Your Gateway to

Alternatives Intelligence

Dive into the RCM Alternatives Education Center, where we’ve been breaking down the complexities of alternative investments for over 20 years.

Featured Resources

Our Podcast

Conversations on what makes alternative investments tick.

We dive into unique hedge fund strategies, chat with industry superstars, and explore everything in between. Hosted by RCM Managing Partner Jeff Malec.

More episodes

-

“Dr. Copper”: From Chilean Mines to Chinese Smelters to AI Data Centers in the US – with Kurt Nelson & Natalie Scott-Gray

Copper steps out of the shadow of gold and silver in this wide‑ranging conversation with StoneX’s Natalie Scott-Gray and Summerhaven’s…

-

The Doctor who Traded Pork Bellies: Patrick Welton’s Journey from Stanford Oncologist to one of Trend Following’s Quiet Legends

In this episode, Jeff Malec sits down with Dr. Patrick Welton to trace his remarkable path from Wisconsin kid to…

-

Painting Corners to Protecting Portfolios: Former MLB pitcher Scott Karl on How Athletes Blow the Money, Alts, the Mental Side of Performance, and the NIL Era

In this episode, former Milwaukee Brewers left-hander Scott Karl traces his journey from Carlsbad baseball standout to big league starter…

Listen wherever you stream

Alternatives Blog

Two decades of practical insights on futures markets, CTAs, and alternatives – delivered weekly without the fluff.

-

Asset Class Scoreboard – May 2026

May 2026 saw equity markets continue their upward momentum from April, with U.S. Stocks gaining +5.26% and World Stocks adding…

-

“Dr. Copper”: From Chilean Mines to Chinese Smelters to AI Data Centers in the US – with Kurt Nelson & Natalie Scott-Gray

Copper steps out of the shadow of gold and silver in this wide‑ranging conversation with StoneX’s Natalie Scott-Gray and Summerhaven’s…

-

The Hardest Trade Is Holding the Thing That Doesn’t Hug You Back

Let’s start with a confession: every asset in your portfolio pays you in two different currencies. The first is returns.…

-

The Doctor who Traded Pork Bellies: Patrick Welton’s Journey from Stanford Oncologist to one of Trend Following’s Quiet Legends

In this episode, Jeff Malec sits down with Dr. Patrick Welton to trace his remarkable path from Wisconsin kid to…

-

Leverage Is Bad. Except When It Isn’t. Morningstar Just Made the Distinction Official.

We’ve all heard the lectures. Leverage caused the GFC. Leverage blew up Long-Term Capital Management in ’98. Leverage cratered Amaranth…

-

Painting Corners to Protecting Portfolios: Former MLB pitcher Scott Karl on How Athletes Blow the Money, Alts, the Mental Side of Performance, and the NIL Era

In this episode, former Milwaukee Brewers left-hander Scott Karl traces his journey from Carlsbad baseball standout to big league starter…

Whitepapers & Research

Quarterly deep dives that cut through the noise with institutional-grade analysis on everything from VIX strategies to emerging opportunities.

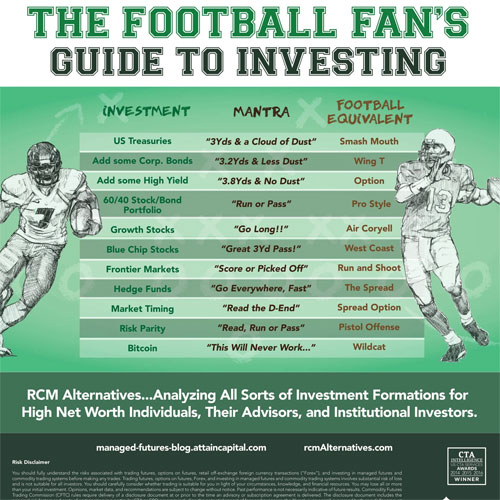

Visual Learning

Complex concepts distilled into clear visuals that get to the point quickly.

Stay Ahead of the Curve