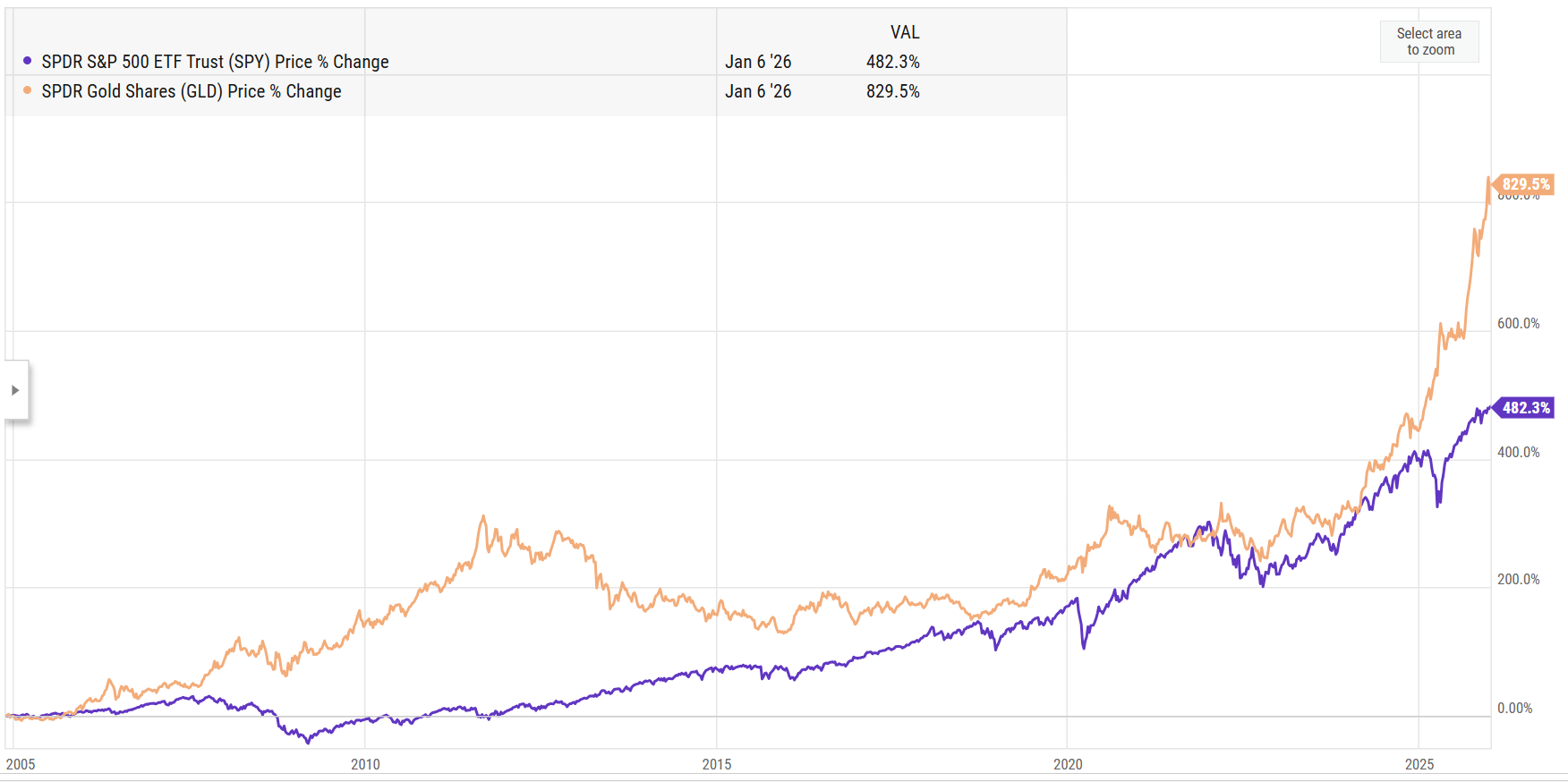

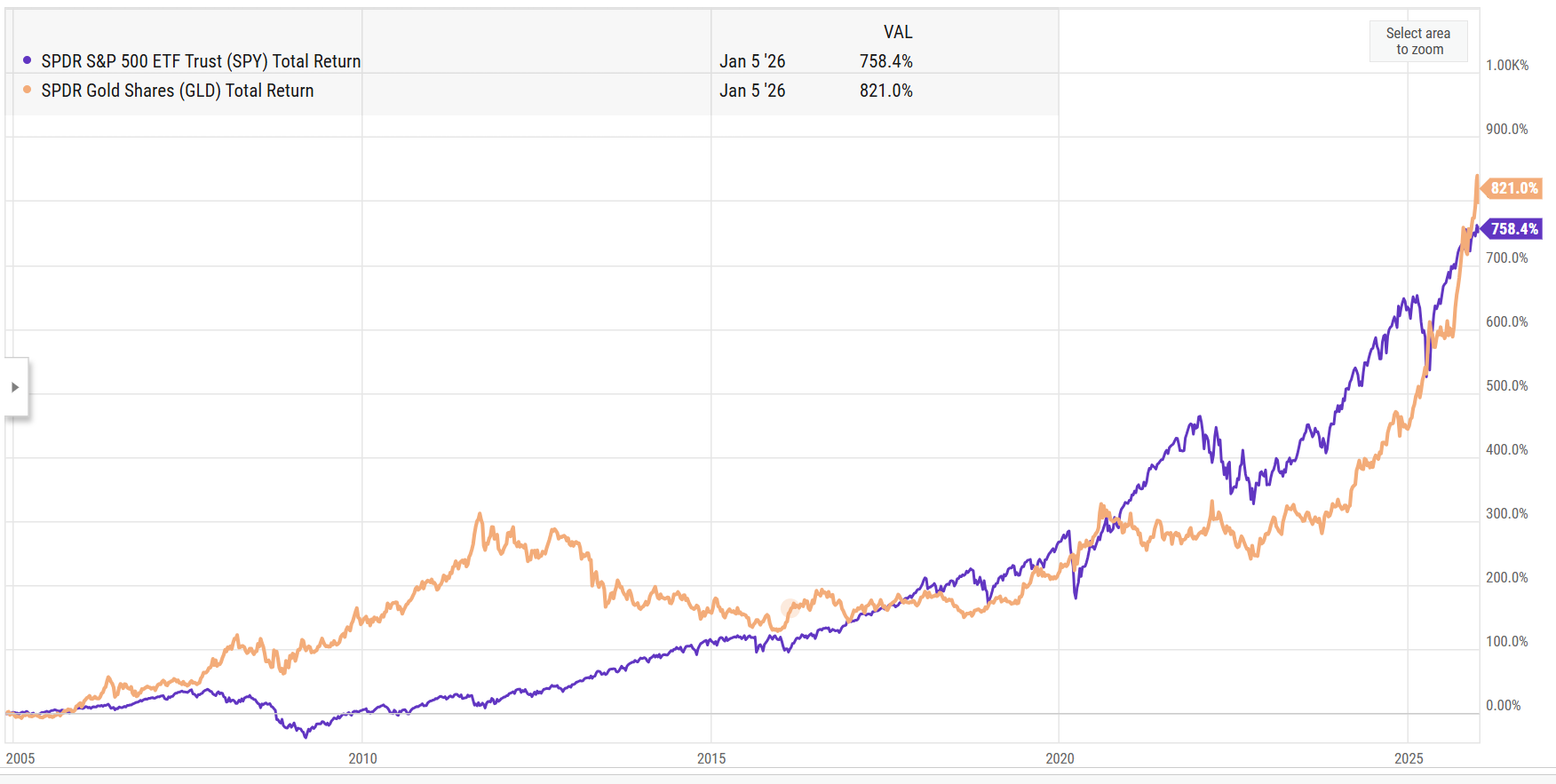

Gold has had a remarkable run in 2025, and that performance has spawned a fresh wave of articles proclaiming that gold has outperformed stocks over 20- and 30-year periods. The headlines are eye-catching, and the underlying data isn’t fabricated. But here’s the nuance that often gets buried: most of that outperformance is price-based. On a total return basis—factoring in dividends reinvested for equities—gold still comes out ahead in some of these comparisons, but the margin shrinks considerably. Gold doesn’t pay dividends or buyback shares; over long horizons, that compounding gap matters.

Source: YCharts

Source: YCharts

Will the rally continue? No one knows. Gold could keep climbing, or it could give back a chunk of these gains. That’s not a prediction we’re in the business of making.

What we can say is this: If you’ve decided gold belongs in your portfolio, whether as a hedge, a diversifier, or a macro bet, the how matters just as much as the whether. The vehicle you choose shapes your costs, tax treatment, liquidity, and ultimately how much of your return is siphoned off before it ever reaches you.

Those choices are not interchangeable. Futures, ETFs, miners, coins, and bars each carry distinct trade-offs that rarely get laid out side by side.

Below we break down the main access points: physical coins, physical bars, gold ETFs, gold miners, and gold futures. We’ll also cover a final twist that rarely appears in retail gold guides: using gold warehouse receipts to fund a futures account—something we touched on in our SMA platform piece, and a structure that illustrates just how differently institutional gold markets operate.

Why Gold’s Run-Up Has a Logical Backdrop

Gold’s latest surge isn’t just narrative; there are real structural drivers.

Record central bank buying has been a defining feature of this cycle. The World Gold Council reports that central banks purchased over 1,000 tonnes of gold in both 2022 and 2023, the highest two-year level on record going back to 1950, driven largely by emerging markets diversifying away from U.S. dollar reserves (World Gold Council, Gold Demand Trends 2023). That trend has continued into 2024 and 2025.

Investor flows have also shifted. After extended periods of net outflows, gold ETFs saw renewed inflows during spikes in macro stress, underscoring gold’s role as a “financialized” safe haven (World Gold Council, Gold ETF Flows). The 2025 rally has accelerated this dynamic considerably.

Finally, real rates and policy credibility continue to matter. Research has repeatedly shown that gold is negatively correlated with real interest rates; when investors doubt central banks will maintain meaningfully positive real yields, gold tends to benefit (Erb & Harvey, “The Golden Dilemma,” Financial Analysts Journal, 2013).

So the interest in gold isn’t irrational. But how you implement that view is where many portfolios go off the rails.

Access Point 1: Physical Gold Coins—The Retail Trap

For most people, “buying gold” still means coins: American Eagles, Maple Leafs, Krugerrands, and the like. There are valid reasons to hold small amounts of physical metal—extreme tail risk, distrust of financial intermediaries, personal preference—but from an investment perspective, coins are usually one of the least efficient options available.

The Real Costs of the Coin Trade

The first issue is wide and opaque markups. Bullion coins trade at a premium to spot gold. In normal markets, common bullion coins often carry premiums in the 3–8% range over spot for small quantities. During crisis periods, when retail demand spikes and supply bottlenecks appear, those premiums can surge dramatically. Surveys and industry reports after the 2008 and 2020 episodes documented premiums on U.S. Mint bullion coins rising well above normal levels as dealers rushed to ration inventory (Nathan, “Bullion Coin Premiums in Crisis Markets,” Journal of Financial Planning, 2010). You’re typically down several percent the moment the trade settles—before gold even moves.

The second problem is liquidity that doesn’t scale. Selling a handful of coins is straightforward enough. But offloading a large physical position quickly and at tight spreads is another matter entirely. You’re negotiating with coin shops and dealers, not hitting a deep electronic order book. You face shipping, insurance, and authenticity verification—especially for larger transactions. For institutional allocations or even serious high-net-worth positions, that’s clunky at best.

Third, storage, security, and insurance add friction. With coins, you either pay a professional vault or depository (adding recurring cost) or become your own security operation—safes, secrecy, insurance policies, and so on. Those expenses chip away at returns compared with more scalable structures.

Fourth, tax treatment in the U.S. is unfavorable. Physical gold is typically categorized as a collectible, meaning long-term gains can be taxed at up to 28%, compared to the 20% maximum long-term rate on stocks and many other assets (IRS Publication 544; IRS guidance on collectibles).

So the coin trade delivers higher tax rates, wider spreads, and storage headaches. For a small doomsday stash, coins might serve a purpose. For a meaningful investment allocation, the coin trade is usually an expensive, inefficient way to own gold.

Access Point 2: Physical Gold Bars—A Step Up, But Not a Panacea

Gold bars represent a more serious approach to physical ownership than coins, and for larger allocations they offer meaningful advantages. But bars come with their own trade-offs that investors should understand before assuming they’ve escaped the inefficiencies of the retail coin market.

The Case for Bars Over Coins

Lower premiums per ounce represent the primary advantage. Because bars involve less fabrication, packaging, and handling per unit of gold, premiums over spot are typically tighter than coins—often in the 1–3% range for widely recognized bar sizes from established refiners, compared to 3–8% or more for coins. For investors deploying meaningful capital, that spread savings compounds into real money over time.

Bars also scale more efficiently. A single 1-kilogram bar (approximately 32.15 troy ounces) or a standard 400-troy-ounce “London Good Delivery” bar consolidates ownership into fewer physical units, reducing per-ounce storage costs and simplifying inventory management. Institutional investors and central banks hold bars, not rolls of Eagles, for precisely this reason.

Standardization matters as well. Bars from LBMA-accredited refiners (such as PAMP, Valcambi, Heraeus, or the Perth Mint) carry recognized hallmarks, assay certificates, and serial numbers that facilitate verification and resale through established dealer networks and, in some cases, direct access to wholesale markets.

The Limitations Bars Don’t Solve

Even with these advantages, bars retain most of the structural drawbacks inherent to physical gold ownership—and introduce a few new wrinkles.

Authenticity and chain-of-custody concerns grow with bar size. While coins can be tested relatively easily with basic tools, larger bars require more sophisticated verification (ultrasound, X-ray fluorescence, or other assay methods) to ensure they haven’t been adulterated or counterfeited. Once a bar leaves an accredited vault or breaks its chain of custody, re-entering the institutional market often requires expensive re-assaying. This “good delivery” problem means bars held privately may trade at discounts when sold, or face friction returning to wholesale channels.

Liquidity remains dealer-dependent. You’re still selling to dealers, not into a deep electronic market. While premiums are tighter on bars than coins, bid-ask spreads at the retail level remain wider than ETFs or futures, and large liquidations can still be cumbersome. The wholesale London gold market is highly liquid—but retail investors don’t have direct access to it.

Storage and insurance costs persist. Bars must be stored securely, whether in a home safe, a bank safe deposit box, or a professional vault. Vault storage fees typically run 0.1–0.5% of value annually depending on the provider, plus insurance. These costs erode returns in ways that don’t appear on a simple price chart.

Divisibility is poor. If you own a single 1-kilo bar and need to raise a smaller amount of cash, you can’t peel off a few ounces—you must sell the entire bar or find a dealer willing to buy back a portion (which often doesn’t happen cleanly). Coins, for all their inefficiencies, offer more granularity.

Tax treatment remains unfavorable. Like coins, bars are classified as collectibles for U.S. tax purposes. Long-term capital gains face the 28% maximum rate rather than the 20% rate on most other long-term investments. This structural tax drag compounds over time and can meaningfully erode after-tax returns versus more tax-efficient vehicles.

When Bars Make Sense

Gold bars are best suited for investors who want meaningful physical exposure—tangible metal they can hold, audit, and store outside the financial system—but who are deploying enough capital that coin premiums become unacceptable. They’re also appropriate for those planning to hold metal in professional vault storage with established chain-of-custody protocols, where re-entry to wholesale markets remains possible.

For investors who prioritize liquidity, tax efficiency, or capital flexibility, bars still fall short of ETFs or futures. Physical metal is physical metal: you’re paying for tangibility, and that comes at a cost.

Access Point 3: Gold ETFs—The “Easy Button” for Most Investors

For many investors, gold exposure simply means a ticker symbol. The major physically backed ETFs include SPDR Gold Shares (GLD), iShares Gold Trust (IAU), and abrdn Physical Gold Shares (SGOL). These funds are designed to track the spot price of gold by holding vaulted bullion, with shares representing fractional ownership.

Why ETFs Work (Mostly)

Simplicity is the primary appeal. You trade these like any stock in your brokerage account—no vault contracts, no shipping, no insurance hassles. Liquidity is excellent; GLD is one of the largest and most actively traded ETFs in the world, with deep liquidity and penny-wide spreads in normal conditions. Authorized participants can create and redeem shares against physical gold, helping keep the ETF price close to net asset value.

Ongoing costs are also reasonable. Expense ratios run approximately 0.40% for GLD, 0.25% for IAU, and 0.17% for SGOL (fund fact sheets; SPDR, iShares, abrdn). That’s far cheaper than paying 5–10% round-trip in coin spreads plus storage.

The Hidden Trade-Offs

Fee drag compounds over time. Even 0.25–0.40% per year adds up. Over a decade or two, that’s several percentage points of return lost relative to spot, all else equal.

U.S. tax treatment is often still problematic. Many gold ETFs that hold physical bullion are taxed like collectibles, just like coins—long-term gains subject to a 28% maximum rate instead of the usual 20% for most long-term capital gains (IRS Publication 544; see gold ETF tax disclosures in GLD and IAU prospectuses).

Finally, ETFs offer no inherent leverage. If you want more than 1:1 exposure, you must use margin in your brokerage account or turn to leveraged products, which bring their own complications.

ETFs are a significant step up in efficiency versus physical gold for typical investors, but they remain a relatively blunt tool—especially for allocators who care about capital efficiency, global collateral optimization, and more nuanced tax outcomes.

Access Point 4: Gold Miners—An Indirect, Levered, and Messy Bet

Another popular way to “play gold” is through gold mining stocks, via individual equities or sector funds like VanEck Gold Miners ETF (GDX) and VanEck Junior Gold Miners ETF (GDXJ). These are equities, not commodities—and that distinction matters enormously.

Why Miners Attract Capital

In theory, miners offer leveraged exposure to gold. If a miner’s costs are relatively fixed, each dollar increase in gold’s price flows disproportionately to the bottom line. That can translate into equity returns that are more volatile—and, in bull markets, potentially higher—than the metal itself (Fabozzi, Fuss & Kaiser, The Handbook of Commodity Investing, Wiley, 2008). Miners also offer equity-specific upside: dividends, share buybacks, M&A activity, and operational improvements can add value beyond gold price moves. Standard equity tax treatment often applies, rather than the collectibles rules.

The Big Catch: You’re No Longer Just Betting on Gold

Owning miners introduces a stack of non-gold risks. Management and capital allocation decisions matter—poor discipline through dilution or overpriced acquisitions has historically destroyed shareholder value across the sector. Cost inflation in energy, labor, equipment, and environmental compliance can eat into margins even when gold rises. Geopolitical and jurisdiction risk is substantial since many reserves sit in politically unstable or high-risk regions. ESG pressures and permitting delays can hammer stocks independent of gold’s price.

Empirically, this has often meant that miners are more volatile than gold and do not reliably outperform it over long horizons, despite their theoretical leverage (Fabozzi et al., 2008; multiple practitioner analyses confirm this pattern).

Gold miners can be useful as a tactical satellite position or as part of a broader resources and equity sleeve. But they are not a clean proxy for gold itself. If your goal is to hedge macro risk or own a monetary asset, miners are a noisy way to accomplish it.

Access Point 5: Gold Futures—Clean, Capital-Efficient, and Institutional-Grade

Gold futures—like the COMEX contracts traded on CME Group—are the tool of choice for many professional traders, hedgers, and institutional allocators. They provide direct exposure to gold with powerful capital efficiency and robust market structure.

Why Futures Are So Powerful

Capital efficiency is the standout feature. A standard COMEX Gold (GC) futures contract controls 100 troy ounces of gold, with margin requirements that represent a fraction of the full notional value. Exact levels are set by the exchange and your Futures Commission Merchant and vary over time (CME Group, COMEX Gold Futures Contract Specifications). This allows you to deploy notional exposure that is multiple times your cash outlay, freeing up capital for other investments or collateral uses. No coin dealer can offer anything remotely comparable.

Deep, regulated liquidity is another advantage. Gold futures trade nearly 24 hours a day, five to six days a week, on regulated exchanges. Central clearing means the clearinghouse stands between every buyer and seller, dramatically reducing counterparty risk (CME Group documentation). Tight bid-ask spreads and deep order books support large, fast executions. This is global, institutional liquidity—not someone’s weekend coin shop.

Futures also offer clean price exposure. Prices reflect spot gold plus or minus carry costs (interest rates, storage, and convenience yield). In normal conditions, that relationship is well understood and tightly arbitraged. You don’t deal with retail dealer markups or premiums and scarcity squeezes on specific coin products.

U.S. tax treatment provides an additional edge. For U.S. investors, regulated gold futures are typically Section 1256 contracts: marked to market at year-end, with gains and losses taxed as 60% long-term and 40% short-term, regardless of how long you held the trade. The effective tax rate is often lower than pure short-term treatment (IRS Publication 550, “Section 1256 Contracts and Straddles”). For active trading or systematic strategies, this is a meaningful advantage over many other high-turnover approaches.

The Drawbacks

Leverage cuts both ways. The same leverage that makes futures efficient also amplifies losses. A modest percentage move in gold can translate into large swings relative to posted margin. Operational complexity is also higher—you handle contract months, rolls, margin calls, and FCM relationships. That’s why many investors use professional Commodity Trading Advisors (CTAs) or institutional platforms to implement futures-based gold exposure.

Still, for those comfortable with the infrastructure—or who delegate it—futures are often the cleanest and most capital-efficient way to get price exposure to gold.

A Hybrid Approach: Return Stacked ETFs

For investors who want gold exposure but don’t want to sacrifice equity returns to get it, a newer category of products has emerged that attempts to solve the traditional either/or problem.

Return Stacked ETFs—like BTGD (Return Stacked Bonds & Gold ETF) and RSSX (Return Stacked Global Stocks & Futures Yield ETF)—use capital-efficient derivatives to layer multiple asset class exposures on top of a single dollar invested. The concept is straightforward in theory: instead of choosing between stocks and gold (or bonds and gold), you can own both simultaneously through a structure that uses futures and swaps to achieve notional exposure exceeding 100% of assets.

How Stacking Works

The mechanics rely on the same capital efficiency that makes futures attractive. Because futures require only margin—not full cash outlay—a fund can hold, say, Treasury exposure via futures while simultaneously holding gold exposure via futures, all backed by the same pool of collateral. The result is a portfolio that might deliver something like 100% bond exposure plus 100% gold exposure in a single ticker, or equity exposure plus trend-following plus gold in a combined wrapper.

For advisors and allocators, this solves a practical problem. Traditional portfolio construction often treats gold as competing for allocation space with equities or bonds. If you add 10% to gold, you’re implicitly taking 10% from something else. Return stacking attempts to sidestep that trade-off by using leverage at the fund level to provide additive exposure rather than substitutive exposure.

The Trade-Offs

These structures aren’t free. Embedded borrowing costs matter—when a fund uses derivatives to achieve leverage, it’s implicitly paying financing costs that can drag on returns, particularly in higher-rate environments. Complexity is higher than a plain-vanilla ETF; you’re trusting the fund manager to execute rolls, manage counterparty exposure, and maintain the targeted notional exposures through varying market conditions. Tracking and rebalancing behavior may differ from what you’d experience holding the underlying assets directly.

Tax treatment varies by fund structure and the specific instruments used. Some return stacked products may pass through the favorable 60/40 treatment on futures gains; others may not, depending on how they’re organized. Prospectus review is essential.

Finally, leverage amplifies both gains and losses. In a scenario where both your equity (or bond) exposure and your gold exposure decline simultaneously, a stacked product will experience larger drawdowns than an unleveraged single-asset holding. The diversification benefit of gold depends on it behaving differently from your other exposures—when correlations spike, stacking magnifies pain rather than cushioning it.

When Return Stacking Makes Sense

Return stacked products are most compelling for investors who have already decided they want gold exposure and don’t want to fund it by selling equities or bonds. They’re also useful for advisors managing tax-sensitive accounts where realizing gains to rebalance into gold would trigger unnecessary tax events.

For investors who are comfortable with the embedded leverage and complexity, products like BTGD and RSSX offer a way to access gold’s diversification potential without the opportunity cost of reducing exposure to other return-generating assets. They represent an institutional-style approach packaged for retail and advisor channels—though, as always, understanding what you own and how it behaves under stress is essential before committing capital.

Pulling It Together: Choosing the Right Gold Access Point

Each vehicle serves different purposes and carries distinct trade-offs.

Coins offer tangibility, portability, and existence outside the financial system. But they come with wide spreads (often 3–8% or more), storage and security burdens, collectibles tax treatment (up to 28% in the U.S.), and liquidity that becomes problematic at scale. They’re best suited for a small “prepper” or sentimental allocation—not a core investment position.

Bars improve on coins with tighter premiums (typically 1–3%) and better scalability for larger holdings. However, they introduce chain-of-custody and authenticity concerns, remain dealer-dependent for liquidity, still carry collectibles tax treatment, and offer poor divisibility. Bars make sense for investors wanting meaningful physical exposure through professional vault storage, but they don’t solve the fundamental inefficiencies of owning physical metal.

Gold ETFs deliver simplicity, high liquidity, and low expense ratios compared to physical metal, with no storage hassle. However, ongoing fee drag erodes returns over time, many are still taxed as collectibles, and there’s no embedded leverage. For most investors seeking straightforward gold exposure, ETFs make sense as a core position.

Gold miners offer equity upside, theoretical leverage to gold prices, and possible dividends. The trade-off is substantial: company-specific risk, cost inflation, jurisdiction exposure, and high volatility. Miners have historically underperformed gold itself over many cycles despite their supposed leverage. They work as a tactical equity sleeve but are not a pure gold proxy.

Gold futures provide capital efficiency, deep liquidity, central clearing, and favorable 60/40 tax treatment for U.S. investors. The requirements are higher: leverage amplifies risk, margin management and roll mechanics demand attention, and the approach is more institutional in nature. For sophisticated hedging or directional views with capital efficiency, futures are often the optimal choice.

Return stacked ETFs like BTGD and RSSX offer a way to add gold exposure without sacrificing allocation to equities or bonds, using derivatives-based leverage to provide additive rather than substitutive exposure. They’re compelling for investors who want gold’s diversification benefits without the opportunity cost of reducing other holdings. The trade-offs include embedded financing costs, complexity, and amplified drawdowns when correlations spike. They represent institutional-style thinking packaged for broader access.

The common theme across these options is clear. Coins are romantic but expensive and inefficient. Bars are a step up but still carry physical-ownership baggage. ETFs are practical and simple but carry fee and tax nuances. Miners are equity bets with gold flavor, not pure hedges. Futures offer clean, scalable, institutional access—if you can handle the tools. Return stacked products provide a way to have your cake and eat it too—with the understanding that leverage always has a cost.

One Last Angle: Did You Know You Can Fund a Futures Account With a Gold Warehouse Receipt?

Here’s a twist that almost never shows up in retail “how to buy gold” guides—and something we noted in our SMA platform piece.

In some cases, you can fund or collateralize a futures account using a gold warehouse receipt, essentially making your gold work as margin collateral rather than sitting idle.

In the centrally cleared futures system, approved warehouses and depositories issue warehouse receipts representing ownership of specific standardized bars that meet exchange specifications. These receipts can be deliverable against certain futures contracts and, subject to exchange and clearing rules, can sometimes be used as collateral to meet margin requirements rather than posting pure cash (see CME Group documentation on acceptable collateral and COMEX delivery and warehouse receipt procedures).

In other words, for sophisticated investors, gold doesn’t have to sit dormant in a vault or in your safe. Properly structured, it can serve as collateral in a futures account, supporting trading and hedging activities while still representing a claim on physical metal.

It’s a far cry from overpaying for coins at a strip-mall dealer, and a good illustration of how institutional gold markets actually operate. If you’re serious about your gold allocation, it’s worth thinking beyond “buy coins vs. buy GLD” and considering how the structure you choose affects cost, tax treatment, flexibility, and what else that gold can do inside your broader portfolio.

Gold Access Points at a Glance

|

Vehicle

|

Upfront Cost

|

Ongoing Cost

|

U.S. Tax Treatment

|

Pros

|

Cons

|

|

Physical Coins

|

3–8%+ premium over spot; wider in crisis periods

|

Storage 0.1–0.5%/yr if vaulted; insurance; security costs if self-stored

|

Collectibles (28% max LT rate)

|

Tangible ownership outside financial system; highly portable; no counterparty risk; recognized worldwide

|

Wide dealer spreads; poor liquidity at scale; storage/insurance burden; unfavorable tax treatment; no yield |

|

Physical Bars

|

1–3% premium over spot for recognized refiners

|

Storage 0.1–0.5%/yr if vaulted; insurance; potential re-assay costs

|

Collectibles (28% max LT rate)

|

Lower premiums than coins; better scalability; standardized and internationally recognized

|

Chain-of-custody concerns; dealer-dependent liquidity; poor divisibility; storage still required; unfavorable tax treatment

|

|

Gold ETFs (GLD, IAU, SGOL)

|

Bid-ask spread (typically pennies); no premium to NAV in normal conditions

|

Expense ratio 0.17–0.40%/yr

|

Typically collectibles (28% max LT rate); check prospectus

|

Highly liquid; easy to trade; low ongoing cost; no storage hassle; accessible in any brokerage

|

Fee drag compounds over time; often taxed as collectibles; no leverage; no physical possession

|

|

Gold Miners (GDX, GDXJ, individual stocks)

|

Brokerage commission; bid-ask spread

|

Fund expense ratio 0.51–0.52%/yr for GDX/GDXJ; individual stocks have no expense ratio

|

Standard equity treatment (20% max LT rate; qualified dividends)

|

Potential leverage to gold price; dividends possible; favorable tax treatment vs. collectibles

|

High volatility; company-specific risks; historically underperform gold; not a pure gold proxy

|

|

Gold Futures (COMEX GC)

|

Bid-ask spread (tight, typically $0.10–0.20/oz); commission ~$2–5/contract round-trip

|

Roll costs vary (contango/backwardation); margin opportunity cost |

Section 1256: 60% LT / 40% ST (~23% blended max rate)

|

Capital efficient; deep institutional liquidity; favorable tax treatment; clean price exposure; central clearing

|

Leverage amplifies losses; operational complexity; requires futures account and FCM; not suitable for all investors

|

|

Return Stacked ETFs (BTGD, RSSX)

|

Bid-ask spread (typically pennies)

|

Expense ratio 0.50–1.00%/yr; embedded financing costs |

Varies by fund structure; may include 60/40 treatment on futures components

|

Additive exposure (gold + stocks or bonds); no need to sell existing holdings; capital efficient

|

Embedded borrowing costs; complexity; leverage amplifies drawdowns; correlation risk in stress periods

|

References

World Gold Council, Gold Demand Trends 2023 (Central Bank Gold Demand).

World Gold Council, Gold ETF Flows (various quarterly and annual reports).

Claude B. Erb & Campbell R. Harvey, “The Golden Dilemma,” Financial Analysts Journal, 2013.

Paul M. Nathan, “Bullion Coin Premiums in Crisis Markets,” Journal of Financial Planning, 2010.

Internal Revenue Service, Publication 544: Sales and Other Dispositions of Assets (collectibles, including precious metals).

Internal Revenue Service, Publication 550: Investment Income and Expenses (Section 1256 contracts and 60/40 rule).

SPDR Gold Shares (GLD), iShares Gold Trust (IAU), and Physical Gold Shares (SGOL) prospectuses and fact sheets (expense ratios, structure).

VanEck Gold Miners ETF (GDX), VanEck Junior Gold Miners ETF (GDXJ) prospectuses and fact sheets.

CME Group, COMEX Gold Futures (GC) Contract Specifications and collateral/warehouse receipt documentation.

London Bullion Market Association (LBMA), Good Delivery Rules and accredited refiner lists.

Frank J. Fabozzi, Roland Fuss, and Dieter G. Kaiser (eds.), The Handbook of Commodity Investing, Wiley Finance, 2008 (chapters on gold bullion vs. gold equities).

Return Stacked ETFs (BTGD, RSSX) prospectuses and fund documentation.