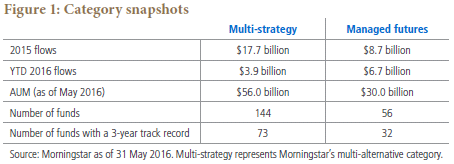

Alternative Investments are becoming more and more the place investors turn to find diversification for their portfolios. Look no further than a recent PIMCO piece showing Morningstar data from the start of 2015 to May 2016, where managed Futures and multi-strategy mutual funds saw roughly $37 Billion flow into the space.

Of course, these Morningstar categories are very broad, covering a lot of stuff we might not even put into the Alternatives bucket, but that’s for another post (in fact, that’s covered in this whitepaper – check it out: “Why Alternatives.”)

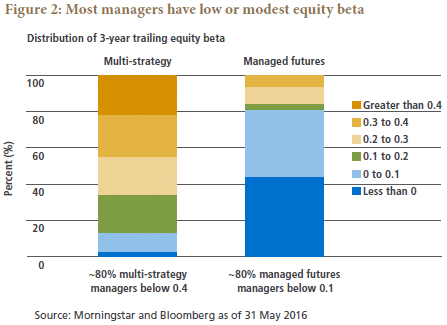

And understanding exactly what you’re getting in the Alternatives space is as important as ever. Take for example, this chart from PIMCO’s piece, showing the Managed Futures and Multi-Strategy categories broken down by their equity beta. If need a quick refresher, beta measures how much an investment moves when the stock market moves. A beta of 1.00 means they’ll have about the same volatility, while greater than 1 means more volatile, and less than 1 less volatility. Less than zero means you’ll have more or less volatility depending on the reading but in the opposite direction. Suffice to say a true diversifier should have a very low, if not negative, beta measurement – so that it isn’t moving in tandem with stocks.

While Pimco felt both categories are doing a good job of diversifying, with both having more than 80% of their funds with betas less than 0.4 – we were a little more interested in how 80% of managed futures has an equity beta of less than 0.1! And nearly half with negative betas. To us, this doesn’t show how both categories are good diversifiers, it shows how managed futures is a great diversifier.

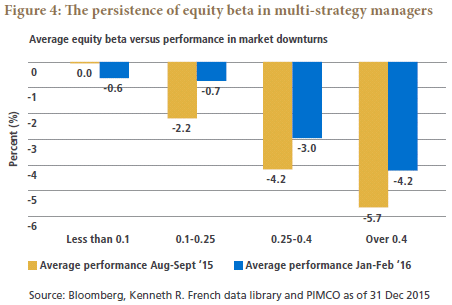

Finally, they finish with some analysis of each category during two recent sell off periods (Aug-Sep 2015 and Jan-Feb 2016). Our takeaway here, again, is that multi-strategy is more equity-like then many would probably assume, losing money right along stocks in both periods, no matter their equity beta.

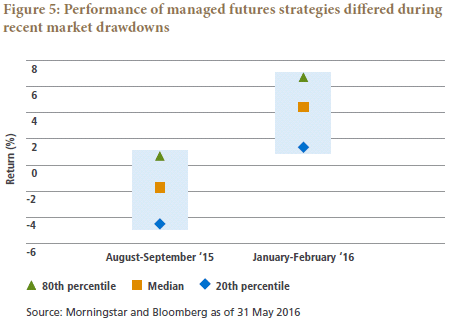

In contrast, Managed Futures mutual funds were up between 2% and 7% during the Jan-Feb stock market downturn across all of their beta ranges; while between up +1% and down -5% in the earlier down market.

The lesson here is that non correlation does not equal negative correlation. Many expect their non-correlated investment to go up while stocks go down – but that won’t always be the case. Non correlated means they’ll do different things, on average! That means one time down, one time up, one time sideways during down markets, and so on – to average out as totally different performance during market downturns. Any one down period, and especially very short ones such as the two listed here, may result in performance you didn’t see coming. That mismatch with your expectations can be particularly exasperated if in a high beta multi-strategy fund which will act way more like the general stock market than their name would entail.

P.S. – Looking for a managed futures mutual fund? Check out the following:

AlphaCentric IMFC Managed Futures Strategy Fund

Catalyst Auctos Multi-Strategy Fund