We recently sat down with the folks at ReSolve Asset Management while both of us were participants on an Opalesque Roundtable here in Chicago, and loved their flare for explaining in depth concepts in simplistic ways. What we found particularly interesting is the way they think about diversification (bikes and skis). They’ve already brought into question the way we think about correlation, and diversification and correlation go hand in hand. So why talk about diversification when it has been covered by just about everyone? Well, Resolve finds there are still many investors who don’t quite get how it works in practice… in real time. They explore their thoughts in their recent whitepaper: “Ski & Bikes: The Untold Story of Diversification.”

The most fundamental principle of investing is diversification. But in our experience, few investors understand what diversification means. Sure, investors typically understand that diversification means “don’t put all your eggs in one basket”. Some also understand that diversification is about owning a combination of investments that zig and zag at different times. But when we probe a little deeper, it seems many investors are still confused about how diversification works in practice. They wonder, “If I’m buying something that makes money when the other is losing money, doesn’t that just give me a zero return?”

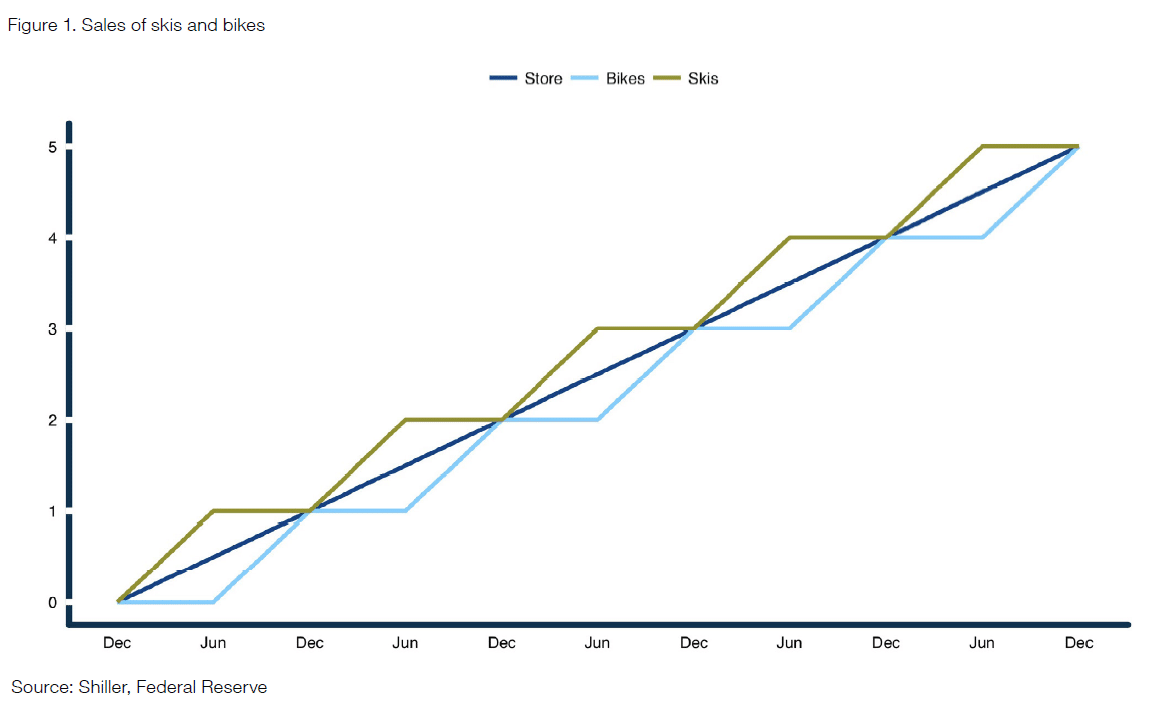

Well, no, just because one thing loses money while another makes money, doesn’t mean the combo ends at zero. They use the following graphic, courtesy of the Fed(?), showing ski stores doubling as bike stores in the summer, to diversify their profits.

In most parts of Canada, we have very distinct seasons. Some months of the year are temperate and relatively dry, while other months are cold and snowy. As a result, most Canadian towns of any size have stores that sell skis and bikes.

The skis and bikes example….shows how deriving cash-flows from two independently profitable businesses, which produce returns at different times, reduces the variability of cashflows throughout the year.

Of course, they argue, you could just exit the ski and/or bike business and invest in bonds or some other low yielding investment. But this is about diversifying returns, not necessarily reducing risk. Investors, whether it be in ski/bike shops or private equity – are looking for return. It isn’t just an exercise in reducing risk as much as possible. Which leads to their main point:

The magic of diversification is that it allows investors to keep more of their money invested in higher risk assets, with commensurately higher expected returns, while lowering the overall risk of the portfolio.

Coming back to the ski/bike example, ReSolve makes the point that investors seeking diversification must be willing to look “further afield.” It’s easy to know that a bike shop may generate returns in the summer than a ski shop, with one reliant on warmer weather and one reliant on colder weather. But not as easy to understand whether Emerging Bond Spreads have a differently timed return stream than Developed Real Estate. When is summer and winter for bonds? Resolve tackles that nuance in the following graphic, detailing different asset class behaviors across different market “season.”

The lesson is that diversification has very practical benefits, but only for investors who can think more broadly about the world’s many sources of returns; most portfolios fail to invest in diverse assets that thrive in different economic states.

To read more about their more sophisticated approach to correlation, diversification, and portfolio construction, click here to download their whitepaper.