Managed Futures could sure use a good outlier move from somewhere. They are roughly even YTD according the Newedge CTA index, and just about everyone is holding out for a hero til the end of night (in this case the year). In more scientific language, managed futures has been waiting for a catalyst to jump start performance. So who is this knight in shining armor? It just might be the bond market, spurred on by 10 Year Treasuries.

Business Insider rolled out a new article, alerting the potential of an “ugly” Treasury bond market with the headline, “The Treasury Bond Market Could Get Ugly Between Now And September 19.” Basically, summer’s coming to an end, and traders are coming back into market that looks ripe for change.

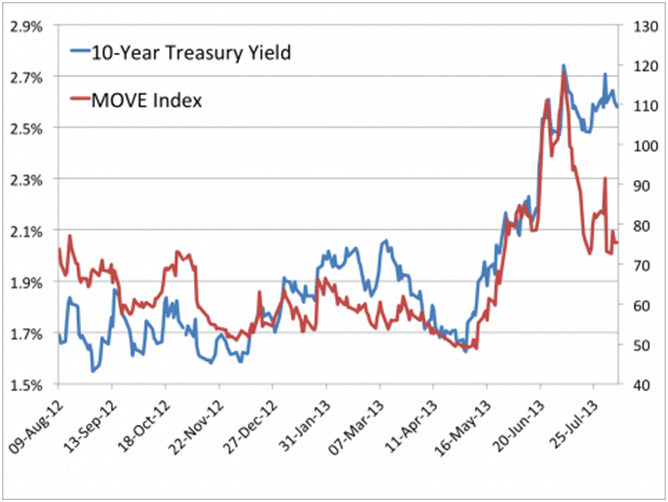

To flesh out their theory, they look at their version of 10 Year Treasury volatility called the “Move Index” (Merrill Option Volatility Estimate), and a drop off in trading.

Chart Courtesy: Business Insider

Chart Courtesy: Business Insider

(Disclaimer: Past performance is not necessarily indicative of future results.)

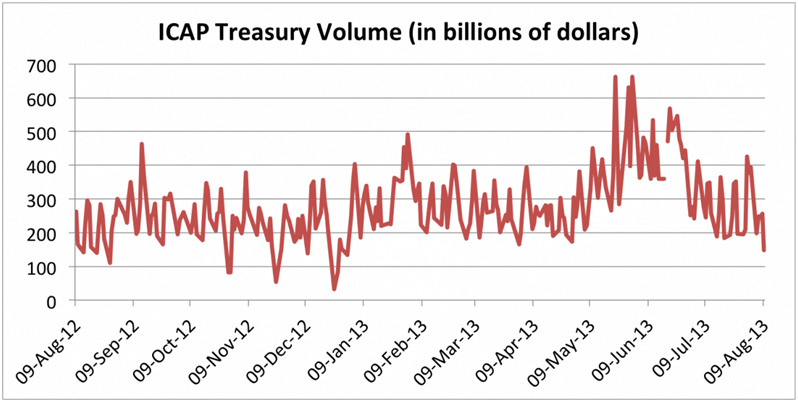

Now notice the decline in trading the past couple of weeks.

Chart Courtesy: Business Insider

Chart Courtesy: Business Insider

(Disclaimer: Past performance is not necessarily indicative of future results.)

So what is all this the recipe for? BofA Merrill Lynch says a rise in risk.

“A seasonal analysis of our MOVE Index (aka the Merrill Option Volatility Estimate) says that fixed income implied volatility tends to jump sharply during August. With the recent range in U.S. Treasury yields growing mature and poised to complete (we continue to target 2.85%/2.95% in US10s), the potential for fixed income implied volatility to hold to its seasonal norms is too high to be ignored…..Expect one more [Fixed Income] volatility bump [in August] before a seasonal lull.”

We’ve talked before about how managed futures love the bond market, and while there are those that don’t believe a sell off in bonds would benefit managed futures the same as the 40 years of run ups have, a trend is a trend – be it up or down – and managed futures could sure use a sustained trend right about now.