Managed Futures is officially in the red for the first time in 2016, seeing a -8.83% drawdown since mid-February. We could sit here and tell Managed Futures investors to blast Wilson Phillips “Hold On,” on full volume (we already did that), but it only provides temporary relief. What you may need more than a song, is some hard numbers. Or, as Anton Ego put it: “some fresh, clear, well-seasoned perspective”

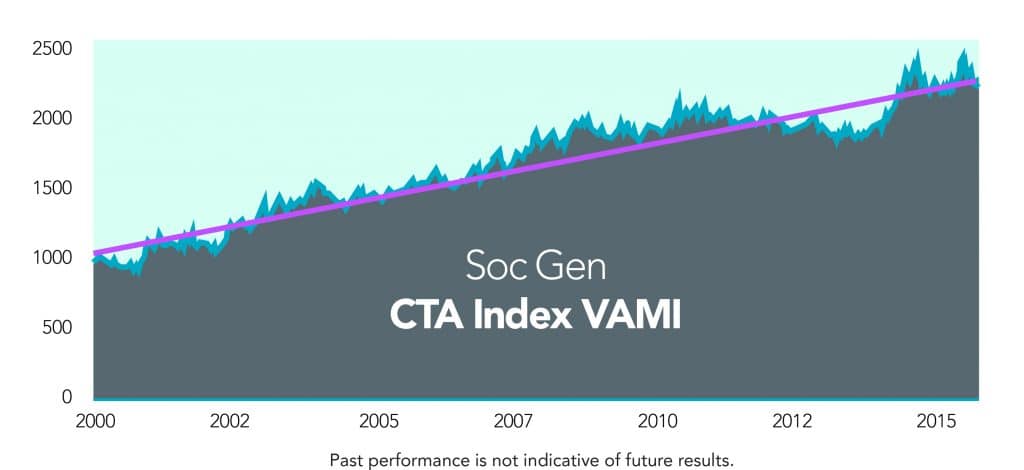

You see, drawdowns are messy. They feel impossible, and that they will never end. They feel like it’s the first time such an investment has gone through such a losing stretch. But with a little perspective, we can see that this drawdown, is pretty darn normal for the managed futures asset class. Of course, past performance is not necessarily indicative of future performance. That being said, it doesn’t hurt to weigh the current drawdown against the long-term performance of managed futures, as shown by the SG CTA Index below. Yes, we’re in a drawdown. Yes, we’re back to around mid-2015 levels. But this is not an aberration on the chart. This is typical movement around the long term up trend line.

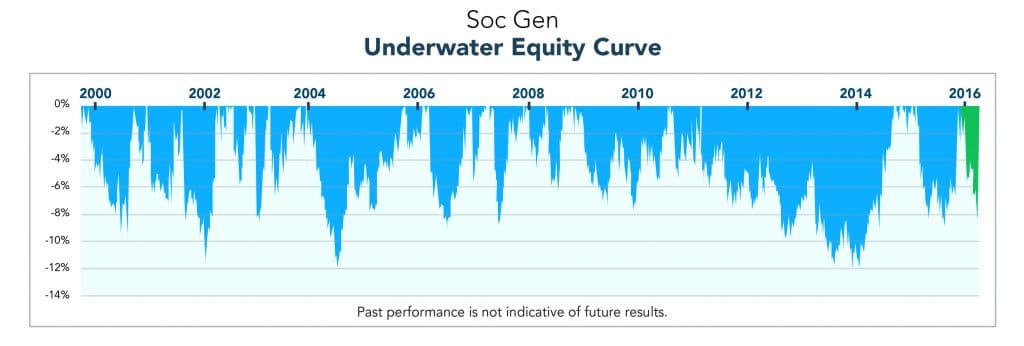

But it’s not all about looking at the nice upward sloping curve. Drawdowns are all about staring into the abyss – not knowing how far the bottom is. Luckily, we have 23 other major drawdowns in the SG CTA Index since its inception in 2000 that we can analyze to get a better feel for where possible bottoms might be. A quick change to the chart above, flipping it on its head to show only the drawdowns in an iceberg-like underwater equity curve shows just what each drawdown period looked like in terms of magnitude and duration. The further down and wider the ‘iceberg’, the worse the drawdown. The current drawdown is way over there on the right, neither very deep or wide.

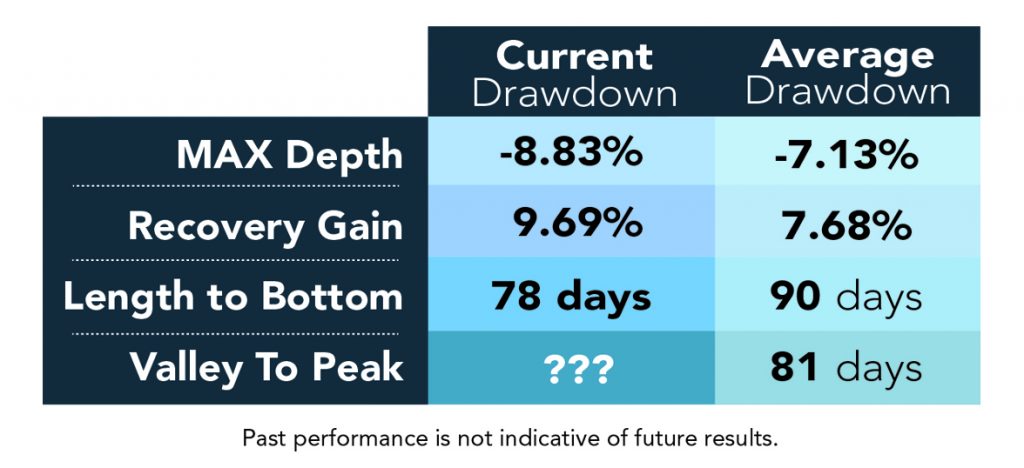

So what can we glean from a look at these past drawdowns? One, that the current drawdown is already deeper than the average drawdown of -7.13% and the median drawdown of -7.21%. In terms of duration, we are well into this drawdown, with the current drawdown now on day 78 (May 31st) without yet establishing a bottom. That compares to the average drawdown taking 90 (trading) days to hit its bottom. Now, whether this drawdown bottom is set earlier or later than the average is yet to be seen, but remember, once the bottom is found – there’s the recovery back to all-time highs. We know what the average recovery gain is – based on how much was lost, so the average recovery gain is +7.68%. In terms of duration, the average recovery takes 81 (trading) days. If the current drawdown acts like the average drawdown (which we can’t say it will), we could be looking at the beginning of August or Mid-August before we see Managed Futures reach new equity highs.

For the more visually inclined, here’s how the current drawdown compares to the averages over the past 17 years:

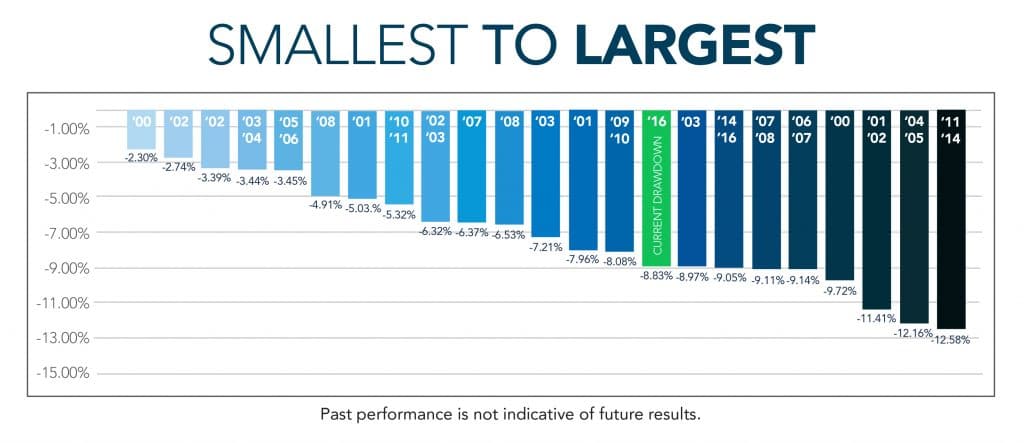

While stacking this drawdown up against all the others, you can see it square in the middle.

So where do we go from here? Nobody knows! This isn’t a stock where value investors will come in and support the falling price. It isn’t a currency a central bank will protect. It’s the average performance of dozens of managers trading models across hundreds of markets. Those markets need to compress and then see volatility expand (ideally separately from one another and based on different impetus) to turn the tide. We don’t know when that will happen, but we do know that it does happen. We can see exactly when it has happened based on the charts above, which is right about now… for this drawdown. Unlike a trade like Ackman’s Valenat trade – the ability of managed futures to pull out of this drawdown depends on dozens of markets moving into more favorable conditions. It depends on markets like Crude Oil and Hogs and Corn which have their own dynamics – with lower prices creating more demand, which leads to higher prices, which in turn leads to more production, which in turn leads to more supply, which leads to lower prices.

The instruments themselves are cyclical, so it only follows from where we sit – that the asset class which tracks that activity will be cyclical also – and perhaps even more cyclical than other investment types.

Here’s to this drawdown being more average than not. That 10% run back to new highs will be most welcome!