By now, everyone has crunched the data for the 2016 returns of Managed Futures. Across the indices that track the asset class show it ending the year in the red. Nothing to induce panic and mass outflows (actually quite the opposite), but nothing to write home about either.

But what went on in the Managed Futures world behind the numbers? Which markets made or broke trends in 2016 that led to the collective index performance numbers that symbolize thousands of programs? For that answer, we will point you to our “Managed Futures 2016 Strategy Review.”

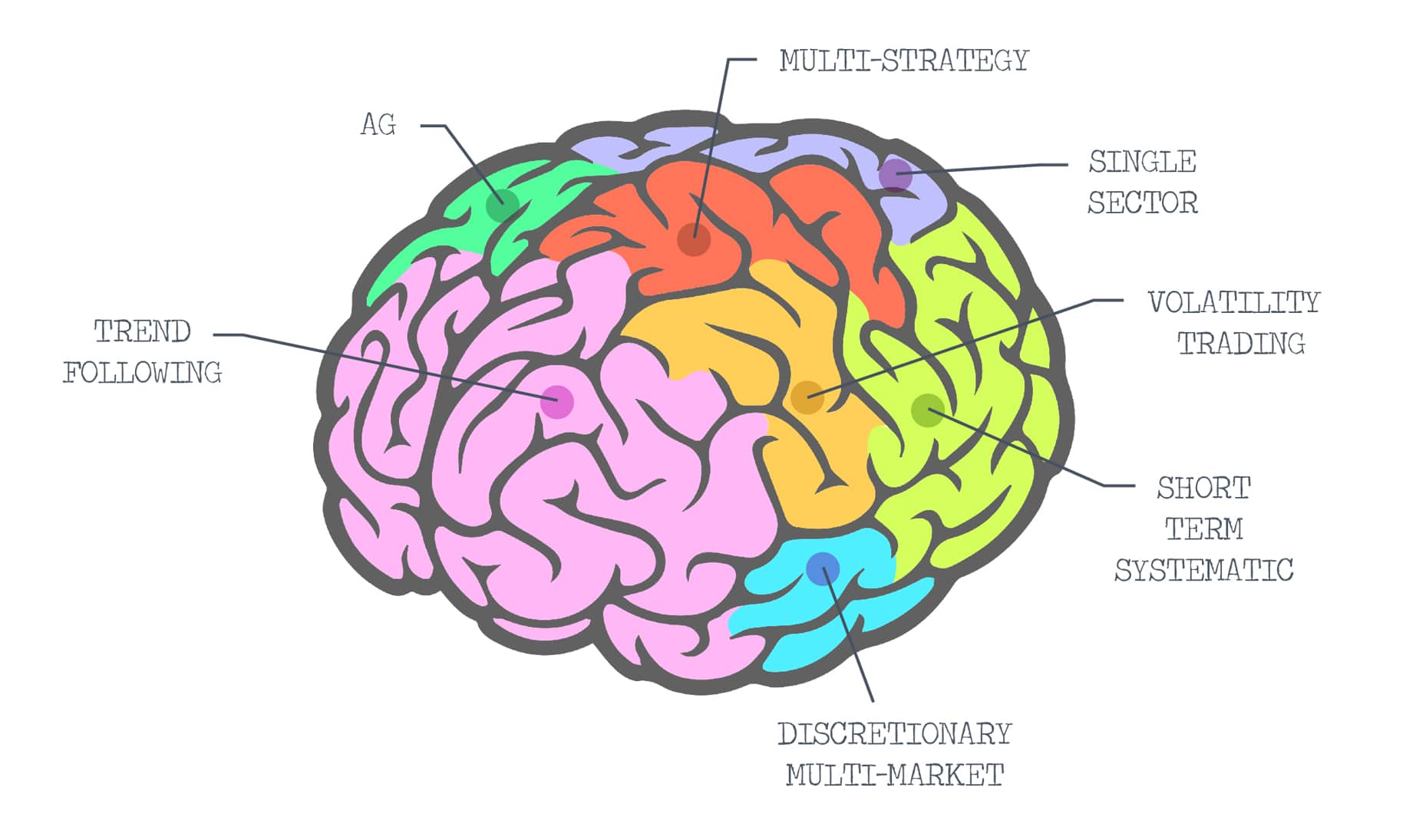

We don’t see the asset class as just the big names or the most popular managed futures mutual funds. In the unique world of managed futures, those programs which make up the asset class can be doing quite different things, as different as short volatility and long volatility, short term and long term, Corn focused or Gold focused. The asset class is like all of our brains in that regard, with the different strategy types all part of the whole (the asset class brain, if you will), with the component strategies making up how the whole responds to market action (what the body is saying to the brain).

In this whitepaper, we outline each of the different types of strategies listed above, delving into the what market factors played a large role in their performance. Here is a preview the most misunderstood sector, short-term systematic.

Overall, the short term strategy performed slightly better than trend followers (mainly due to the moves being shorter in duration), but not as well as we would have hoped.

It’s difficult to categorize this section, with some managers in and out of positions within hours, and others holding multiple days; but generally speaking it was not a good environment for this type of strategy for many of the same reasons as the trend following space – mainly the decline in volatility across financials, which make up the bulk of short term trading strategy portfolios given the greater volume and liquidity there. Remember the days leading up to the election, for example, when uncertainty was in the air and stock markets frozen in their tracks – to the tune of the S&P not moving outside of a 1% range for more than 38 days? That’s bad news for traders who rely on large intraday moves.

Download our “Managed Futures 2016 Strategy Review” to read the rest of the Short Term Systematic review as well as the other sector reviews.