We first published this article on CTA Intelligence.

The short history of volatility trading in the CTA space goes something like this: In the beginning, there were simple option selling strategies that sold out of the money calls or puts once a month until something bad happened. Then strategies got a little more dynamic, doing covered options, iron condors, protecting the wings, and so forth. Then the CME came out with weekly options, opening up a new game board for traders who could collect premium without the extended time risk. And somewhere in there came the VIX futures traders, capturing the option decay via the structure of that futures market versus being short options, while also putting on hedges and even going long volatility from time to time.

Yes, gone are the days of a steady diet of vanilla options selling in the volatility space. What was once a purely short volatility space is rapidly becoming more and more of a volatility trading space (VIX Futures strategies), able to profit from either increases or decreases in volatility, as well as the volatility of volatility itself.

There’s a bevy of new(er) managers who have modeled their strategies around just this sort of thing and analyze all angles of volatility, including the relatively new world of VIX futures and options. There were more than a few VIX futures traders at the MFA conference down in Miami to start the year. But this isn’t just a movement among individual programs. No, we’re also seeing more than a few multi-strategy and traditional momentum/trend following type approaches add volatility trading to their overall models.

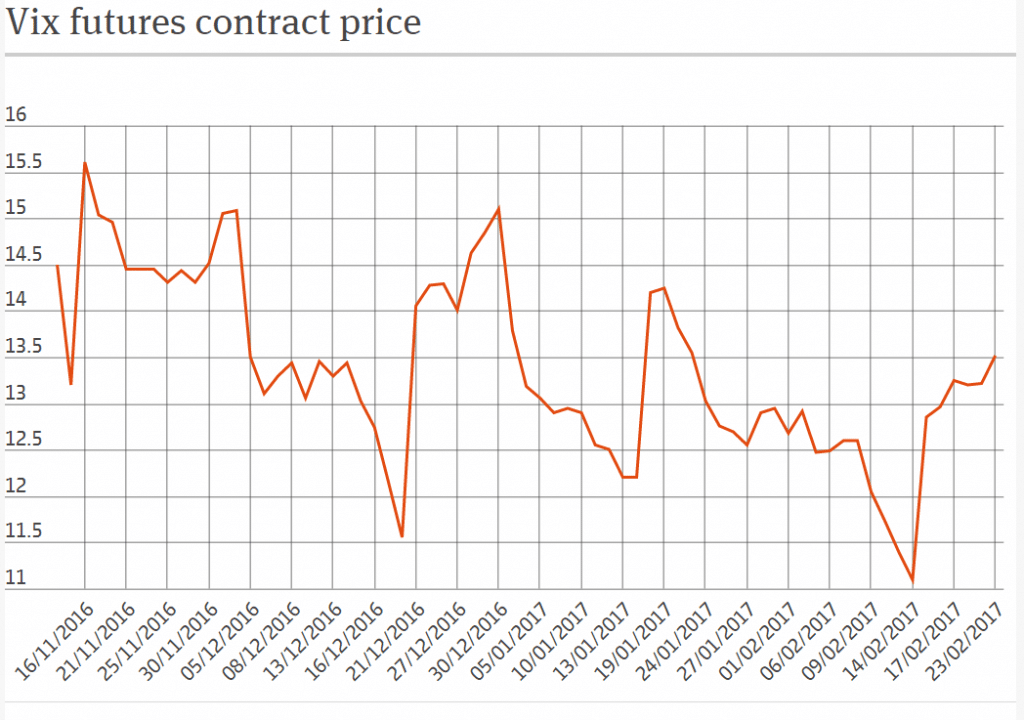

And can you blame them? One look at the VIX futures chart and each contracts uncanny ability to open higher, then revert lower throughout the month to close at the lows, before starting the whole process over again the next contract, and so on and so forth, rinsing and repeating – is enough to make any quant start to see a bit of a pattern there which maybe could be codified/captured in some way.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Source: Quandl

And from our seat, this is becoming an ever more popular trade, with more assets under management and more understanding of the play on ‘market structure’ among investors. Our back of the napkin estimate of the managers we’ve worked with or done our due diligence on comes out to be roughly $750m. When you compare that to the entire Managed Futures space, it’s still but a small speck among the entire industry, but with it being one of the only sectors producing positive returns in 2016, we have a feeling this space will continue to spread its roots and become a mainstream sector in the space. And not just because of performance. Investors are also drawn to it because it can do well in periods when volatility is falling (when momentum strategies tend to struggle), as well as many being generally a low margin usage product with low correlations to the rest of an alternatives portfolio (especially CTAs); allowing investors to add it to current portfolios of managers with very little impact in terms of additional capital or additional portfolio level drawdowns and added volatility.

Yes, what used to be a conversation about volatility and avoiding potential spikes has become a more nuanced conversation also about the decay, the market structure, and the volatility of volatility – as well as the spikes. Now the real question – with the VIX remaining at its lowest levels basically ever, is the tail wagging the dog here? Are these strategies the ones keeping volatility suppressed by selling into every spike at seemingly ever shorter time intervals? Or are they just benefitting from this new volatility environment as covered in our Managed Futures 2017 Outlook.

PS – we’d be remiss to leave out that many of these traders don’t need decaying or falling volatility to earn returns, and would likely take offense to some of our implications above. No. Many of these new batch of traders view themselves truly as traders of a new asset class, volatility, willing and able to capture moves both up and down in that ‘asset.”