They say to get smarter… it helps to hang out with smart people. Well, in the investing world, the corollary may be: to be a better investor (smarter), read good investors (smart people’s) research work. We eat up hundreds of research pieces every month and thought this piece from Quest Partners was particularly on point. Quest* just happens to be up around 15% so far this year {past performance is not necessarily indicative of future results}, after enjoying a spot on our Top 5 Rankings for Risk Adjusted Performance at the start of the year. So enjoy some smarts from one of our favorite managers. Here’s Quest Partners on the current market environment and outlook:

As we review the investment landscape and our proprietary research, two clear themes are emerging:

- End of QE-driven low volatility regime as macro and political risks rise.

- Increased risk of sharp reversals as asset prices rise to record levels but ‘skew’ turns increasingly negative.

Breakdown Of The ‘Managed Equilibrium’

As global economies move away from the financial crisis of 2008-2009, normal rules of economic policy would suggest that crisis era policies should normalize. Contrary to normalization however, nearly every instance of moderate economic weakness since the financial crisis has been met with acceleration of unorthodox monetary policies by Central Banks.

We believe this unprecedented intervention of Central Banks in financial markets has led to a ‘managed equilibrium’ whereby asset prices are getting increasingly distorted and volatility has remained suppressed relative to what it would have been if markets were left to themselves.

We believe this period of artificially low volatility is in the process of ending, as aggressive Central Bank actions of recent years are becoming increasingly ineffective. Despite massive quantitative easing programs in Japan and Europe, there is little improvement in growth. Instead, the main impact of their actions is evident in rising asset prices in government bonds, credit and equities.

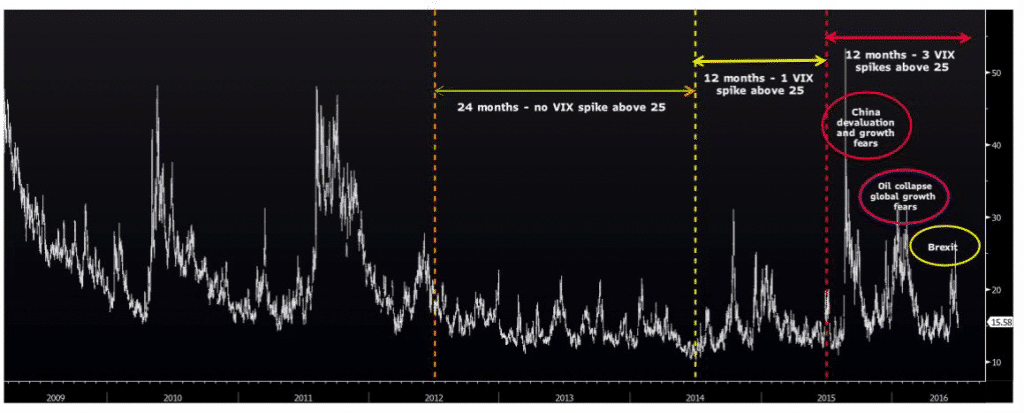

As markets sense the ineffectiveness of the interventions, volatility spikes in markets are becoming more common and more closely spaced. This is seen in the charts on the following page. Over the past year, there have been three spikes in the VIX index above 25, compared to just one in the preceding 12 months and none in the preceding 24 months before that.

Historical experience suggests that increasing frequency of volatility spikes after a prolonged low volatility period typically portend larger macro-economic regime changes or large market moves.

Between July 2007 and July 2008, the VIX spiked above 25 no fewer than five times. In the late 1990s, from July 1997 to July 2000, the VIX averaged just shy of 25 for the entire period as the Asian Crisis, Russia / LTCM Crisis, Y2K fears and finally the Technology Bubble burst.

The reversion of volatility to a more normal environment should provide a favorable backdrop for AQO. As volatility rises, the number of instances of volatility expansions should rise thereby increasing the opportunity set for AQO’s models.

Another benefit for a normalizing volatility environment is that it should be supportive of AQO’s focus on short term time horizons. In the low volatility trending markets of recent years, it was helpful to be more long term with increased holding periods. However, as volatility rises towards historical norms, the nature of price action may experience more frequent trend changes. AQO’s focus on shorter term horizons should enable our models to adapt faster to these changes relative to strategies with longer-term horizons. 4

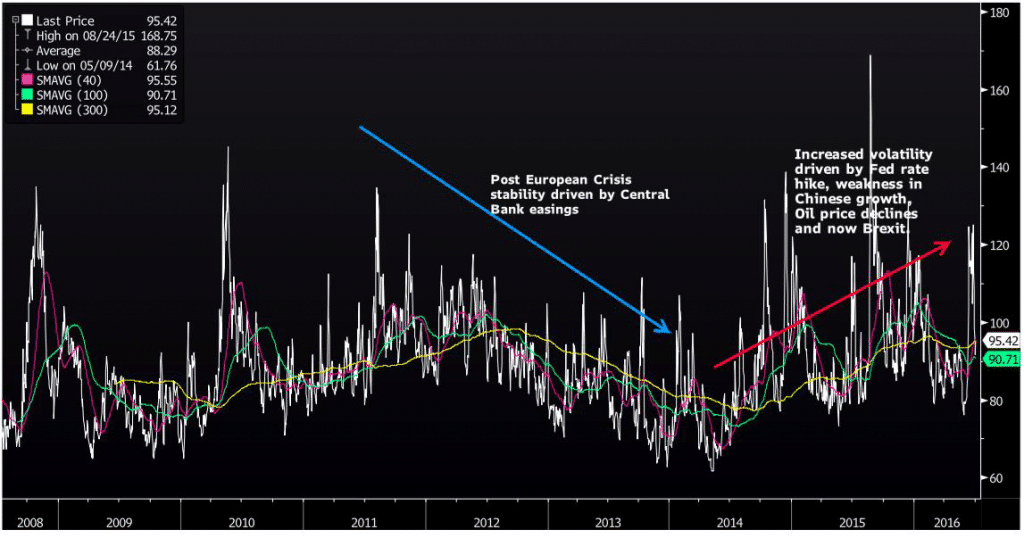

The VVIX Index, a volatility of volatility measure that represents the expected volatility of the 30-day forward price of the VIX Index, also shows similar trends.

VVIX Index

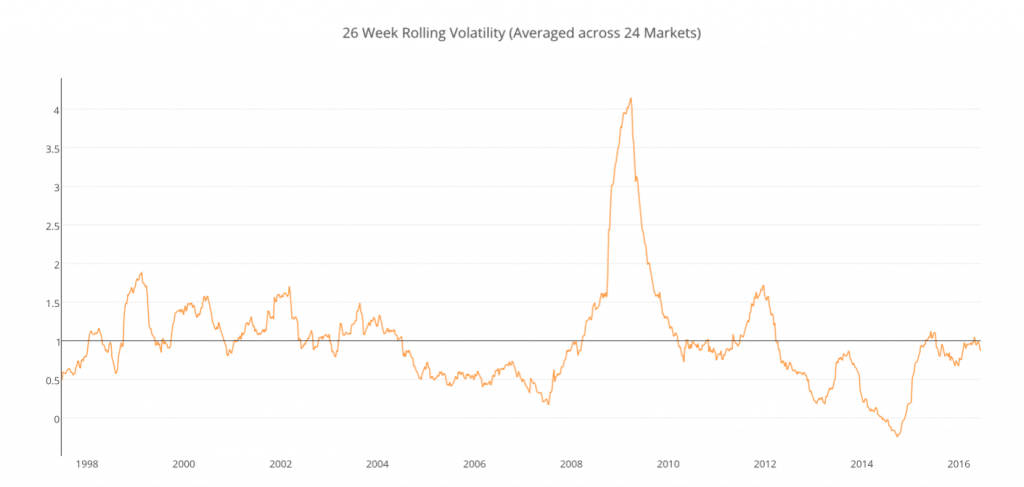

Quest’s proprietary indicators also suggest that volatility is recovering from the abnormally low levels that persisted in recent years but has only just reverted to historical averages.

Source: Quest Partners LLC

The chart above shows the normalized realized volatility across 24 markets in equities, currencies, commodities and bonds. As can be seen, realized volatility was steadily falling for a five-year period starting in 2009 through to late 2014. Since then, we have seen a recovery in realized volatility, but it has only come back to its average of the past eighteen years.

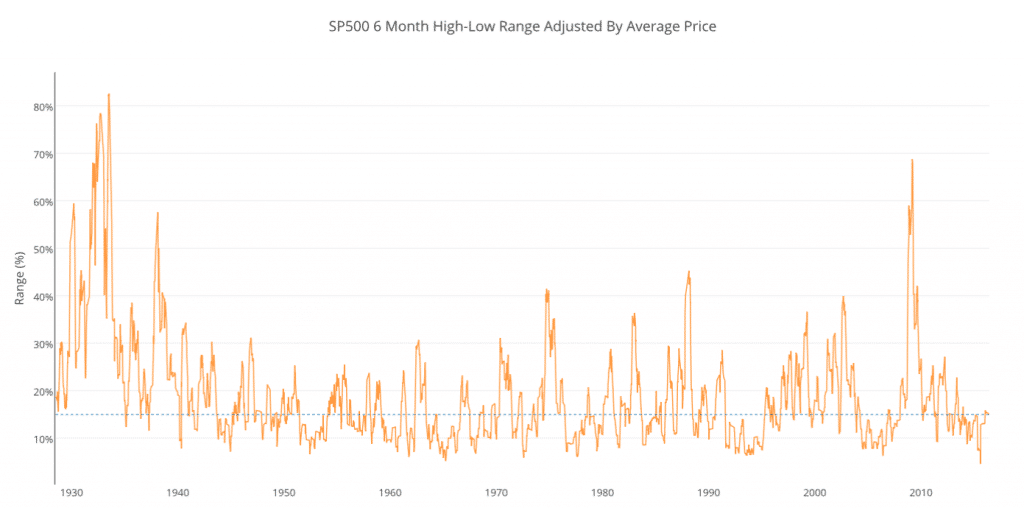

The chart on the preceding page is another proprietary indicator we track. It is the rolling 6-month range of prices for the S&P 500 divided by the average price of the index during the period. It gives a measure of how much the index moved during a given 6-month period.

The chart on the preceding page is another proprietary indicator we track. It is the rolling 6-month range of prices for the S&P 500 divided by the average price of the index during the period. It gives a measure of how much the index moved during a given 6-month period.

Similar to the earlier chart, it shows that price movements of the S&P 500 were steadily declining and were unusually compressed up to 2014-2015. It has only recently normalized to its historical average.

The key takeaway from these indicators is that while volatility over the past year appears to be high, we are just now back to historical averages. Only compared to the abnormally depressed volatility standards of recent years does the current level of volatility appear to be high.

In the world of volatility, we are not in a ‘new normal’ but only back to ‘the normal.’

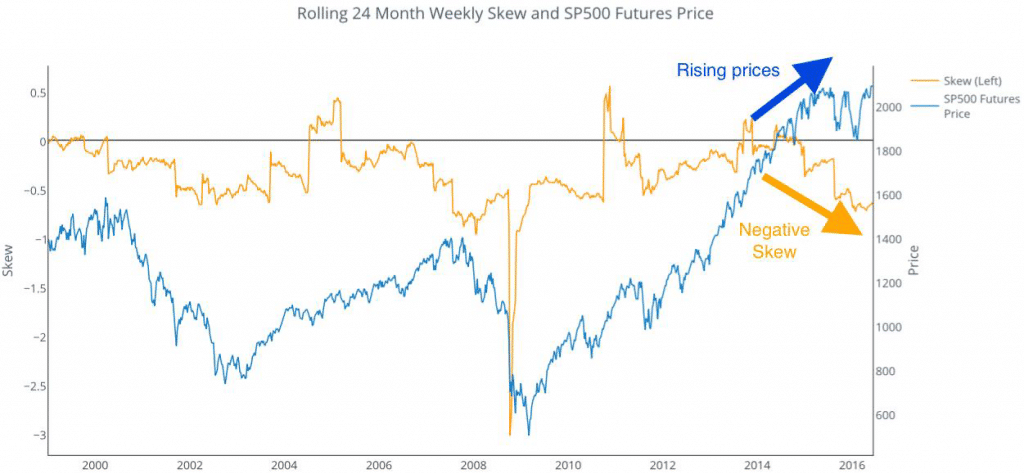

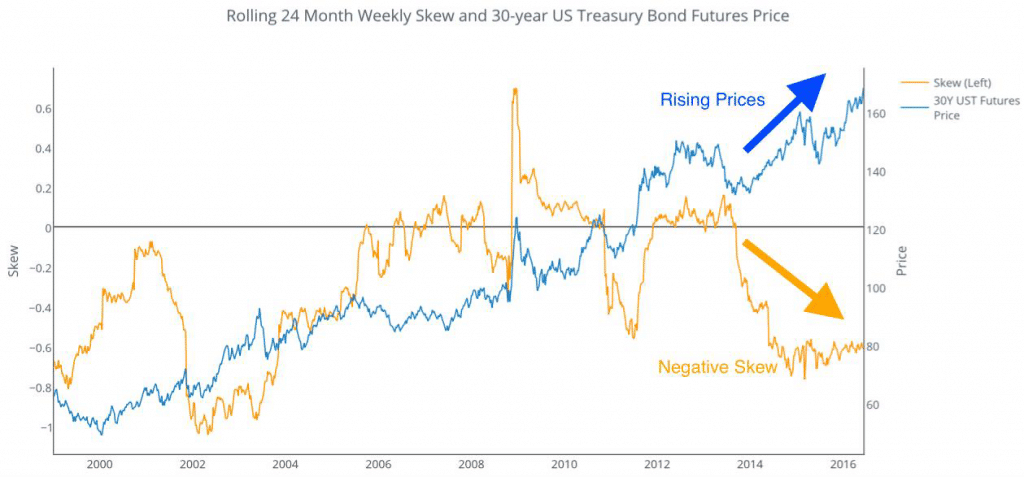

2. Rising Prices But Increasingly Negative Skew

One of the key risk indicators we look at is not just the standard deviation of prices, but also their ‘skew’. Skew is a measure of the asymmetry in a return distribution. A set of returns made up of frequent small, lower than average, returns and occasional large gains would be positively skewed. Conversely, a set of returns with frequent small, above average, returns and occasional large losses would be negatively skewed.

When prices of an asset are steadily rising but can occasionally be vulnerable to large declines, such an asset is said to be negatively skewed. Conversely, when an asset price is steadily falling but can occasionally have large gains, such an asset is said to be positively skewed.

Given the unprecedented intervention of Central Banks in supporting asset prices, many major asset classes are currently exhibiting negative skew, although their prices are at or near record levels. This implies that such asset classes are vulnerable to sharp declines or trend reversals if Central Bank support ends or is perceived to be ineffective.

These indicators highlight caution against ‘chasing beta’ in the current environment, especially in assets with negative skew characteristics, as the return relative to risk is poor.

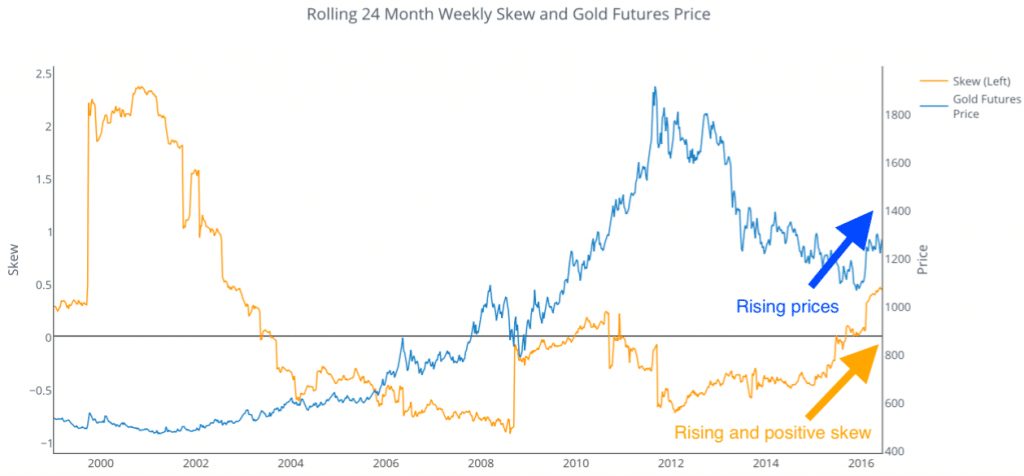

However, not all assets are exhibiting negative skewness. The chart below shows that Gold is exhibiting positive skew, indicating that it is more likely to have large gains than large losses.

The recent movements in Precious Metals markets bears close observation, as they have typically been a good indicator of market fear as well as precursor for potential volatility in fixed income markets. With a significant percentage of developed market sovereign bonds trading at negative interest rates, a steady rise in Precious Metals could result in an abrupt shift out of sovereign bonds, a move that could be exasperated by their negative skewness.

Given the extended nature of bull markets in a number of asset classes, we believe is it critical to pay attention to alternative measures of risk evaluation rather than simply focus on price momentum or standard deviation of returns, which may not capture the full extent of risks currently embedded in asset prices.

Judiciously trading in markets with more advanced tools and indicators will be key to generating alpha going forward.

We believe Quest’s models are well suited to take advantage of an environment of increased negative skewness and its potential for creating more trend reversals. Firstly, AQO’s (AlphaQuest Original) faster reaction times should be useful in dynamically adjusting exposures and capturing the moves as they develop. And secondly, our proprietary convexity filters should help identify markets where counter-trend moves are the most attractive.

AQO’s returns are in fact positively skewed and this is a key attribute from a risk perspective. As documented earlier, within the hedge fund industry the relationship between drawdown and volatility hinges on skew. The lower the skew, the higher the potential drawdown as a multiple of volatility. The same relationship holds within the CTA industry as well. For major funds, the correlation between volatility normalized drawdown and skew is significantly negative.

Hence, when evaluating funds it is quite helpful to focus not just on volatility and Sharpe ratio but also the skewness of their returns, which is an important indicator of maximum loss.

To learn more about Quest*, sign up for performance details and RCM’s due diligence notes here.

*Program available only to Qualified Eligible Persons (“QEP”), as that term is defined by CFTC Rule 4.7