It seems like nary a day goes by without a new article popping up hating on diversification. Not because there’s anything really wrong with diversification, but because financial journalism seems to think there’s something wrong with diversification, especially with the S&P at all time highs just a couple weeks ago. Take the recent Market Watch article entitled, “Why Diversification isn’t working.”

Much like the majority of articles out there, the headline is a little deceiving. Author Howard Gold isn’t claiming that the idea of the theory of diversification is flawed, but the application of diversifying your portfolio to include other asset classes in this current climate is flawed, as in his words, “investors have to choose between many bad choices,” implying that there’s nothing out there that can really create a portfolio full of truly diversified asset classes. He even goes as far as calling some of the choices rotten eggs.

“But what if all the baskets were floating in the same direction and the only one that wasn’t was filled with rotten eggs?”

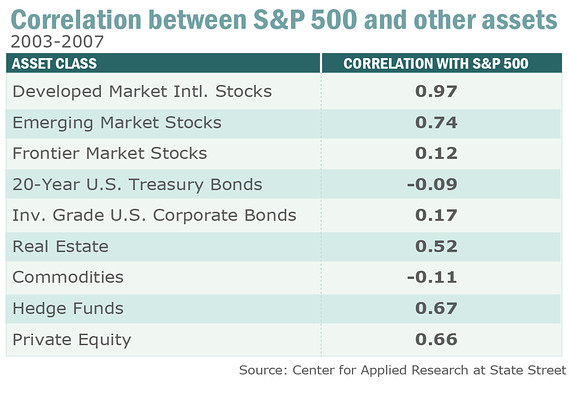

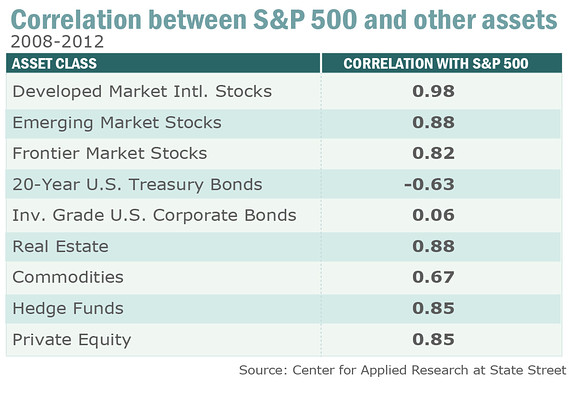

To show that all the basket are floating in the same direction, he shows two tables outlining nine asset classes and their correlation to the S&P 500, one between 2003-2007, and the other from 2008-2012.

Charts Courtesy: Market Watch

Charts Courtesy: Market Watch

(Disclaimer: Past performance is not necessarily indicative of future results)

As a refresher: the closer the correlation to 1.00, the higher the correlation, the closer to -1.00, the more negative correlation the two asset classes are, and in-between -0.30 and 0.30 is an example of a non-correlation. His argument, is that among the nine asset classes… the positive correlation to each other are growing – except for in the 20-Year US Treasury Bonds, which he argues are the rotten eggs (because we’re at the end of a 30 year bull market in bonds and prices are likely to fall).

“So, the choice appears to be throwing even more money into stocks, which are nearly five years into a bull market, or buying bonds, which we know will go down in price. Or keeping more in cash (with its negative real return) or stuffing money in the mattress. Or, God forbid, buying leveraged inverse ETFs as a “hedge.”

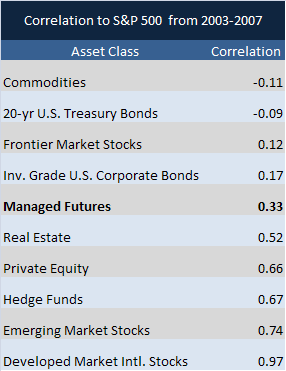

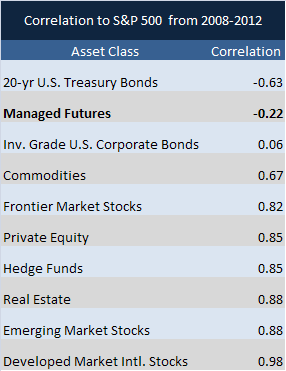

Now we in the managed futures space love talking non-correlation, and we really like that something like this is getting good attention… but the article is missing a rather big thing in our opinion… Managed Futures. So what does the shift in correlations look like when including managed futures. To do this we used the BarclayHedge BTOP 50 Index.

(Disclaimer: Past performance is not necessarily indicative of future results).

Turns out managed futures has become less correlated to stocks, unlike the other asset classes (or more appropriately – more negatively correlated). Now, that’s rather obvious from looking at the performance, where managed futures was up while stocks were down in 2008, and has been flat to down since 09 while stocks have been going straight up. (Disclaimer: Past performance is not necessarily indicative of future results).

But we don’t really agree that things are becoming more correlated as of late. Yes, they became very correlated in 2007, 2008, and 2009 – throwing off managed futures and their multi-sector diversification in the process – but since then things have been moving away from that risk on/risk off environment. As a whole, we’ve been tracking how correlated the futures markets have been to one another, not just other asset classes (i.e. gold futures, corn futures, S&P futures, and so on) (see here, and here), and compared to the 2008-2009 numbers, the correlation has significantly decreased.

So managed futures has remained non correlated, but is that ‘basket’ full of rotten eggs just like bonds? Not on your life. Indeed, managed futures has had nearly the inverse performance of bonds since 2009, and is at all time lows versus all time highs. The new attitude is to buy into managed futures not just because it will help your portfolio when the s^&% hits the fan, but because it isn’t likely to get much worse from here (although it could).

hbspt.cta.load(313774, ’99e6b49e-c85e-4c18-a846-604de1b9ae53′);