In the midst of a quite abnormal run up in the stock market, we thought it might be of interest to review just how consistent the stock market is overall. As of Tuesday, this week, the S&P had only closed down <1% just once over the past 100 days. That’s pretty consistent, but a pretty small sample size when you’re looking at the history of the market. And it doesn’t matter if you only lost more than 1% once if you lost 10 times that on that occasion. No, what people are more interested in when talking about consistency, in our experience, is not how many days were down over 1%, it’s what percent of the time an investment is positive versus negative.

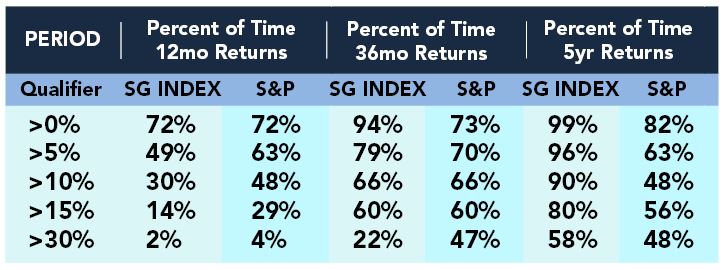

Just so happens we have done the math on this type of consistency before, in our Performance Profile whitepaper; and recently set out to update these numbers to see what the recent period of smooth stock market returns has done for the “consistency” of the S&P; measuring what percentage of the time (between Jan. 2000 and April 2017) the stock market finished in varying positive territories over rolling 12, 36, and 60 month periods. Here’s the breakdown, showing how the stock market is much more consistent on a one-year basis than the managed futures asset class, but much less so on longer 3 and 5 year time frames.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

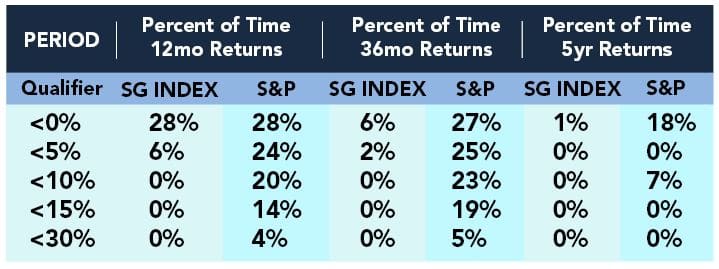

And what about the downside, some would say they don’t care how often they’re up over 30% – they just want to make sure they’re not down double digits over extended periods of time more often than not. Here’s the inverse look, showing what percentage of the time (between Jan. 2000 and April 2017) the stock market finished in varying negative territories over rolling 12, 36, and 60 month periods. We bet the average stock market investor doesn’t believe they’ll be down more than 10% over a three year period about a quarter of the time… but there it is in black and white. Hey, no risk, no return.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

The point of these tables is to compare and contrast the more well-known stock market performance profile with the profile of alternative investments in managed futures, something we highlight in our recently updated whitepaper, “Performance Profile.” Here’s an excerpt:

Here is where we separate the mice from the men, so to speak. See, managed futures may not, in every time period, trounce stocks on the positive side, but they have demolished them on the downside (with no losses more than -10% in any of the 12, 36, or 60-month period). Put another way – if you could have mustered allocations to the components of the Newedge CTA Index at any point in the past fourteen years… you would never see losses more than -10% for ANY one, three, or five-year stretch (and just a handful of periods below -5%). Stocks can’t touch those statistics with a ten-foot pole.

For more on Managed Futures and Stock Market performance comparison, click here to download our Performance Profile Whitepaper.