. you can put up just a portion of the investment amount in all sorts of investments: stocks via a margin account, real estate via a mortgage, art via a credit card; you are missing the one big difference. That difference is that there is a cost to buying stocks on margin or purchasing real estate with a mortgage. That cost is the cost of money or the interest rate you pay to borrow the funds to purchase the investment you are interested in.

With notional funding, there is no borrowing of money and therefore no interest rate and no cost of money. How can there be no borrowing? Because we’re not talking about someone loaning you $1 mm to meet the minimum (or about trading a smaller version of the program with $200K), we’re talking about having $200,000 traded as $1,000,000 via the use of notional funding.

But as an old history professor we knew would say – ‘that begs the question’ – ‘What is Notional Funding?’ And when we answered notional funding is funding an account through the use of notional funds, he would again say that begs the question: ‘What are Notional Funds?’ We should have known not to use the word in the definition.

Notional Funds

Notional funds represent the difference between a managed futures investment’s minimum investment amount and the amount of cash an investor is willing to put towards a managed futures program at that time. An investor may not have the full amount of the minimum, or wish to only put up a portion of the minimum and use the rest for another investment. In a way; notional funds can be thought of as added money which is used to bridge the gap between the cash outlay an investor is willing to put towards a managed futures program at that time, and the stated minimum amount of that program.

A quick example is probably the easiest way to describe it. Take the aforementioned Three Rock program (QEP Investors only) with its minimum investment amount of $1,000,000. An investor does not actually have to have all of that money in their account in order to trade the program. Levels of notional funding vary between managers, but for this example, Three Rock will allow clients to use notional funds to cover up to 80% of the investment minimum.

The actual cash balance plus the notional funds balance equals the required minimum investment amount of $1 mm. Another way to think of how this works is to imagine having that $200,000 account, but telling the manager to trade is as if it was $1,000,000.

If you’re asking “how the heck can you trade more than what you have in your account?” – let us explain further.

To understand how an investor can use these notional funds, we must first back up a step and understand how a managed futures advisor arrives at their minimum investment amount. Minimum investments could, or perhaps should, be further split up into three distinct levels, specified as:

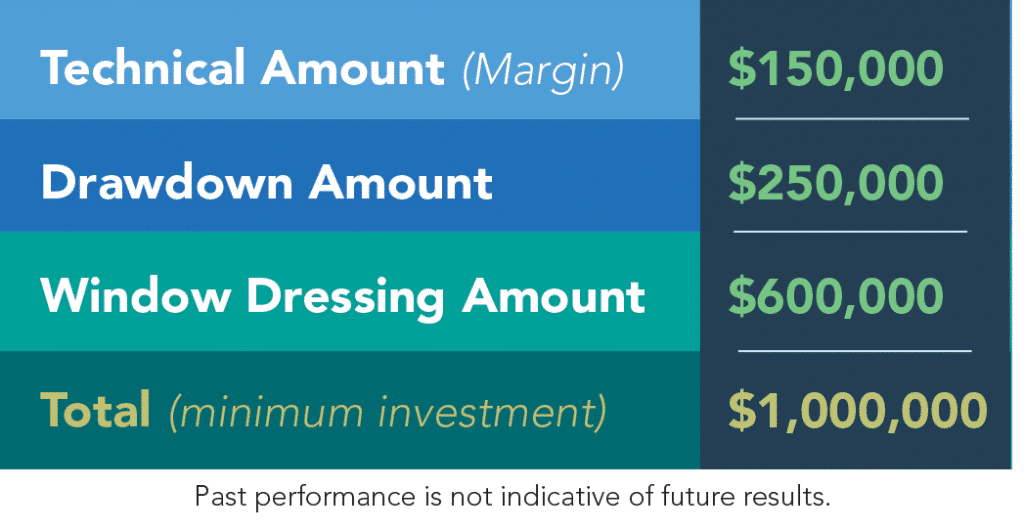

- The Margin Minimum: the technical minimum amount needed to actually place the trades on the exchanges

- The Drawdown Minimum: the amount for an investor to withstand any eventual drawdown of the investment

- The Window Dressing Minimum:the amount to make the percentage drawdowns and returns attractive to the greatest number of investors.

Margin Amount: The first part of the minimum investment amount is the amount technically needed to place trades. This is what the exchanges and clearing firms refer to as the margin requirement. Any account which wishes to trade a futures contract on a regulated futures exchange like the Chicago Mercantile Exchange must first have enough money in the account to cover the performance bond requirement of the exchange (the margin). This insures that the exchange can make the trader who takes the other side of the trade good should the trade go against the account.

Margins can sort of be thought of as the amount of money which could be lost on that position in a single day – and the exchanges and clearing firms make sure each account has that much money – or else the whole system doesn’t work. If this wasn’t in place, where would a winner get her winnings from – the loser could disappear.

- Drawdown Amount:The second part of the minimum investment amount is the amount an investor needs to withstand any eventual drawdown. Again, this is another technical level of sorts, in that an account must have at least that amount in order to stay above zero. If the investment has the possibility of losing $150,000, for example, in the normal course of operation, then an investor better have at least that amount in order to proceed. If they didn’t, they would have to get out of the investment during the normal ups and downs of the investment.

Think of it like a tank of gas; if you are driving 100 miles and need 5 gallons of gas to get there, you better have at least 5 gallons of gas in the car – or else you’ll never get there.

Window Dressing Amount: The third part of the minimum investment amount is the amount needed to make the percentages appealing to potential investors, or “window dressing” amount. Unlike the margin amount, it is simply a subjective amount the advisor computes in order for the average returns and risk of his or her program to come out “nicely,” for lack of a better term.

Imagine an advisor with average annual returns of $100,000 and drawdowns of $50,000. If that advisor sets his minimum at $100,000 – the average annual return in percentage terms is 100% with a 50% drawdown; while if the advisor sets his minimum at $1,000,000 – the average annual return in percentage terms is 10% with a 5% drawdown. While the returns in dollars are exactly the same, the advisor would likely find much more success raising money with the $1 Million minimum amount, because investors will ignore programs with large drawdowns such as the 50% drawdown number. The difference between the desired minimum and the minimums needed for margin and drawdown is the window dressing amount, and it is often this amount which can be “notionalized.”

If we look at a fictitious CTA program with a $1 million minimum investment, and 15% average margin usage, and -25% max drawdown as an example, those levels would be:

Understanding that up to 80% of a managed futures program’s stated minimum investment amount can be nothing more than window dressing gets us a step closer to understanding how you can use notional funds, when investing in a managed futures program.

It should be clear that while an investor actually needs both the ‘technical amount’ for margins and ‘drawdown amount’ to stay alive, the investor doesn’t necessarily need the window dressing amount. If it is only there to make the returns and drawdowns more palpable for most investors; an investor who can stomach much larger percentage gains/losses (you will have the same dollar gains/losses) doesn’t need window dressing.

How can you use notional funding?

For those investors who don’t want the window dressing, (those who can handle 3 to 5 times the percentage gains and losses), notional funding is perhaps the most efficient form of investing available to investors. Once investors understand that the window dressing amount is only to make them feel better about how much (in percentage terms) they have made or lost – they are free to take that window dressing amount and use it for other purposes.

Notional funding also allows for the trading of multiple managed futures programs with a single cash allocation. Assume an investor wants to put $900K into managed futures. An investor could use all of those funds on one manager, our could trade a balanced managed futures portfolio of $1m in program X, $1m in program Y, 1m in program Z, totaling $3 Million in initial investment amounts, with just the $900K in cash.

This would represent leverage of roughly 3.3 to 1 in the account ($900K traded as $3 Million), and the investor would see percentage gains and losses on his $900K that are 3.1 times what an investor putting up the full $3 Million would see.

Now come the fun part touched on in the beginning of our discussion. The cost of doing this is zero. There is no interest rate charged on the notional amount like you have in the stock market when buying shares on margin or when buying a house with a mortgage. This is because there isn’t any real money behind the notional funds, thus you aren’t borrowing any money and thus there is no charge for the notional funds you employ. The notional funds are, in a way; nothing more than the amount of leverage you are taking on. The more notional funds you use; the more leverage you are applying to your investment.

What are the risks of notional funding?

While there is no physical cost to notional funds, one “cost” is that the fees charged by the manager are on the nominal amount of the investment (meaning the full minimum amount), not the cash balance in the account. So if the program you’re participating in has a 2% management fee, that will balloon to an 10% annual fee on your cash amount if you used 20% cash with 80% notional funds to meet the minimum. Likewise, commissions will have a much bigger impact on the account in percentage terms.

It is important to note, however, that the fees and commissions will not be any different, in dollar terms, than they would be if fully funding the account. Consider a $1,000,000 minimum investment program, which an investor invests in using $250,000 cash and $750,000 notional funds (25% cash/75% notional). The 2% management fee on this account would be charged on the $1,000,000 minimum nominal level of the account, meaning the charge would be $20,000. That $20K charge would be the same for an investor doing 100% cash/0% notional, 50% cash, 50% notional, and our 25% cash/75% notional example; but it would represent a 4% charge ($20K/$500K) for the 50%/50% account, and an 8% charge ($20K/$250K) for the 25%/75% account.

So while leverage through notional funding increases the percentage amount of fees and commissions, it has no effect on the dollar gains and losses. The key to understanding notional funds is to understand that while the percentages change – the dollars do not. The $20,000 in fees does not become larger – they stay at $20,000 no matter how much notional funds you use. They only become larger as a percent of the cash in your account, and only when the cash in your account gets smaller. So 2% of $1 MM = 4% of $500K = 8% of $250K. They all equal $20,000.

There is also a greater risk that you may lose more than you deposited in the account when using notional funds. If a $1 Million minimum program loses $500K, and you are notionally funding that account with just $250K (having $250K traded as $1 Million), your account will have lost $250K more than you deposited in it, and you will owe that money to the clearing firm. Of course, even if you had fully funded the account, you would still lose the same $500K (again, the dollar amount of gains and losses does not change, only the percentage amount), and whether you notionally fund or fully fund – there is always the possibility with a futures investment of losing more than you deposit in your account.

The last negatives to consider are the mental anguish you may go through seeing percentage drawdowns 4 times those that are reported (but again, you’re still losing the same amount of dollars) and the nervousness you may encounter when/if the a drawdown takes the account down to within a few hundred dollars of a margin call. And finally, if the account goes on a margin call in which you have to deposit more money into the account in order to keep trading with the program, the risk that you choose to cease trading the program instead of adding more money, and then miss out on the upside when and if the program rebounds.

If you’re not familiar with notional funding, or still have questions, feel free to contact us 312-870-1500 or email us at [email protected]