Without a doubt, “Alternative Investments” has become somewhat of a buzz word with clients when talking to their advisors. Part of this is because the all-encompassing space has been booming over the past decade thanks to the pain felt by traditional stock/bond investors during the 2008-2009 credit crisis; and part of this is because investors are, for the first time, being able to gain access to investments that offer unique return drivers (aka – hedged, futures, and other non-correlated strategies) in an easy to access mutual fund format.

Not only are investors and advisors interested in “alts,” but they see themselves increasing their allocations in the coming years! That’s the information coming out of a new Whitepaper titled, Alternatives in the Mainstream: A Potential Growth Opportunity for Advisors,” from BlackStone and Investment News.

Perhaps most important, say advisers, is that investors — often unprompted by advisers — are expressing more interest in alternatives. According to findings from recent research conducted by InvestmentNews, 83% of clients have expressed some level of interest in alternative investments.

But interest and actual allocation are very different things, and despite an overwhelming number of people interested in alternatives, it appears the majority of those people still don’t quite understand the ambiguous investment class. Here’s more from the whitepaper:

But alternatives can be confusing. The word itself is over-broad, and means different things to many people. Some investors may turn to them in search of income, or higher returns, some for protection from rising rates and inflation or as a haven from market volatility — and others for some combination of all those. According to this report, 67% of advisers say that a lack of understanding is a key impediment to greater allocations to alternatives.

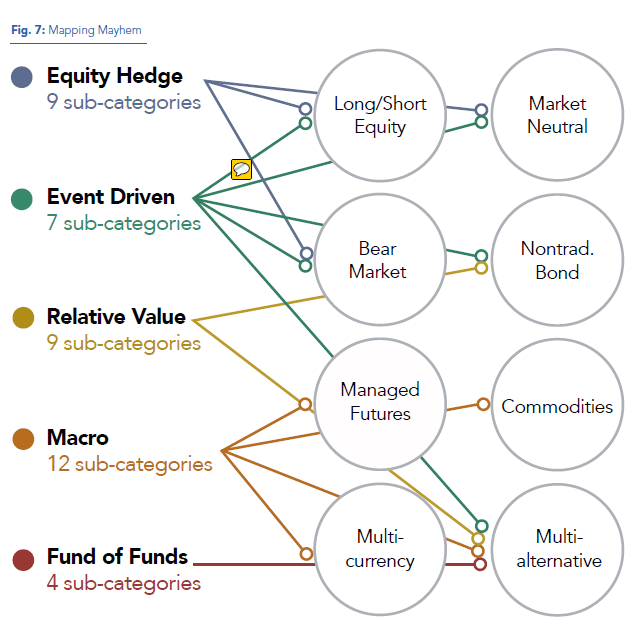

Education is the key? Where have we heard that before? Ahhhh – right here. We do have a pretty active blog, and dozens of whitepapers breaking down alternative investments into their own sub-groups as best as possible. For example, in our whitepaper, “Why Alternative Investments,” we seek to show just how hard it is to understand what classifies an alternative investment.

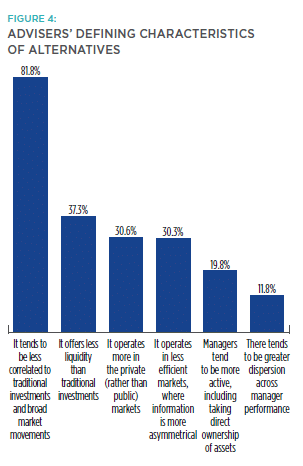

This is just the tip of the iceberg because once an investor has an understanding of what type of alternative investment they’re looking for, they need to make sure it’s providing them what they want. Is it diversification from their current portfolio? Is it providing an extra return? In the Blackstone / Investment News whitepaper, here’s what advisors are seeing as the defining characteristics of alternative investments.

Underlining the interest in portfolio diversification, the defining characteristic of alternatives, say most advisers, is their lack of correlation to traditional investments and broad market movements (82%). In a world where investors increasingly are allocated passively to “the market” through either index funds or ETFs, advisers may see a growing need to diversify away from that tidal movement. Additionally, alternatives are viewed as distinct from liquid, public market investment options, with corresponding benefits (“managers tend to be more active”—20%) as well as liabilities (“offers less liquidity than traditional investments”—37%).

Non-correlation is great and all – but how does one figure out whether the alternative investments they’re looking at display that critical characteristic when its needed most. This is exactly the sort of question we looked to answer in our whitepaper “Truth & Lies in Alternative Investments.” Here’s an excerpt:

In the end, what type of alternative investment you want depends on what you want it for.

If you are looking for a diversifier or even outright hedge against stock market exposure, then most so called alternative investments won’t work. The grand majority, including private equity, hedge funds (most), real estate and commodities (in extreme examples) will show equity like returns during a crisis, because they are reliant on global demand, which can quickly go on strike as we saw in 2008.

Understanding Alternative Investments isn’t easy. We’ve been in the alternatives space specializing in commodities, managed futures, macro, options, and volatility strategies for more than a decade and want to make sure people understand how to access the markets the way they want to. We’re here to help.