Today is the first day of October and that means it’s time to break out the Halloween decorations, drink as many pumpkin latte’s as possible, and watch as much Sunday football as possible. But in the Ag world, it’s more about the fresh harvest smell of Soybeans and Corn. The latest USDA crop report inked its way out, amid the government shutdown yesterday, with new supply numbers… So how are the crops fairing this time around compared to last year’s drought?

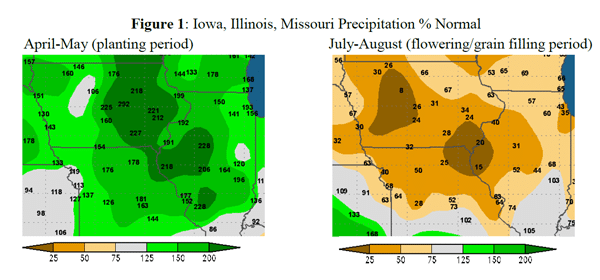

Earlier in the summer, we covered M6 Capital’s behind the scenes paper on the Ag markets, with record breaking rain for the late spring/early summer months, providing bold predictions for grain yields. But it doesn’t take someone specializing in the Ag markets to know that the Midwest has been in a dry spell since then…

Maps Courtesy: M6 Capital

Maps Courtesy: M6 Capital

But what these green and orange maps don’t tell you are what it means for the Ag crops themselves and how it could affect the contracts pricing, in which M6 are experts. They’re saying it’s going to affect soybeans far more than the yellow veggie.

“ As a result {of the lack of rain}, the US soybean yield is expected to 8-10 % below trend. This largely reduced soybean crop will likely keep US supplies tight well into 2014, while keeping oilseed prices firm. Global soybean demand is currently very strong. Soybean crush margins in China, the world’s largest soybean importer, are at the highest levels in three years. Therefore, Chinese import demand is currently very good.”

But if the US supplies will be tight – why are Soybeans down -16.55% since the end of June and near a 19 month low (past performance is not necessarily indicative of future results). Well, there’s yesterday’s USDA crop report which stated domestic soybean inventories totaled 141 million bushels (15 million bushels more than last year). That’s one for M6 to work out on their own…

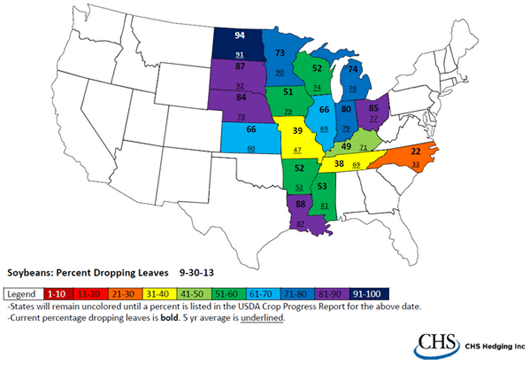

Before we get off Soybeans, we can’t help but share this map from the CHS Hedging using USDA crop report data showing the percent of Soybean plants dropping leaves. I guess there is more to this than just whether it’s raining in Chicago.

Map Courtesy: Joe Hofmeyer

How about corn? M6 is predicting that both the corn and wheat supply will be in great shape (824 million bushels domestic via USDA crop report), not to mention foreign support from Brazil and the Black Sea area. And in this case – the markets have reacted as you would expect from large supplies – with Corn having dropped -13.69%, near its lowest closing price in three years. (past performance is not necessarily indicative of future results).

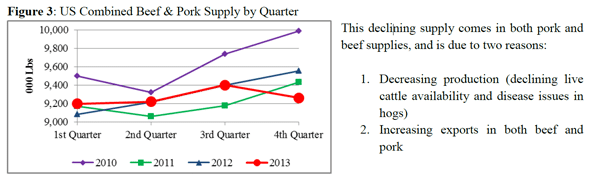

But it’s not just grains in the Ag market, quite a few people forget about live cattle, and M6 is expecting a significant change in cattle supply from just last year.

“As shown in Figure 3 below, combined US beef and pork domestic supplies in the 4th quarter of 2013 should decline to the lowest level in years, down over 3% from last year. A 3% change year over year is historically a VERY large change.”

Chart Courtesy: M6 Capital

Maybe the decrease in Cattle production has something to do with large meat processors now refusing cattle with growth hormones (we covered here), or maybe not as many Cattle were raised this year. Whatever the cause, we’re all for movement in some form, and M6 suggests exactly that.

“There is no lack of opportunity in agricultural markets in coming months. M6 Capital’s analysis, and we do a lot of it, continues to point to these opportunities being in both bull and bear markets.”

For a more in depth look at the program read our Managed Futures Spotlight on M6 we published in February.

(If you would like a copy of the entire M6 newsletter, please email us at [email protected] and we would be happy it forward it to you).