Oh, to be an investor, where the markets often seem to do something completely different than what you thought was going to happen. The old buy the rumor, sell the news axiom, perhaps? But whatever you call it, October brought the idea home hard. Here we were expecting some Q4 magic in the CTA space, especially with the election looming…

Source: RPM risk and portfolio management

When a nasty bit of reversals in bonds and currencies sent everything all haywire, as evidenced by Bloomberg’s headline: Bond Routh Deals Fresh Blow to Fast Money Quants in Year of the Whipsaw

Many systematic traders had built up significant bond, rate, and rate adjacent (currencies) trades coming into and after the Fed’s long awaited start to easing US interest rates. Makes sense, right? The Treasury market had been on a nice five-month upward path – the best streak seen in 14 years according to the article.

But then the script flipped. Strong economic data came in, making more of those rate cuts look a bit premature. Add in some election-related market moves, and suddenly yields jumped more than anyone expected. This caught many funds loaded up on the wrong side of the trade, exposing them to Trend Followers most dreaded pattern, the “V-shaped” reversal or whipsaw.

Source: finviz, RCM edits

Now, October saw upside down ‘Vs”, except in the US Dollar which is a mirror image of the foreign currencies. But this is the risk in trend following… as October 2024 sharply reminded us. These sharp V-shaped reversals are kryptonite to typical systematic trading strategies that use price momentum. These models will use the nice trending up moves on the left side of the charts above to enter new trades, with that up move signaling an up trend. From there, the trade is rather simple: if prices keep going up, the trade is likely to be a winner. If there’s a reversal, it’s likely to lose.

But that’s a little over-simplified, because if it’s a sharp, V-shaped reversal, the trade is likely to be an unusually big loser. Why?

Well, one of the long-standing criticisms of systematic trend following strategies is that they often give back open trade profits. But this complaint usually refers to profitable trades, like “you made 10% as the market had an outlier move, then ended up only making 5% as the market slowly retracted and the program waited to get out until the trend was confirmed over.”

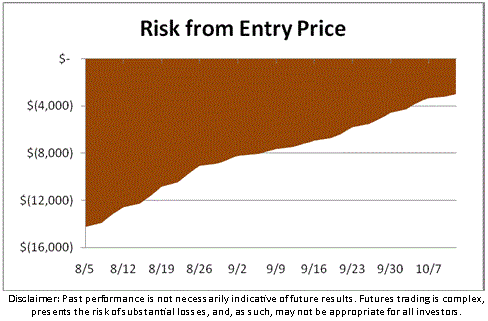

The V-shaped reversal brings “full stop outs” into play because of how quickly the reversion to the mean occurs. A typical systematic managed futures program might risk around 0.75% of account equity per trade, but few trades actually lose that much. This is because a typical trend following trade combines risk from both the entry price and the market price, meaning most models only need a small amount of time moving in the desired direction for the moving average of prices to shift, thereby reducing the potential loss from the entry point.

Here’s a graphical look at the risk over time (as measured from the entry price) for a fictitious trade using a basic trend following model. You can see that the greatest risk to a typical trend following type trade (the bulk of managed futures trades) is right at the outset, where the position is at risk of a sharp reversal and what we call a “full stop out”.

The V-Shaped reversal means you’re at risk of losing quickly, before the system has had time to move its risk protections over time and in line with the market’s movements. Said another way – these long trades had a best case scenario = market continued trending up, a no-blood scenario, where the trend didn’t continue, but markets moved sideways for several weeks/months, eventually signaling the end of the up trend. And a worst case scenario, which is a sharp, v-shaped reversal where there was little time for trade exits to move closer.

So, don’t go firing your manager for guessing wrong on the Fed. There was no guessing. This is part and parcel for Trend Following and the CTA/Managed Futures space. They’ve seen it before and they’ll see it again. And even while October may have been painful, it is mostly a win for the program’s risk parameters, being that many markets could spell the end for some strategies, but systematic strategies ethos which typically risks less than 1% or so on each trade, keeps them in the game. They’ll now patiently wait for the next setup, getting long if that is an up trend, and short if it’s a down trend. You may remember October for a bit, but the systematic models have already ‘flushed it’, moving on to finding the next trend.