Our own Jeff Malec went solo on the Derivative last week, dishing on all sorts of topics from ski races to conferences. But one topic caught our eye in particular, talking bonds.

And particularly bonds in times of war. Last month, when the U.S. began military strikes on Iran, markets delivered a reminder that the old playbooks do not always apply.

Equities sold off. Oil surged higher. And U.S. Treasuries, historically one of the market’s go-to safe havens during geopolitical stress, declined as yields moved sharply upward.

In a moment where many expected a classic “risk-off” response, bonds instead participated in the volatility. The 10-year Treasury yield moved from roughly 4.0% toward 4.3%, after already pressing near 4.5% earlier in the year before retracing. The prevailing interpretation was straightforward: higher oil prices could revive inflation pressures, prompting markets to quickly reprice future interest rates.

That may be logical on paper. In real time, however, watching bonds sell off while missiles were in the air for an Iran war many had thought would be a prelude to World War III…. was a striking departure from conventional expectations.

A Historically Difficult Period for Bonds

But this episode was not an outlier. It was simply the latest chapter in what has become one of the most challenging stretches for fixed income investors in decades.

Across a few bond ETF proxies, the damage is easy to spot:

For investors accustomed to bonds serving as ballast, this has been a painful adjustment.

Why This Matters for Managed Futures

But this isn’t just a story of bonds haven’t been going up (rates down). Here in our Alternative Investment world heavy in trend following, global macro, and managed futures, it’s more that they haven’t been going anywhere.

Bonds have historically been one of the most important return drivers for managed futures and trend-following strategies. Review many of the strongest CTA periods, from the late 1980s through the 2000s and into the Global Financial Crisis, and te trading of fixed income futures (in rates and bonds) frequently played a leading role.

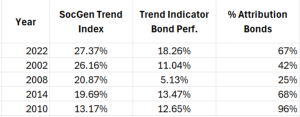

Here’s the best 5 years in the SocGen Trend Index over the last 24 years, and you can see that bonds played a big part, contributing between 25% and 96% of the total performance. (note, this is using the Trend Indicator’s bond performance vs the Trend Index performance, so not exactly correct, but close enough for these purposes).

Importantly, this is not limited to U.S. Treasuries. Managed futures programs typically trade a broad universe of fixed income markets across the globe, from Australia to Canada, Germany to Japan.

These markets are deep, liquid, and often trend together during major macro shifts. When bonds trend cleanly, they can provide meaningful opportunities across multiple regions simultaneously.

The issue recently has not been a lack of movement. It has been the lack of sustained movement.

Instead of durable trends, bond markets have been characterized by reversals, false starts, and range-bound trading for much of the last five years.

The Numbers Behind the Frustration

2022 actually demonstrated how powerful bond trends can still be.

As inflation surged and yields rose rapidly, trend-following managers were able to position short bonds and capture one of the more profitable CTA environments in recent memory. As seen above, the SocGen CTA Index posted one of its strongest annual returns during that period.

Since then, however, the environment has changed dramatically.

Markets have struggled to determine whether rates should continue materially higher or gradually drift lower. That indecision has created repeated whipsaws for systematic trend strategies.

Using SocGen trend indicator data, again, the results are striking:

That is not simply below average. It is historically extreme.

For investors frustrated with recent managed futures performance, bond market behavior is likely the primary explanation. Gains from trends in commodities (OIL… anyone), currencies, and select other sectors have often been offset, or fully erased, by losses within fixed income positioning.

Roy Niederhoffer’s Warning Looks Prescient

A few years ago on The Derivative, Roy Niederhoffer discussed an important structural issue that now feels highly relevant.

His argument was that the 30-year bull market in bonds created a powerful tailwind for many systematic strategies. Falling yields and rising bond prices offered persistent, clean trends.

But simply reversing that chart, assuming rising rates and falling bond prices would be equally profitable, was never guaranteed.

Why?

Because shorting bonds introduces different economics:

- Roll costs can become a headwind

- Carry dynamics change

- Downtrends may be less persistent

- Choppier price action can disrupt systematic signals

In other words, correctly forecasting higher rates does not automatically translate into profitable trend-following returns.

That distinction matters. A manager can be directionally right and still struggle if the path is noisy enough.

That has largely defined the post-2022 bond market.

So Where Does That Leave Investors?

We do not believe this environment lasts forever.

Bond markets will eventually establish a new equilibrium. And when they do, trend-following strategies should be well positioned to respond, whether the next durable move is higher yields, lower yields, or a globally divergent rate regime.

Fixed income remains a core sector in managed futures portfolios for a reason: these markets historically do trend, and when they do, the opportunity set can be substantial.

But the current drought is real.

It has been historically severe, unusually persistent, and likely the single largest drag on CTA returns in recent years.

Final Thought

No strategy works in a straight line, and managed futures is no exception.

Understanding why recent performance has been muted is often the first step toward maintaining conviction through difficult periods. In this case, the explanation may be simpler than many realize:

It has largely been the bond market.