The entirety of the Managed Futures industry has had a tough go in recent years. Despite strong 2014 performance numbers, the asset class has accepted small consistent losses waiting for volatility to expand since then – and as we can see from the ever present articles about the VIX hitting all time lows – that’s been one hell of a wait.

Bloomberg’s latest article on the space attempted to look at this link – but misses the mark by quite a bit – comparing managed futures returns to volatility by running a correlation analysis on managed futures average 3 year percent return versus the average 3 year price of the volatility index (from what we can tell and recreate – Bloomberg’s policy is to not share its data calculations for its charts). Returns versus price is a weird way to calculate a correlation – in our opinion. It isn’t telling us anything about the relationship between increasing volatility and managed futures returns, it’s just telling us how three year returns compare to three year average volatility index prices (which over three year periods are going to include a lot of small values, as it is a decaying price type of index). As an example, if you test the correlation between the price of the S&P 500 and the returns of that same index (the monthly percent gains/losses implied by those prices) – you get a correlation of 0.04 !!

Here are Bloomberg’s results:

Here’s that same chart when you look at the 3yr change in price of the volatility indices (whether it’s rising or falling), and the change in price (returns) for the managed futures index, which shows quite a high correlation between the volatility index three year price differences (whether it has risen or declined across those three years) and managed futures performance over the three years on a rolling basis.

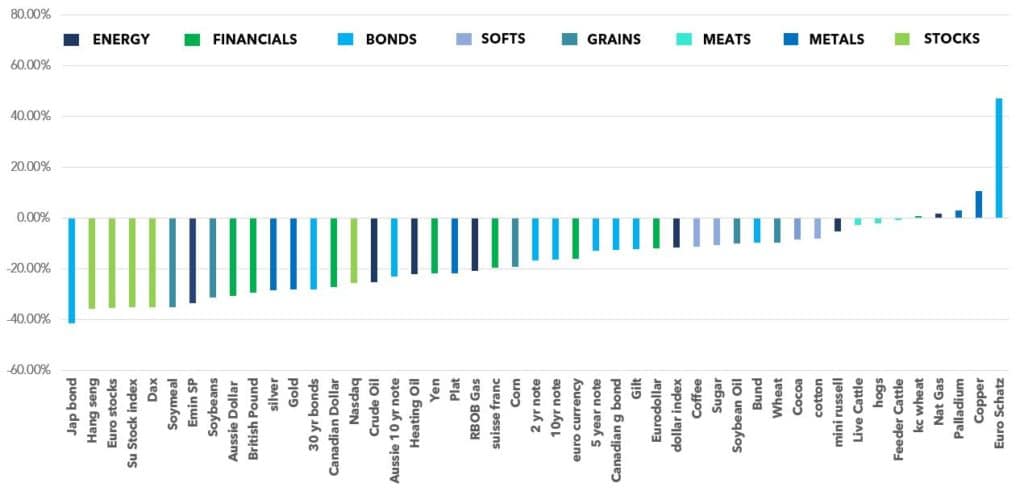

And of course, there’s our annual look at the expansion and contraction of volatility in the various markets Managed Futures actually trades. It just so happens we do this in our annual Managed Futures overview, specifically, measuring the average daily true range from one calendar year to the next calendar year, seeing which markets saw their average ranges (the kind of volatility managed futures care about) expand or contract. Given managed futures struggles this year, we would expect most markets to have seen a contraction in their volatility/ranges -and boy have they. We ran the data for the first six months of 2017, and a whopping 89% of the markets experienced consolidation over the first six months of 2017, leaving only five markets that expanded. The average volatility movement in the markets was -17%. Here’s a look at each of the market’s contraction and expansion.

Managed Futures has been called out before for only liking “the right kind of volatility,” and what is meant by that is directional movement upward or downward in various markets for Managed Futures to capture. But right now, it feels like we would take any kind of volatility – with this current rate of low volatility expansion having 2017 on track for the lowest percentage of expansion since 2012. On the other hand, considering Managed Futures are only down -2.86% throughout the first half of 2017 given the thing they are betting on is noticeably absent – it’s not as bad as it could be. And of course, the contrarian will point out that with futures markets contracting more than expanding going on three straight years, we could be on the verge of another pop. To read more about what we could see for Managed Futures in the remainder of the year, click here to download our Managed Futures 2017 Outlook.

Want to learn more about VIX? Click here to download out VIX Whitepaper.