Quants are everywhere. They run Wall St; they’re in healthcare and in education. The rest ended up telling us when and where the hurricane will hit.

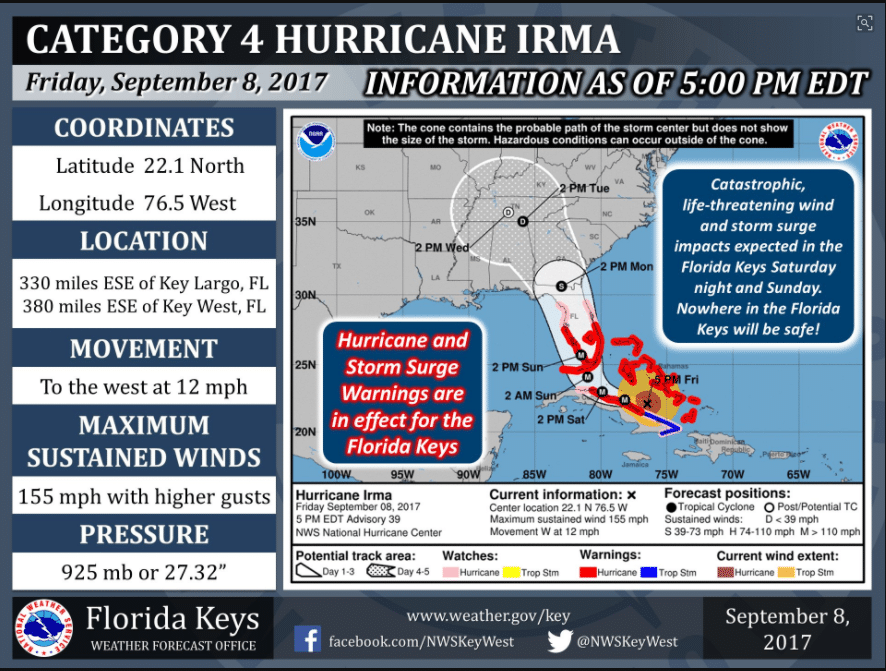

It’s hard to spend your time analyzing models for a living and not recognize quantitative modeling when you see it. Here’s what most of the world sees when checking out the possible landfall time and intensity forecasts for Irma…

But a more in depth look at what’s going on – is dozens of models are using different inputs and variables to cover a wide range of possible outcomes. Here are 20 different models on the forecast of Irma.

If you’ve ever wondered what’s going on at the top quantitative hedge funds in the world – it’s something quite similar to this. But instead of the wind, water, temperatures, and steering currents, they are using market data like price, volume, correlations, and volatility. They’re outputting various ‘model runs” just like this on where a potential trade might go, and whether by combination of trades or intelligent selection of model – typically end up with the ‘ensemble’ model – which can generally be thought of as the average or mean of the models.

They typically aren’t following a single model hoping for the best outcome, just as the National Hurricane Center doesn’t just bet on one model and hope it’s right. The National Hurricane Center diversifies its risk (of completely mis-forecasting and putting lives at risk), and skilled quants diversify their risk (of completely mis-forecasting and costing the fund millions) by doing a similar thing and capturing dozens if not hundreds of possible outcomes.

Note this is very different than what someone like Bill Ackman does. If he were in charge of Hurricane forecasting – he’d gather up a bunch of experts and look at a bunch of maps, and plot a course right through those islands… maybe he’s brilliant and that works… maybe it works for a while. But can it really work as often and as risk-contained as computer models generating hundreds of possible paths.

P.S. – The National Weather Service recently moved to a new modeling system.