Is it just us, or is everyone talking politics these days amidst the US conventions and upcoming election. While data journalists will tell you that it’s all relative when debating whether the economy will be better under a Democrat or Republican, we’re starting to see more and more articles predicting what commodity/financials/currency markets will do in the wake of the 2016 election. The fervor has even gotten down to the rarely traded Mexican Peso:

To hedge against ‘Trump risk,’ bet against peso, Citigroup says https://t.co/DrTxp06N5v pic.twitter.com/AC6cmZQUMr

— Bloomberg Markets (@markets) July 25, 2016

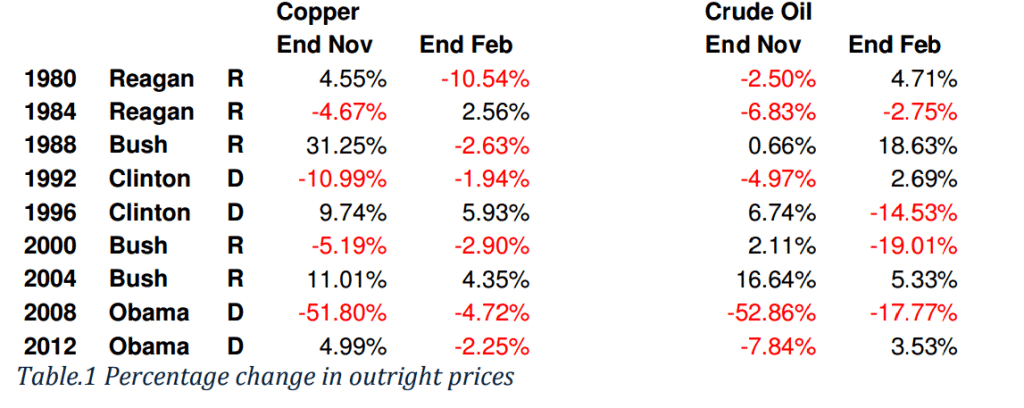

We already asked if Presidential elections are good for Managed Futures, but what about Crude Oil and the metal markets? When we’re looking for that kind of commentary, we turn to none other than oil and metals specialist – Jaguar Investments Limited. Here’s their take on price changes in Copper and Crude Oil from three months before the election to the end of the election cycle (the ‘End Nov’ column) and the change for the three months after the election (the ‘End Feb’ column).

Although it covers over thirty years, a sample size of nine elections is still ridiculously small – and it should come as no surprise that there is no clear pattern. The only [potential] pattern [seen] was that in the three months leading up to the election, the copper price alternates on election cycles. I also looked at the effect of different scenarios, i.e. Democrat victory, Republican victory, first-term President etc. and the only conclusion I could draw from that was that copper tends to fall in the three months after a new (not second-term) President. Since the sample size of occurrence is five occasions in the last thirty-six years I’m not sure I’d want to risk a dollar on that trade.

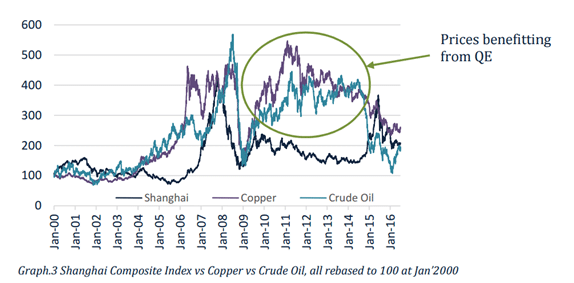

Turns out metals dance to the beat of their own drum, not one of either party. But Jaguar doesn’t stop there. You have to mention China if trading in commodities, especially Copper; and Jaguar’s research note looks at the correlations between Copper, Crude Oil, and the Chinese stock market.

The significant bull-market that peaked in early 2008 certainly coincided with bull markets in both copper and crude oil over the same period (indeed as Graph.3 above shows, copper and oil were leading indicators of stock market strength). But as Graph.3 also shows, neither copper or oil have shown any real affinity for the SCI since the crash in late 2008. Interestingly the one thing the graph does show clearly is how artificially high commodity prices were kept (dollar-denominated) as a result of the extraordinary quantitative easing by global central banks from 2008 to 2015. Once the markets began to price in the end of QE (at least in the US) then prices plummeted back to where they should have been all along [relative to the Shanghai].

Further and clearer evidence of these low (non?) correlations can be seen in Graph.4 below;

[Here are the correlations of the Chinese Renminbi to Copper and Crude]:

The disappointing issue with this indicator, however, is that although the correlations are high from January 2014, if we take the data back to July 2010 (when the second peg was abandoned), the correlation falls to just 25% and 14% respectively – i.e. not tradeable.

So they put out a research note showing no real zingers? You got it – and we think that’s their point – that sometimes the real news is to ignore the news. That sometimes the sky is falling metaphor is just that… a metaphor. As Jaguar puts it:

Neither Brexit, nor US Presidential elections, nor female leadership, nor the Chinese economy or Chinese stock market give us any clue as to where the prices of copper and oil may go next.

Although, if you press them for a prediction….

….over the last two years, there has been a relatively high correlation between the prices of these commodities and the Renminbi and so perhaps it would be prudent to keep an eye on that for future guidance. Although the PBOC is trying to manage currency volatility, there does not seem to be any meaningful attempt to stop the slide. Against a backdrop of expected economic weakness in the second half of 2016, the consensus seems to be that it will continue to slide through 6.70 and ultimately towards 6.90. This would imply copper and oil prices moving towards $7000+ and $80+ respectively. But I’ve been wrong before…

But in the end, while they consider all of the above – Jaguar isn’t in the business of making big directional bets on these markets. Their specialty is trying to capture short to medium term spread and arbitrage opportunities in metals and the energy complex. That means they are more interested in seeing what their contacts at physical dealers are looking at and planning than how the Chinese stock market is doing. Even so, it never hurts to know all sides of your particular slice of the market.

For more information on Jaguar Investments check out:

Alternative Analysis: Jaguar Investments Limited

25 Questions Every Investor Should Know About Jaguar Investments Limited