We did our monthly look at how various commodity ETFs track the futures markets they’re designed to follow recently, and found a rather interesting data point in Natural Gas.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Natural Gas Futures = Selling the December Futures contract the last week of November (including exit costs), then using the following December contract numbers)

We’ve talked before about “3 Big Reasons Commodity ETF’s Aren’t Getting the Job Done,” and the usual picture is of the ETF underperforming the asset they track because of prices being in contango and a little thing called roll yield, which the ETFs have to pay if further out prices are more expensive than nearby prices, and if you look back at UNG since inception, it’s clear that the ETF underperforms a simple strategy of rolling the December futures annually:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

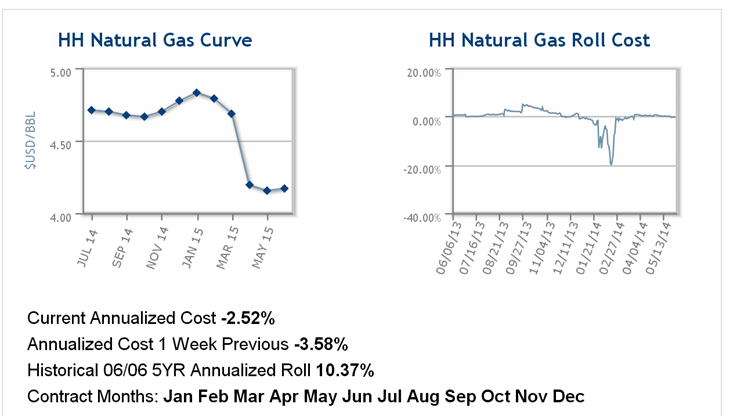

So why is UNG suddenly outperforming the December futures strategy? You guessed it… Natural Gas has moved ever so slightly into Backwardation – the condition opposite ‘Contango’, where the near prices are more expensive than the further out prices. In that scenario, the ETF earns the roll yield instead of paying it. Here’s a nice graphic and stats from Hard Assets Investor: showing the 5yr annualized roll cost has been 10.37% (a cost of 10%), while the current roll cost is -2.5% (a benefit of 2.5%).

Charts Courtesy: Hard Assets Investor

But whether or not the futures are down -67% since 2009 or the worst ETF ever is down -78%, does it really matter. It’s kind of like being the cleanest dirty shirt or skinniest fat kid. You’ve still lost a boat load of money betting on the “energy of the future”. And I guess that’s what the folks at Direxion and VelocityShares and ProShares were thinking when they launched Inverse Natural Gas products… and not just inverse, but 2x and 3x inverse. Why just go short, when you can double and triple your leverage? Direxion even got the great ticker – GASX – seemingly unconcerned with the link to the world’s number 1 brand for flatulence and bloating relief.

If you had to guess when these guys launched their inverse Natural Gas ETFs, what would you choose:

A. In mid-2008 when Natural Gas had risen ~100% over the last 12 months

B. In 2011 and 2012 when Natural Gas had fallen between 60% and 80% from its highs

Pat yourself on the back if you chose B. These funds were launched in a hurry to capitalize on the big move down in Natural Gas prices, just in time for prices to rally about 130% from their 2012 lows, just like the long Natural Gas ETF (UNG) launched just in time for Natural Gas to fall 80%. A look at the all time charts for these ETFs is like watching a race to see who the first one to hit -100%.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

We’re not sure if this is a commentary on the volatility of Natural Gas, on the dangers of turning futures markets into ‘safe looking’ ETFs, or on the age old problem of investors getting in exactly at the wrong point… but it sure is a weird set of circumstances when investors buying the long ETF are down about the same amount since inception as those buying the short ETF. They can’t win for losing. Here’s the sad performance since inception of the various Natural Gas ETFs:

(Disclaimer: Past performance is not necessarily indicative of future results)

Source: Google & Yahoo Finance