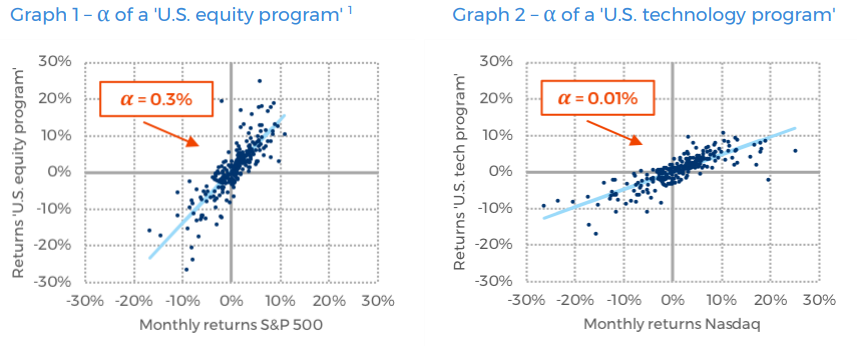

The good folks over at Transtrend (the 12th largest managed futures program in our top 100 managers infographic) are out with a new research piece via the CME that throws the whole Alpha concept out the window. They agree with the classical definition of Alpha as the amount of return not explained by the chosen beta benchmark, but argue somewhat convincingly that it doesn’t mean that Alpha equals skill, that just means we haven’t really identified the correct benchmark (or portfolio of mixed benchmarks/betas) in which to compare returns to. Here’s some of their proof, showing two Alphas that could be marketed as manager skill:

But, then they tell us these aren’t skill at all. The left hand graph is actually just the Nasdaq plotted over the S&P returns, and the right hand graph the S&P over the Nasdaq. There’s no skill there, they argue, just a mathematical value of how much one data set doesn’t fit with the other data set. They expand that thought to essentially say there is no such thing as positive Alpha, only the ability in which to capture betas, with all Alpha being negative Alpha reflecting the success with which a manager has in capturing his or her selection of various betas. Here’s their clever analogy:

Health is nothing but the absence of injury and disease. One may strive to avoid injuries and diseases, but one cannot acquire health. The same holds for alpha in investing: one may strive to avoid negative alpha, but no pharmacy or investment strategy is able to deliver positive alpha.

We’re not sure what Transtrend’s end game is here, exactly; but this all comes back to why manager selection is so difficult. Something we wrote about way back in 2007 and 2012:

The problem inherent in the difficulties of alternative manager selection is that investing in Alpha often means you will lack a reliable Beta. While Beta may seem like an advanced statistical concept – most of us feel Beta whenever we look at our overall portfolio’s performance. We may see that our portfolio of mutual funds was down in the third quarter, but not feel so bad because they were down less than the overall market. We may see that our high flying growth stock lost 3 times what the market as a whole did last Friday, but comfort ourselves by recalling that the stock had risen many times more than the overall market thus far this year.

We also feel Alpha – with thoughts such as “I’m dropping this mutual fund because its underperforming the overall market.,” So while not putting fancy calculations on paper with Greek symbols and figuring what your investments’ Alphas and Betas are, most people can intuitively work out what the Alpha and Beta are for their STOCK and BOND portfolios. This is because they can feel the differences in return and volatility between any single investment and the overall stock or bond markets

This ability to intuitively work out Alpha and Beta starts to fall apart when entering the alternative investment world and the often complex and diverse portfolios and multiple strategies employed by hedge funds or managed futures programs. In short, finding a reliable benchmark (a Beta measure) for these kinds of investments is difficult. You may look at the S&P 500 when evaluating the returns of a mutual fund over time, or a government bond index if you’re investing in a fixed income program, but if you’re investing a managed futures program that can go long or short in dozens of commodity, financial and currency markets, what exactly does that line up with? The answer: it’s complicated.

The problem many of those in charge of doing manager selection run into, therefore; is one of understanding (without the normal Alpha/Beta framework) exactly how a manager has achieved their past performance. This impact is amplified in the black box world of hedge funds, where transparency is often a dirty word.

Does that mean you should avoid these kinds of absolute return investments? No. The problem, going back to the Alpha/Beta conundrum, becomes the selection process. Ritholtz likes to talk about the importance of process when it comes to managers- the importance of relying on methodology over luck. In our opinion, that process is just as important, if not more so, when it comes to manager selection.

And that comes back to working with the right people – and our solution. Manager selection isn’t easy. In managed futures in particular, there are dozens of elements that need to be considered and continuously monitored. You’re looking at performance, but you’re also looking at the ins and outs of the strategy, risk profile, manager experience, back office functionality, and much more to arrive at a measure of what the ‘Beta’ should look like for each manager. Some of this is quantifiable, and some of it isn’t. And it’s not enough for that kind of research to be a one and done type process. If you want to protect yourself from things like strategy drift or other unfavorable circumstances, these things need to be checked constantly. Do you have the time for that?

Realistically, the ability of family offices and investment advisers to conduct this ongoing due diligence on their own, especially in a world with thousands upon thousands of investing opportunities in the absolute returns arena, is limited. Each kind of strategy would require specialized knowledge for evaluations. Unless the family office or adviser you work with has a massive staff under them (and sometimes, even if they do), selecting managers is going to be difficult…unless they work with a firm that specializes in that space and has developed that ever important process.

In other words, manager selection IS difficult, because of the issues outlined by Transtrend with Alpha and Beta. But if you’re working with the right people to identify what the actual return drivers are (another word for Beta) for each strategy, it doesn’t have to be insurmountable.

PS – This 2013 piece from Transtrend is still pretty relevant today: Fat Tails and Tall Heads.