For what seems to be the first time in what we can tell, there are other people out there warning investors of the dangers of Commodity ETFs. This week, the Financial Times beatifically outlined one of the many issues with these sort of products, such as $USO, $UNG, and $CORN.

Investors have learnt the hard way that many commodity ETFs do not work if held over long periods. The worldwide commodities glut not only depressed prices but pushed down many spot commodity prices compared to those for future delivery. This pattern, known as contango, ate up investors’ money as ETFs that owned futures effectively sold low and bought high each time they replaced expiring contracts with more expensive ones.

This is something we’ve been hammering at for years (see Commodity ETFs Suck as one ineloquent example), in hopes of saving one or two investors from buying an ETF in order to participate in rising prices (only to see the commodity price go up but their investment not keep pace). The gist is – commodity ETFs are good at tracking short term moves of the commodities they track, but lose effectiveness the longer the ETF is held. If we had efficient markets or rational investors, these ETFs would cease to be used for anything but capturing a 1 to 5 day move in a commodity. And the FT article echoes that sentiment, with multiple quotes and stats backing up the idea that they are being used mainly for short term exposure.

With average volumes of about 45m a day, the [USO] fund’s 287m shares outstanding turn over every six days.

“The holding period for levered products is typically very short,” says Nick Cherney, head of exchange products for Janus Capital Group, the parent company of VelocityShares.

“These ETFs have never been intended to be, ‘buy and hold’ investments and the companies offering them have been very clear on this provided you actually read the information given.” – Jesse Cates of Midland, Texas

But can inflows grow when it’s all short term trades? Wouldn’t that result in a netting out of flows? If you’re an ETF flow expert, please let us know, because it seems to us that an increase in assets means an increase in the amount of ETF shares being HELD, not just traded. And we’re talking some major flows of late – with investors hopping on the commodity train the heaviest in seven years in 2016, shoving $33 billion of new flows into commodities based exchange traded products.

Source: FT

Source: FT

So this all begs the question. What if you do want long-term exposure to a commodity price? What if you think oil is going back into the $100s sometime in the next few years? If the ETFs are just short-term instruments, how do you get that longer term exposure without suffering the consequences laid out in the FT article and our posts over the years? Well, quite simply – you can get direct exposure via futures, buying the futures contract yourself rather than through the ETF. This allows you to customize the time frame you’re looking to align with, instead of getting the ‘one size fits all’ approach of the ETF.

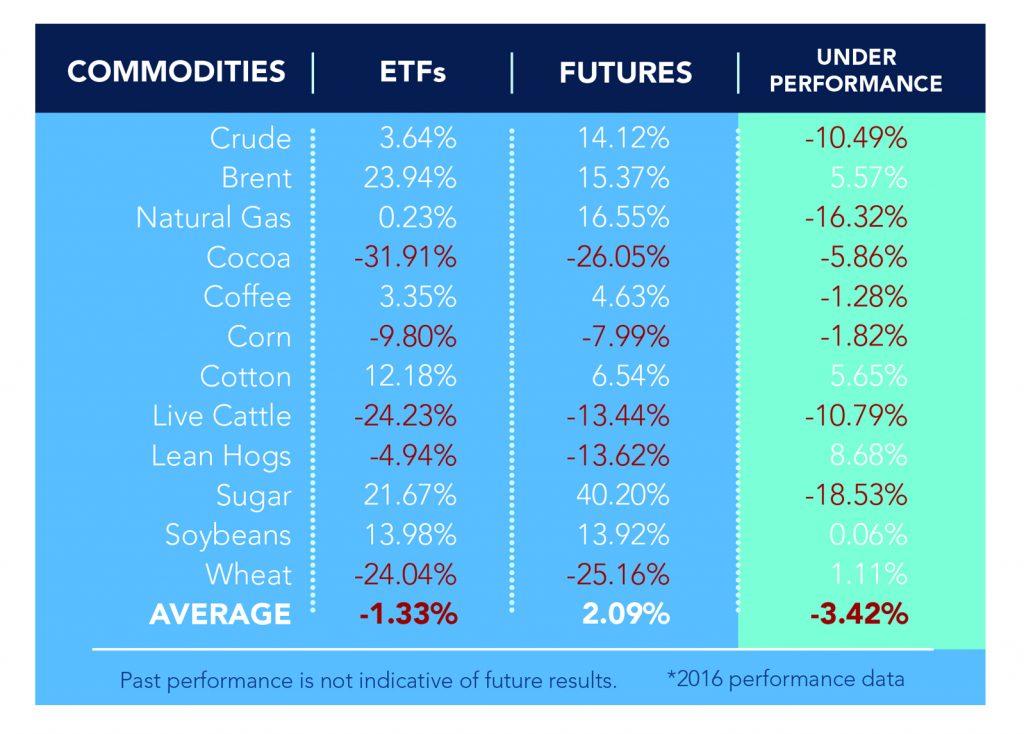

Say you want exposure to the annual price move of Crude Oil, you can simply buy the December futures contract one year out, and avoid the costs (when in Contango) of rolling the futures contract month after month. How’s that work across various commodities – take a look at this table showing various commodity ETF 2016 performance versus a simple strategy of owning the December 2016 futures contract (and rolling it to the Dec 17 contract before expiration – we used 10/31 for that).

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Sugar uses the October contract, Soybeans the November contract.)

Source: Barchart and Yahoo

Of course – we don’t think anybody should just be doing long only, buy and hold commodity exposure. A quick look at that strategy versus other asset classes shows it to be the asset class with the lowest returns and highest volatility. That’s not a good combo for the health of your portfolio, and not worth any ‘inflation protection’ you might get from commodity exposure. No. For us, it’s better to have dynamic and tactical exposure to commodity markets via Global Macro and Managed Futures investments. It’s better to be able to go long and short commodity prices. It’s better to have exposure to more than just energy markets. And it’s better to have systematic, focused risk control (did we mention commodity markets are volatile). To learn more information on this sort of approach, click here to download our whitepaper, “Why Alternatives.”