If you haven’t heard, we’re in the midst of the strongest El Nino in history, and while it might be a chilly 33 degrees in Chicago, the planet just recorded its warmest land and sea temperatures ever:

JUST IN: January 2016’s globally averaged temperature over land & sea was the warmest ever on record since record keeping began in 1880.

— CNBC Now (@CNBCnow) February 17, 2016

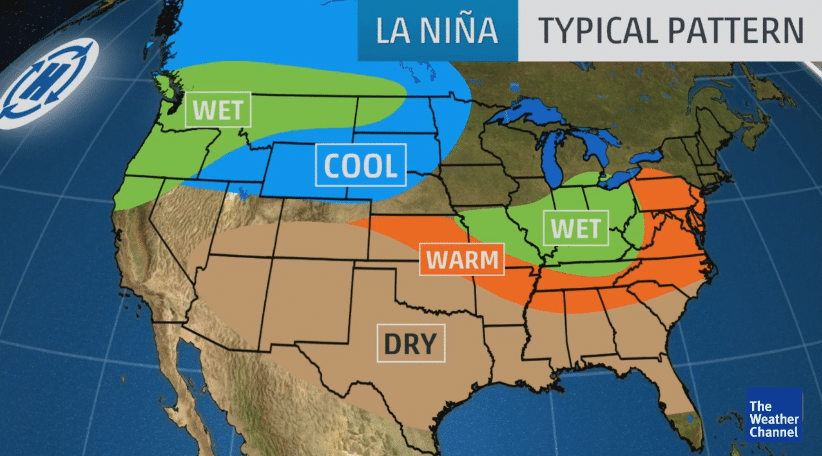

A while back, we covered El Nino and what it could mean for commodities, but we may need to start concerning ourselves with another weather phenomena that typically follows El Nino, called La Nina (supposedly the Spanish flavor is due to fisherman naming the phenonemons off predominantly Spanish speaking South America). So what is La Nina? Essentially, it’s the exact opposite of El Nino, where the Pacific Ocean near the equator experiences cooler than usual temperatures, causing this effect on the United States weather pattern, via the weather channel.

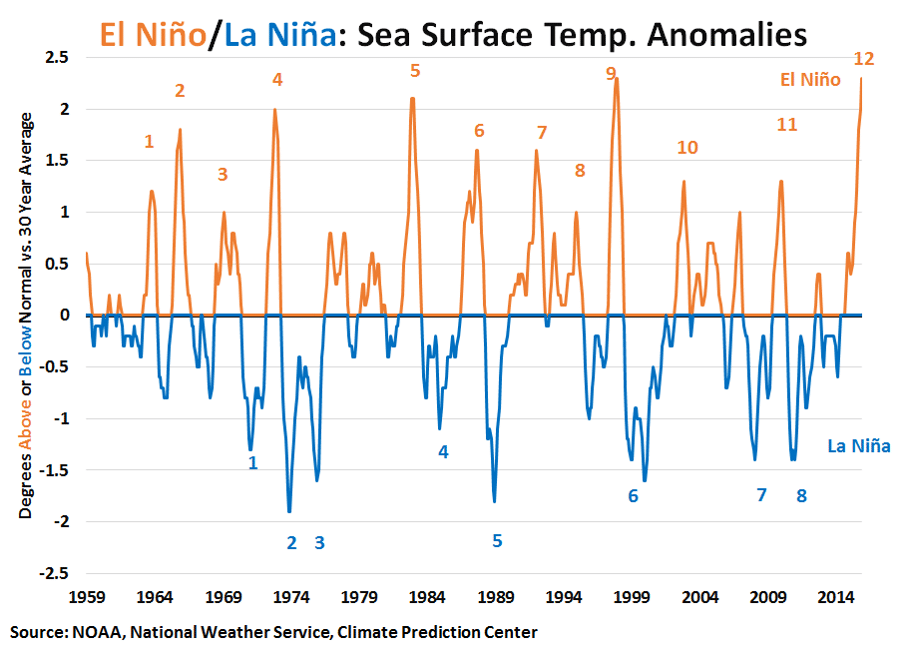

But it’s not just that this weather phenomena follows El Nino, it’s that the more extreme the El Nino, the more extreme possible response from La Nina, via a chart by Erik Norland, Senior Economist of CME Group.

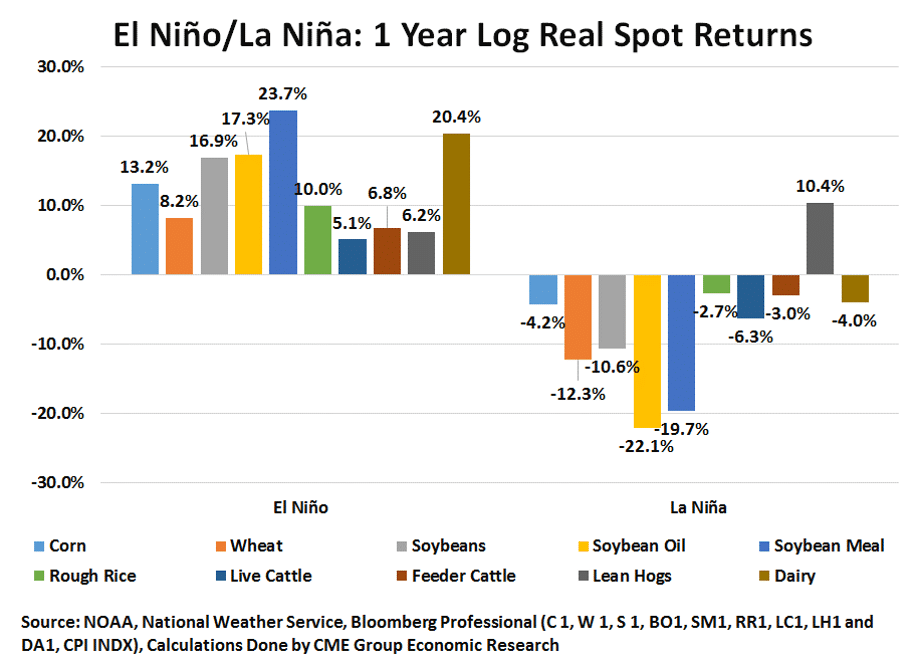

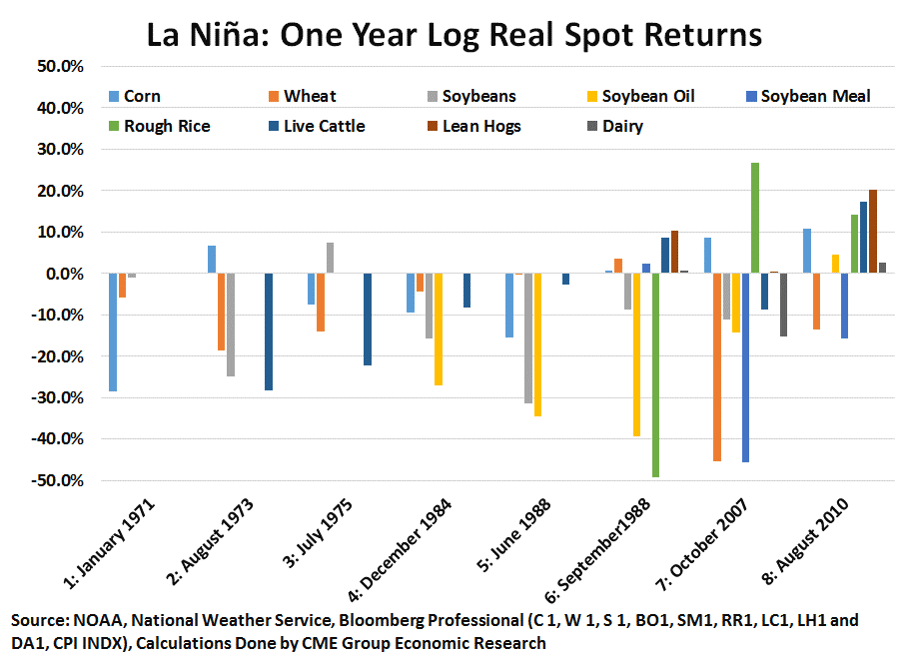

So who cares besides Jim Cantore and weather geeks? Well, anyone who grows a crop in the US, or trades those crops (affectionately called AG markets, after agriculture) in the futures markets, for starters. Using data from the NOAA, the CME Group looked at spot and rolled (reinvested) AG futures market returns in the 12 and 24 months after temperatures rose by one degree above normal (El Nino) or fell by one percent (La Nina) from 1959 to present. Turns out… the shifting weather seem to play a role with AG prices rising during El Nino and falling during La Nina.

El Nino Effect

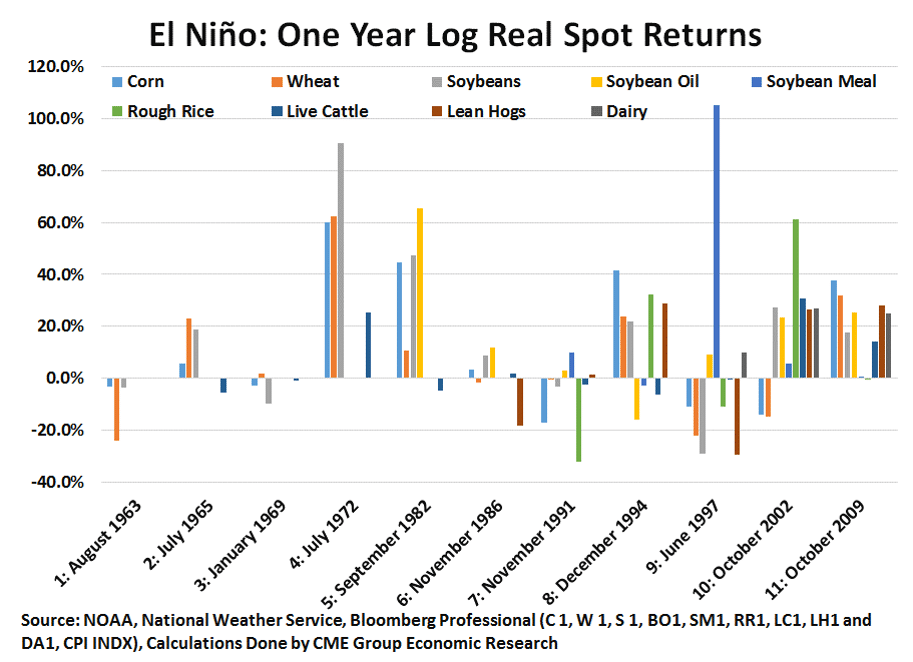

Scanning the data above, we would expect Ag prices to be higher during this record El Nino… but we’re only a couple months into El Nino, and it’s hard to say if the grain and meat markets are going to have the same response as it has on average over the past 60 years. We are the first people that will tell you that past performance is not necessarily indicative of future results, and so far grains and meats are unexpectedly down since El Nino has started. But this wouldn’t be the first time that El Nino didn’t have an effect on commodity prices. Take a look at each market move during each El Nino dating back to 1963 and you can see more than a few down bars. But given that this is the strongest El Nino on record, the lack of corresponding moves in the Ag markets are a bit puzzling, with sympathy sell offs in energy markets perhaps the culprit.

In the meantime… What about La Nina?

With La Nina the opposite phenomenon of El Nino, we would expect the opposite market behavior – and that is exactly what is seen when looking across the same swath of markets, with everything mostly down across the La Nina’s, and just a few bars higher. It is interesting to note that the recent La Nina’s have seen more market moves up than in the past, however.

Takeaway:

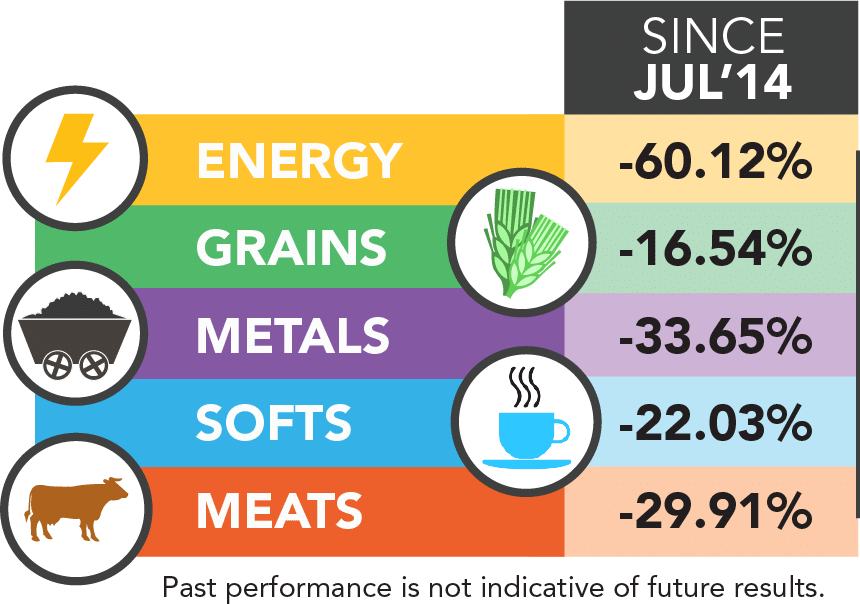

Commodities have consistently been moving downward over the past 18 months, but it’s actually interesting to note that grains have seen the smallest decline when compared to the rest of the sectors. Perhaps that is the El Nino effect offsetting the commodity sector sell off somewhat?

(Performance as of 1/29/16)

Energy = WTI, Brent, Heating Oil, Gas RBOB Gas, Natural Gas, and Ethanol

Energy = WTI, Brent, Heating Oil, Gas RBOB Gas, Natural Gas, and Ethanol

Grains = Wheat, Corn, Soybeans, Soybean Oil, Canola Oil

Metals = Gold, Silver, Copper, Platinium, Palladium

Softs = Cotton, Orange Juice, Coffee, Sugar, Cocoa, Lumber

Meats Live Cattle, Feeder Cattle, and Live Hogs

And now what? If prices are supposed to go up in El Nino years but they’ve gone down… if they’re supposed to go down in La Nina years, will they now go up? Will Bizzaro world continue to hold steady? Or will La Nina assert itself on the downside with grain markets ‘catching up’ to energies and the rest with substantial sell offs. Only time will tell, so we’ll leave it to the professional Agriculture traders to find the highs, lows, and possible return drivers in these markets. You can request a list of Agriculture traders we consistently track here.