Don’t look now, but the Golden child of commodities is creeping back in the limelight – riding a near 20% up move so far this year back into relevance (or at least headlines). We’re talking about the so called ‘barbarous relic’ Gold, of course:

Gold just saw its biggest one-day gain since December 1, 2014 $GC_Fpic.twitter.com/KwC6UqpzDU

— Amanda Diaz (@cnbcdiaz) February 8, 2016

Three days later, Gold saw an even bigger gain of $50 an ounce spike, or around a 4% increase. What’s going on? What’s pushing the favored market for “the end of world types” higher? Look no further than interest rates, and the Fed’s apparent change of heart on raising rates in 2016. The logic goes – if the Fed doesn’t raise rates, we’re looking at paper money yielding essentially $0, with the real possibility that you would have to pay to have your money held in a bank. For those who view Gold as a store of value, akin to another currency, they would much rather hold Gold than a paper currency at risk of being devalued.

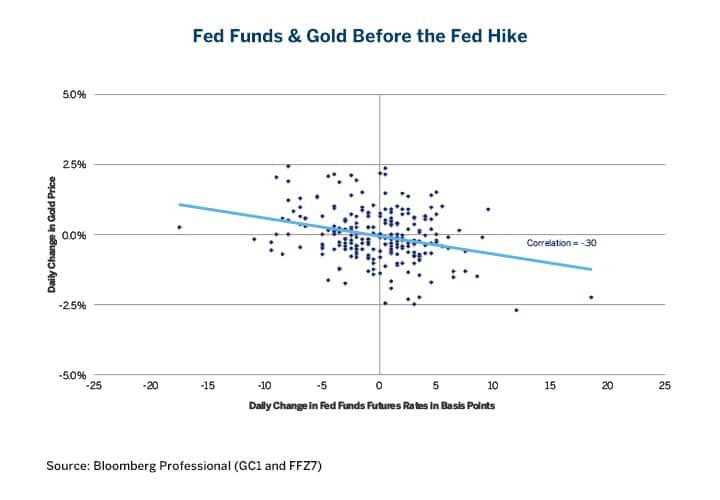

CME Group Senior Economist Erik Norland took a deeper look into whether this Gold rally is sustainable or just a flash in the pan, and one of the most interesting findings is Gold’s negative correlation to Fed Fund Futures contracts (which we talked about it detail here). Specifically, how the negative correlation between the two increased dramatically after the fed raised rates.

On a daily basis, from January 1, 2015 to December 16, 2015, gold correlated at -0.30 with the daily change in the Fed Fund Futures rate (100 minus the price) as shown on Figure 2. Since the Fed’s December 16 rate hike, the correlation has become even stronger: -0.57. When expectations for Fed rate increases rise, gold tends to fall; and when expectations for Fed rate moves diminish, gold tends to rise. And, while we do not think the Fed would adopt a negative rate target for federal funds, as it would be punishing for bank earnings, even thinking about negative rates in the U.S., gives gold prices a boost.

(Disclaimer: Past performance is not necessarily indicative of future results)

Charts Courtesy: CME Group

Granted there have been less days since the fed hike, so the correlations are bound to be a little skewed; and it’s not too hard to see how all of the other market forces out there currently might be pushing the increase in negative correlation.

…there has been a sea change in expectations: amid collapsing oil prices, falling equity markets, and roiled credit markets, Fed Funds Futures by February 11 were pricing a small chance that the Fed might even cut rates. Another round of policy tightening was not priced until 2018. And, in response to actions by the European Central Bank (ECB), the Swedish Riksbank, Swiss National Bank, and Bank of Japan, Fed Chair Janet Yellen indicated that the Fed would study the negative rate policies being adopted by their peers.

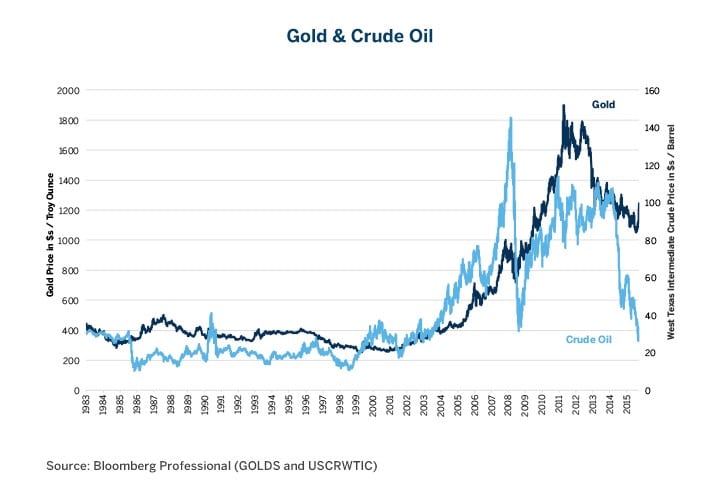

Finally, Norland warns that the historic crude oil move, could actually put a cap on any gold rally, in part due to cutting mining and production costs, which could increase supply.

Lower energy prices: Mining and refining gold is highly energy intensive, and lower oil, natural gas and coal prices will reduce the cost of doing business… which may limit further upside in the long run.

At the end of the day – we’ve never been big believers in Gold as a standalone investment, just like Warren Buffet . For our money, we would much rather have exposure to moves in Gold (both up and down) via a dynamic trading strategy (which is the same logic for anyone looking to play a bounce in Oil prices, coincidentally – see here). But trying to dissuade a Gold Bug is about as easy as pushing a string. They can’t even see the 20 year sideways price action between 1983 and 2002 or the near 50% drop from the 2011 highs. All they see is the $400 to $1,800 per ounce move and possibility of Armageddon.

And who knows, maybe the onset of negative interest rates is the start of some sort of Gold friendly market debacle. Only time will tell, but why put all your eggs in the Gold wheel barrow is a binary bet with just two outcomes – good or bad. Choosing an alternative investment with both exposure to Gold moves AND the ability to make money no matter what Gold does seems like a better idea than storing a wheel barrow full in a cave.

P.S — If you’re interested in the Gold commodity conversation, here’s our previous commentary.

- The Surprising Connection That The Worst Performing ETF’s Share

- Goldfinger, Gold iPhone, and Gold Backwardation!

- Who’s Meddling with Metals?

- You Think Gold’s been doing Bad, Check out Gold Miners…

- Gundlach’s Next Call – Short Gold

- RAID for the Gold Bugs

- Gold Forming Classic “Frowny Face” Pattern

- Smiling While Gold Sinks

- Kicking Gold While It’s Down

- Platinum Outshining Gold in the New Year

- Coinage Takes a Well-Deserved Nosedive

- Gold and Stocks Decoupling?

- The Best Way to Lose Money on Gold