Sometimes the headlines just write themselves… We might have been writing about hogs today given their sharp move higher and multiple “limit up” days in a row; but when we found out the move was from a deadly diarrhea swine virus… well, that’s just too good to pass up.

One might think the public would have heard about something as unique as this, but Kelsey Gee at the Wall Street Journal details that the virus started almost a year ago, and uncovers the scope of the situation.

“Porcine epidemic diarrhea virus has spread to farms in 25 states and killed millions of young pigs since it was identified in the U.S. for the first time last April, and the number of confirmed new cases each month has accelerated since late last year, according to industry estimates.

Last month, the U.S. Department of Agriculture trimmed its forecast for total U.S. pork production this year by 160 million pounds to 23.4 billion, citing the continued spread of the virus. Its forecast marked a 1% increase over 2013 output, down from a 2% increase projected in January. The government is scheduled to update its forecast on Monday.”

Well, it’s nice to hear this isn’t spreading to humans (a la Mad Cow or Bird Flu), but did he just say millions of hogs? We happen to have someone in the office whose grandparents used to be pig farmers (among others) and know that it usually takes six months for young hogs to grow up. Theoretically, that means we should have started experiencing a shift in lean hogs in September, but we’re only now seeing a spike due to the lack of supply.

(Disclaimer: Past performance is not necessarily indicative of future results.)

(Disclaimer: Past performance is not necessarily indicative of future results.)

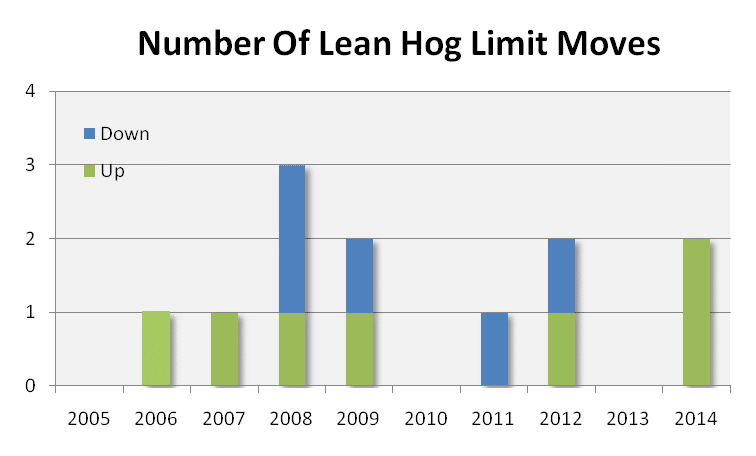

Chart Courtesy: Finviz.com

(If wondering why the chart is all jacked up, see here and here.)

Hogs have been up 15 out of the past 20 days, with a run of six straight up days in there and two “up limit” moves based on this diarrhea virus, catching more than a few traders on the wrong side of the Hog market:

“I’ve been around this market 28 years, and this is the most extreme situation of wild panic that I’ve ever seen,” said Dennis Smith, a commodities broker at Archer Financial Services in Chicago. Traders who had bet on lower prices “were just run over,” he said.”

These ‘limit up’ moves can be worrisome for Managed Futures managers and systematic programs who risk only a small percentage of total equity on any one trade (typically at or below 1.0% of equity), because the market won’t let them out during such moves, meaning their willingness to risk $10,000 on $1 million could mean a loss of $15,000 or $25,000 by the time they are able to get out of the position.

Just what is ‘up limit’ or as it’s also called – ‘Limit Up’? Well, besides being on our Best (futures) investing movies ever list, Limit Up is a unique futures phenomenon where the exchange halts trading if a market moves too far up (or down… Limit Down) and there are no offers at that price. In layman’s terms – when there are no more market participants willing to sell at a price 3% above yesterday’s close, the market shuts down until tomorrow, or until someone comes in and is willing to sell at or below that price. This is similar to the circuit breakers employed on the NYSE, and is intended to give people time to catch their breath, reassess the situation, and allow for better price discovery.

The CME sets the lean hog price limit move at 0.03¢ above or below the previous day’s settlement price, which might not seem like a lot, until you consider it represents about a 3% move. Both Live Cattle and Feeder Cattle have the same 0.03¢ limit.

So what if a CTA was caught in on a short position, would there be a hell to pay? Let’s consider a $1 Million account risking 1% per trade and using the 6 day Avg True Range of $1,398 as a risk amount – they would be doing 7 contracts (1%*$1mm = $10k/$1,398). Now, the two limit moves in Hogs saw prices go up (there may have been some offers in there, we’re assuming there were none for this example) from an opening of 103.85 to 112.575 three days later. At $400 per full point, on 7 contracts, our theoretical CTA would be looking at losses of about $25,000, or 2.5%. And if we assume they were almost out of their position the day the market’s locked limit and this entire extra loss was on top of their desired 1% loss, that’s a 3.5% loss – not the end of the world, but about three times as much as they wanted to lose on the trade.

How common are these limit moves? Not very, although Lean Hogs has already experienced more “up limit” move days in the past two months than in the past three years… and it’s only one limit move away from tying the number of moves in 2008. The question is… will we see more to come if the virus isn’t controlled?

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

P.S. – Both Feeder and Live Cattle are still hovering around their all time highs

And don’t forget our Bacon post: “What does Chinese deal mean for Hog Prices?”