Raise your hand if you’ve been terribly, awfully, 180 degrees wrong about this nearly 10-year-old bull market at one point or another?

C’mon now, don’t be shy… 2010? 2012 (more than a few were thinking that was “the big one back down”)? Any of these too expensive, too high tops in ’15, ’16, or ’17? We’re all a little guilty, to be sure, if not completely guilty (and shamed) at missing parts of this bull market as we padded our portfolios with alternative investments and hedges and crisis period performers. As we protected against future “Black Swans.” Ooh, what a clever term that was when (financially) coined by Nassim Taleb (see our posts about him here). It was that rare market euphemism that’s at once easily understood and also deeply intelligent. After all, how many actual, physical, aviary black swans have you seen?

For the uninitiated, a Black Swan in the financial world is a “market event” so out of left field and unexpected that it ends up having a deep impact in markets, severely resetting the goal posts as the true risks of a new market environment become understood. Black Monday 1987 is the classic example, but you can also say 9/11, and to a lesser extent the dot.com bust and financial crisis (those were unexpected by many, but outright predicted by some). The whole point of financial Black Swans is that they are statistically not supposed to happen, but there they are – sitting in the middle of the pond.

Which brings us to a question from one of our favorite bloggers – Ben Carlson of A Wealth of Common Sense:

What if the biggest black swan over the coming decades is no black swan events?

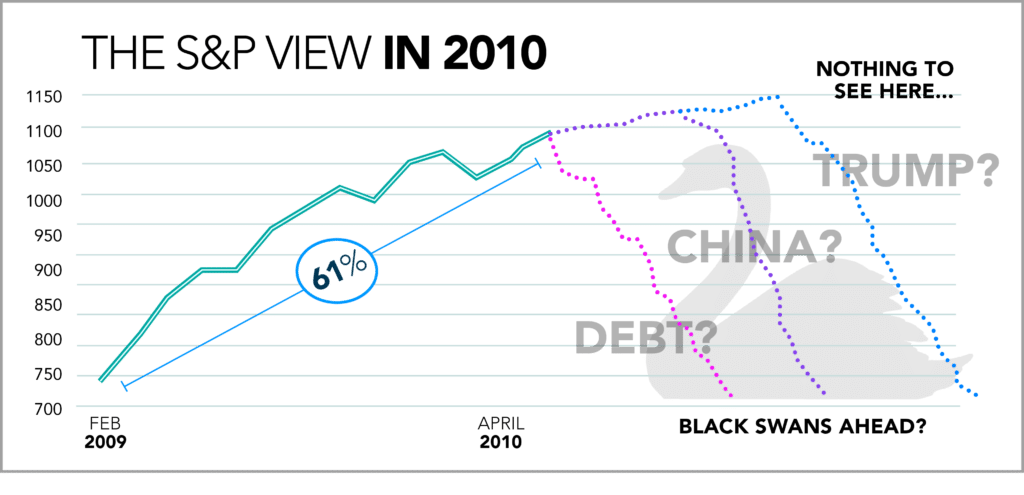

The philosopher in us couldn’t help but jump at that one. What if the biggest truth is that there is no truth? What if the biggest unknown is the known? What if the Bears toughest opponent is… the Bears? We could play this game all day long. But what we found most interesting about it was doing a quick thought experiment and going back about 7 years and asking this question again. Imagine sitting there sometime in 2010 with the market having jumped significantly off its lows, but the ghastly specter of the financial crisis throwing shade over nearly everything in sight. The conversation was swamped with ZeroHedge-type theories on why this or that was going to be the catalyst for the next leg down, how the next big sell off would be like or worse than 2001 and 2008, and how these things were happening with increasing frequency, after all.

The 2010 conversation: A matter of when and what the cause will be, not if…

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

But what if the Black Swan we all knew was coming wasn’t China, or QE, or flash crashes, or Trump, or any of the rest of it? What if the Black Swan we were/have been all worried about was the absence of a black swan, creating a black swan itself? That’s meta and a technical reading of Mr. Taleb’s Black Swan theory would point out that none of those risk factors you read about on the interwebs could have been true black swans, anyway, because they were known. The true Black Swans, according to Taleb, aren’t the known unknowns, but rather the unknown unknowns. And the biggest unknown unknown seven years ago (as we now know with the benefit of hindsight) had to be how high and how big of a rally we could expect with all of the market headwinds that were out there.

The more nuanced question we all should have been asking around Black Swans wasn’t what the Black Swan event would be. A better framing of the question should have been around the costs of an unanticipated event. We all assumed that the costs would be negative and involve a market sell off. But we now know that the cost of the next Black Swan as we sat there in 2010 wasn’t more downside, but the opportunity cost of missed upside.

Turns out, fictional 2010 Ben Carlson was exactly right – the biggest black swan over the next 7 years was the absence of any Black Swans. The biggest risk was the risk of missing out. What we’ll now call, with an assist from @RudyHavenstein, the White Moose.

Is this the opposite of a Black Swan? pic.twitter.com/A0wftTeIpV

— Rudolf E. Havenstein (@RudyHavenstein) August 14, 2017

Which begs the question looking ahead the next 7 years. Stocks are still at all time highs (and very expensive according to all sorts of measures). Rates are still near all time lows. Central Banks still have a bunch of shenanigans to unwind and undo. It’s only natural to worry about all of these as kindling for an unsettling market crisis period. But we need to at least consider (again) that we should be worried (if we can say that about upside) about another White Moose as much as about a Black Swan. They are perhaps equally as rare.