While we inch closer and closer to the day Bitcoin is introduced to the Futures world, the price continues to surge upward. Last week it topped $10,000 – and over the weekend nearly topped 12,000 – putting it up over +1,000% in 2017, making other decade-long trends look like mere blips:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Source: WSJ

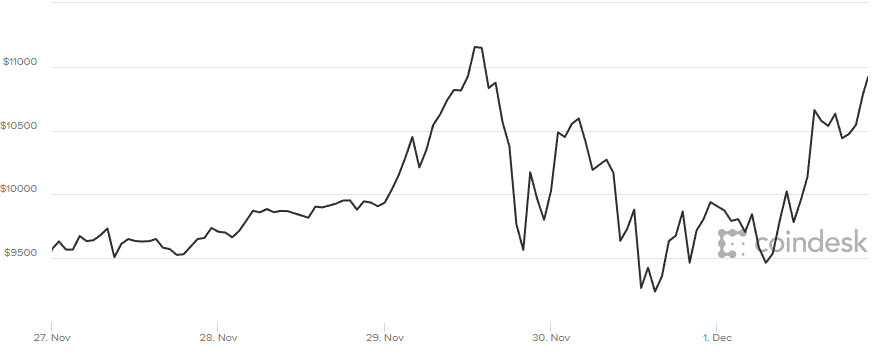

But the granular questions remain: What about the volatility? Like when Bitcoin dropped $1,000 in minutes last Wednesday and fell about -18% shortly after putting in new all-time highs over $11,000 per Bitcoin.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

For those waiting for Bitcoin to hit 50k or 100k, a thousand dollar move is a drop in the bucket, and -18% moves are worth the price of admission. But when it comes to the nitty-gritty of trading futures on this thing, what would such a move have looked like? After all, Black Monday in 1987 saw prices fall -22% in a single day… causing bankruptcies and margin calls and all the rest en masse in one of the worst days ever for not just investors, but Wall Street as a whole. There’s no doubt this could be a contract unlike any other, and it begs the question – just what would last week’s type of move have looked like through the lens of the futures markets?

As we talked about in our Bitcoin Futures Contract Specs article, the CME looks like they’re settling on the rather high level of 35% margin (see #27). So let’s play our a scenario of what it would have been like for someone getting exposure to bitcoin mania thru futures.

Bitcoin Margin

Let’s say someone bought a contract of Bitcoin futures on the “close” Tuesday night around 5pm. The price at the time was 9,961. Now, remember the futures contract only tics around $5 at a time, so the futures contract would have been $9,960 perhaps. That futures contract would have been worth a nominal amount of $49,800 (the 9,960 price per bitcoin * 5 bitcoin per contract). That means a futures trader would need to have about $17,500 (35% of $50k) to put on a single Bitcoin futures contract. Fast forward to the Wednesday highs where bitcoin was up just over 13% on the day, standing at $11,290, and your single futures contract would have been up to $6,645. The margin, however, if the CME goes to a daily changing of the margin – which would be somewhat unique – would now stand at $16,935, having increased the same 13% the end price did.

Fast forward to the “lows” on Thursday, where prices had dropped 18% from the highs down to about $9,200, and our theoretical investor trader speculator would have lost about $10,500 in open trade equity from the highs, and be down about -$3,800 on the trade put on Tuesday night, leaving the account at $13,800. That’s right, this investor would have seen their $17,500 account climb up to $23,645 (a 37% gain… in a day), and then be nearly cut in half by falling more than $10,000 (-44%) down to $13,800.

Now, the required margin would have fallen the same 18% from the highs, leaving it at about $17,325, which would put the account of just $13,800 on margin call, needing to deposit $2,400 to remain in their position. The CME and FCMs have come up with something called maintenance margin to lessen these types of swings and need for money to be sent back and forth… with the maintenance margin typically some smaller percentage than the initial margin requirement.

At this point, it doesn’t look like the CME is thinking about a different (lower) maintenance margin amount, so it will be interesting to see how the margin game plays out with the Bitcoin futures. Suffice it to say margins jumping around 10% day to day is not exactly normal practice, even for commodity markets thought of as quite volatile. Will the CME and FCMs recalculate margin on a daily basis? Hourly? Will FCMs just require some multiple of the exchange limit (like 1.5x) to smooth out that margin requirement volatility for clients? All this remains to be seen, but its important to a fully functioning futures ecosystem, which has about half of the FCM’s we work with eager to get things going in Bitcoin futures (more trading = more money); and half not as welcoming of the pending futures contract. On particularly vocal opponent has been the typically vocal Thomas Peterffy, the chairman of Interactive Brokers, who took a full add out in the Wall Street Journal says it’s just too soon for Bitcoin futures:

“Cryptocurrencies do not have a mature, regulated and tested underlying market,” he said. “The products and their markets have existed for fewer than 10 years and bear little if any relationship to any economic circumstance or reality in the world.”

“If the Chicago Mercantile Exchange or any other clearing organization clears a cryptocurrency together with other products, then a large cryptocurrency price move that destabilizes members that clear cryptocurrencies will destabilize the clearing organization itself and its ability to satisfy its fundamental obligation to pay the winners and collect from the losers on the other products in the same clearing pool.”

When Bitcoin futures hit the markets in a couple days, it will be interesting to see how many traders are new to futures realm, how many of them understand how often they might be on margin call, and how much time they might have to spend making sure they stay in the market.

Bitcoin Price Limits

One bit of protection against the dangers envisioned by Mr. Petterffy the exchange will employ is price limits, where trading is halted for a time when and if certain circuit breakers are hit on both the up and downside. The CME has put in limit moves very similar to those in place in the Emini S&P contract for bitcoin’s limit moves:

Price limits for a given Business Day are calculated in relation to a reference price, which generally will be set at the most recent Bitcoin Futures settlement price, calculated at 4:00 p.m. London time each Business Day. The reference price may be adjusted at the sole discretion of the Exchange to incorporate BRR changes on non-trading days. A price limit of 20% above or below the reference price and special price fluctuation limits equal to 7% above or below the reference price and 13% above or below the reference price apply. Trading will not be permitted outside of the 20% range above or below the reference price.

The idea here is that any sort of flash crash or the like will be met with cooler heads when everything is put on pause, and buyers (or sellers) will come back into the market once they see there’s a pause. Some of that is wishful thinking, of course. Back in 2014, the Lean Hogs market had at least 7 limit moves, many of which were in the same direction and occurring day after day, leading the CME to announce they are expanding limit moves in the Hog market. And there’s the little problem that if Bitcoin goes to $0 overnight because one entity gains control of 51% of the network, there’s a crack of the encryption, or similar – the CME can halt trading all it likes, but you’ll be hard-pressed to find any buyers of the futures when the index is at zero.

We’ll all get to see what happens in real time, very shortly. This Sunday for the CBOE’s product, and the 18th for the CME’s.

Investing in Bitcoin Futures

New to futures markets? Need help understanding how margin works, this crazy $5 tick size, 5 bitcoin contract size, etc? We’re here to help. Call us at 855-726-0060 to talk to one of our professionals about setting up an account. And/or check out this idea we have for gaining exposure to some of Bitcoin’s upside, while trying to eliminate most of its downside.

hbspt.cta.load(313774, ‘7d8b3e7f-5588-4746-a9c0-20e67b3825b5’, {});

hbspt.cta.load(313774, ‘7d8b3e7f-5588-4746-a9c0-20e67b3825b5’, {});