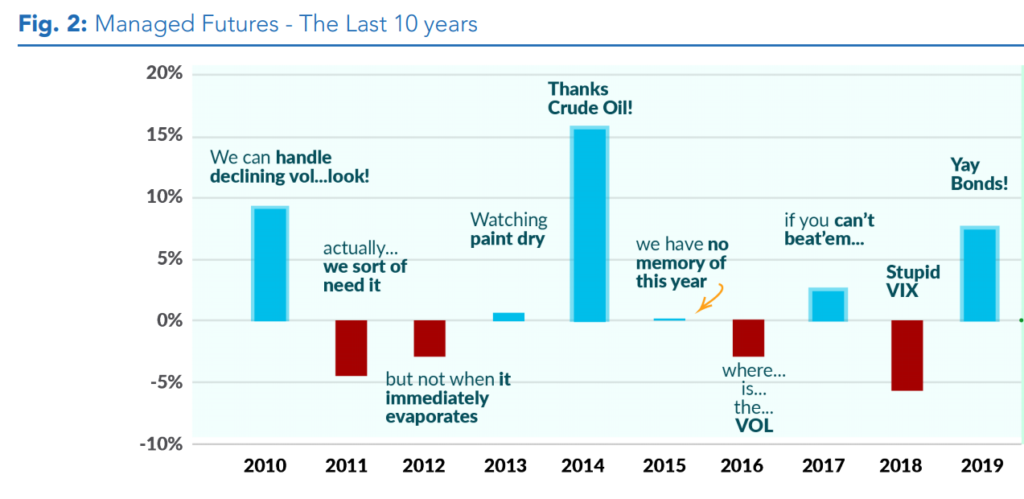

Our own Jeff Malec relayed a story on a recent podcast (if you haven’t checked our The Derivative yet…get on over there) about telling his 10 year old son that “we’ve been in drawdown your whole life”. He was referring to managed futures, of course, and this rather un-even, lumpy, lots of flat/red bars chart from our 2020 outlook.

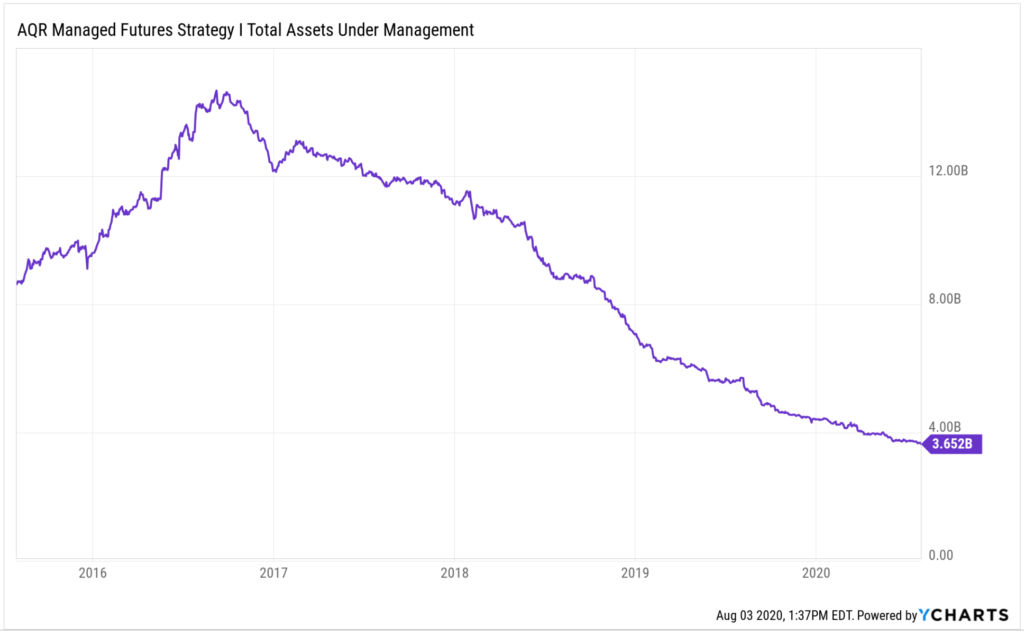

How do investors feel about managed futures right about now? Well, the good folks over at AQR made a managed futures product so popular at its height that it acts as a great proxy for answering that question. Here’s AQR’s managed futures mutual fund’s asset flows as proof that managed futures is not so en vogue right now. That’s about $10 Billion in outflows over 4.5 years. Ouch.

I Don’t Like the Taste

Now, AQR has had it’s own issues with their managed futures product and trailing peers. But, this isn’t about them. Their fund didn’t become less ‘managed futures-ish” over this time. It’s about investors chasing that performance, and not having the fortitude to stick with a diversifier when it is diversifying in a seemingly wrong way – losing when the stock market is going up. Investors (on the whole) no longer like the ‘taste’ of their managed futures medicine. It’s too path dependent, or too unpredictable, on how and when it delivers the negative correlation in down markets – sometimes doing it on a short term basis, sometimes not.

Bring on the Sugar

So, what do you do? Ditch the asset class and its well known crisis period performance and ability to capture breakouts like Silver which come out of nowhere? That sounds a bit like throwing the baby out with the proverbial bathwater, and not the smartest of ideas for a well balanced portfolio. No, a new crop of mutual fund managers have a better idea to allow you to get that bad tasting medicine down the old hatch. Let them add the “Sugar” beta to the diversifying managed futures Alpha in a single product for you. Let them take away the line item risk, whereby you keep seeing that flat/losing asset and question why it is in there. Let them solve for your emotional biases by burying that flat performance into the overall product, delivering a combination that aims to come out better than the single ingredients look on that statement.

Here’s a handful of new mutual funds going down this intriguing path:

Standpoint Multi-Asset Fund = Global Equities & Managed Futures

Standpoint blends 50% Global Managed Futures via a trend following approach with 50% Global Equities via a suite of ETFs.

YTD: +4.50%

Website

Morningstar

Podcast

Rational Equity Armor Fund = Dividend Paying Equities & Tail Risk Protection

Equity Armor Investments partnered with Rational Funds to take over this mutual fund at the end of last year, putting into place their strategy of a core long holding of dividend paying stocks inside of the S&P 500 and up to 20% in a VIX replication strategy designed to provide as much pop as possible during a sell off with as little bleed as possible the rest of the time.

YTD: +10.48%

Website

Morningstar

Podcast

Catalyst Multi-Strategy Fund = Fixed Income & Managed Futures

Caddo Capital Management took over control of this fund in January 2018, implementing a different approach to the original fund – by blending fixed income investments across bonds, MBS, CLOs, CDOs, and more – with the more traditional trend following managed futures component.

YTD: -1.81%

Website

Morningstar

*YTD performance numbers as of 8/2/2020 per YCharts.com*

PS – speaking of AQR, here’s are past views on “what’s wrong with AQR”