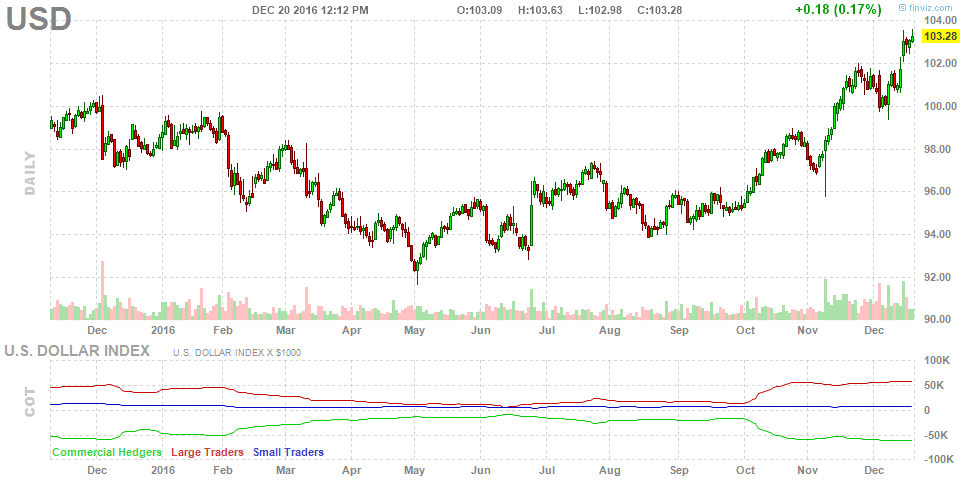

While the rest of the world is talking about new all-time highs in the stock market, there’s another rally that deserves attention, the U.S. Dollar Index. Over the past six months, the U.S. Dollar Index is up 10.42% — a substantial move for the world’s reserve currency.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Finviz

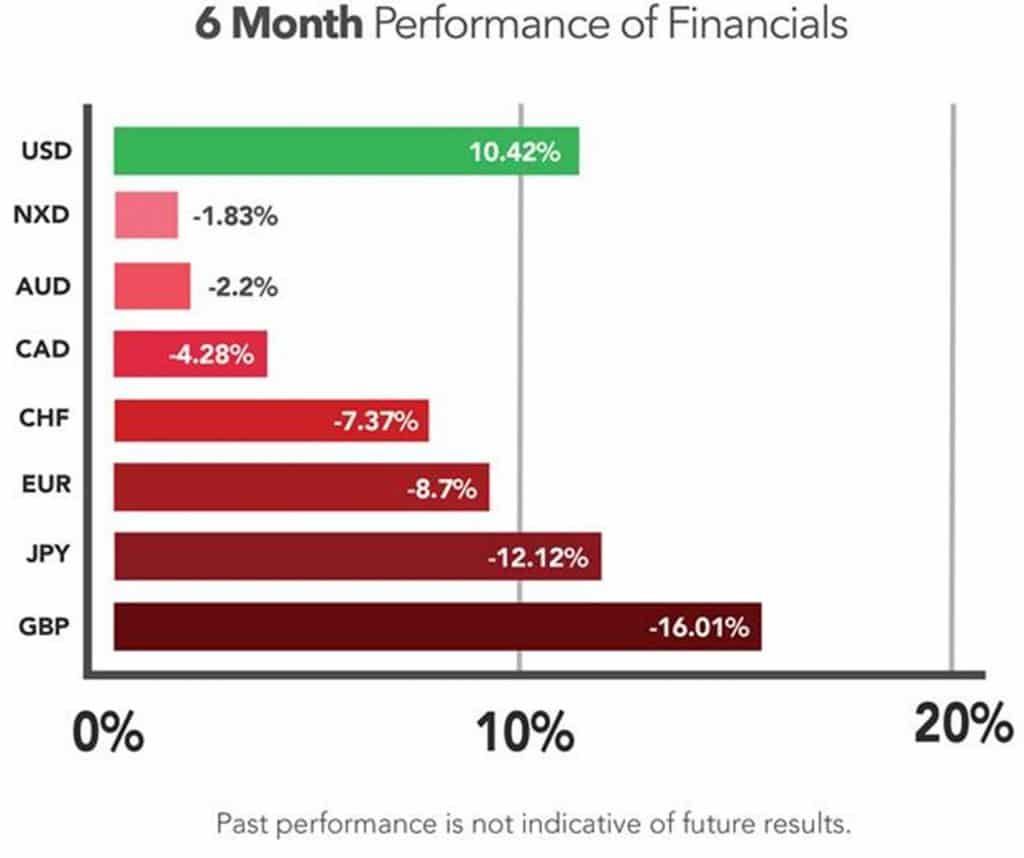

Traditionally, a rally in the Dollar Index has proven to be very beneficial for Managed Futures. That’s because it typically means the other currency markets are also moving with the same sort of depth. Here’s a 6 month look at the performance of the U.S. Dollar compared to the other foreign currencies that the Dollar index is tracked against.

Part of the reason managed futures tends to do well when the US Dollar is trending, is because the U.S. Dollar index impacts almost all commodity futures markets simply because those markets are priced in the dollar. That means, for example, a falling U.S. Dollar can translate to falling prices in dollar denominated futures markets (all else being equal).

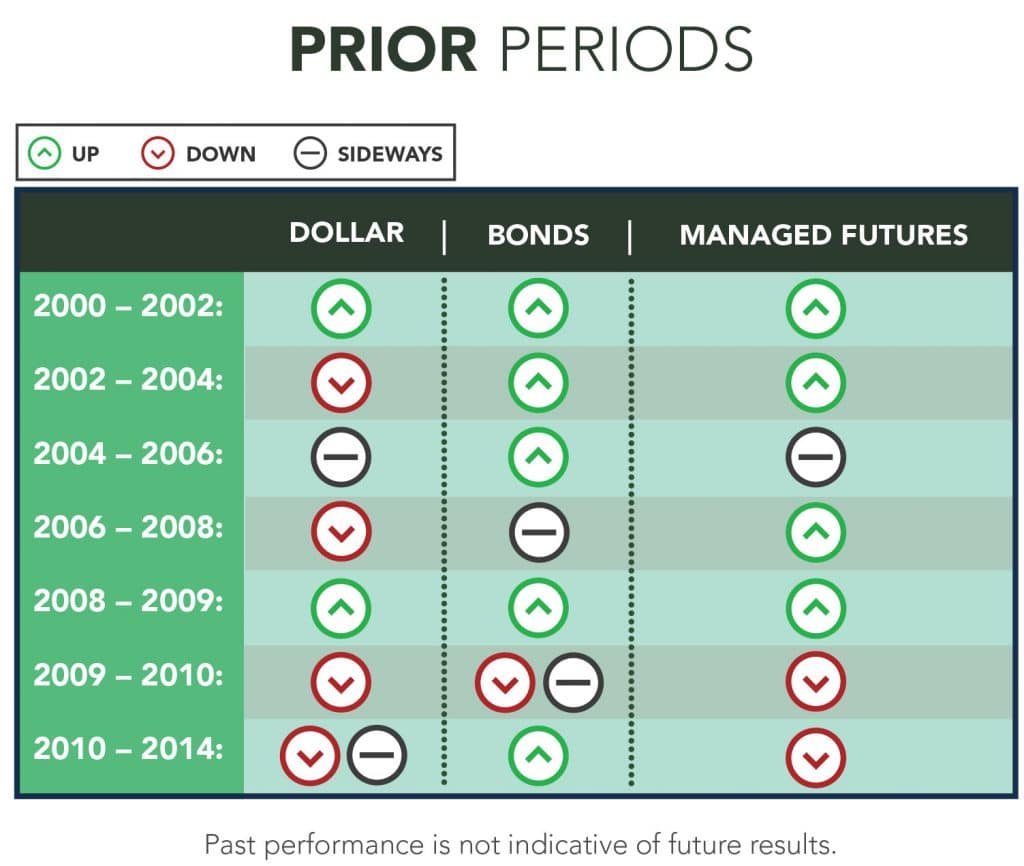

But here’s what things gets interesting. There’s one dollar denominated market that doesn’t tend to fall when the dollar’s rising. We’ve seen a rallying dollar before. We’ve seen falling commodity prices before. But it’s harder to remember an extended period of time we’ve seen both a rising dollar AND falling bond prices (yields rising). Mainly because there haven’t been many recent periods where bond prices were falling (rates rising).

Here’s a quick and dirty look at the recent history of the Dollar and Bonds, as compared to managed futures.

Which brings us to the environment many see persisting for quite a while here – Bonds falling (yields rising) and the U.S. Dollar trending up at the same time. The question on all those allocating to managed futures is – will this benefit or hurt Managed Futures performance? Turns out – no one really knows – because it’s never happened in a meaningful way the past 30 or so years.

The main unknown in this puzzle is how managed futures will perform in an extended rising rate environment. We’ve seen managed futures do well in past rate rising environments, but there’s also warranted debate over whether an extended down move in bonds will be as good for managed futures as the extended up move was.

Grab your popcorn… this is going to be fun.