Just throwing something into a portfolio labeled an Alternative Investment is likely going to be a mess. But a lot of times, that’s what happens. A client listens to the words Alternative Investments, but hears the words diversification and stabilization and all the rest. Before you know it, some random Alts strategy is in a portfolio and doing its thing. Problem is, that ‘thing’ might not be all that alternative, or not the type of alternative you want, making it a bit of a total trash fire in there.

Having assisted clients in allocating to more than 100 alternative investment programs over the past 15+ years, we’ve seen those clients who had success (and those who made a mistake or two, or twenty).

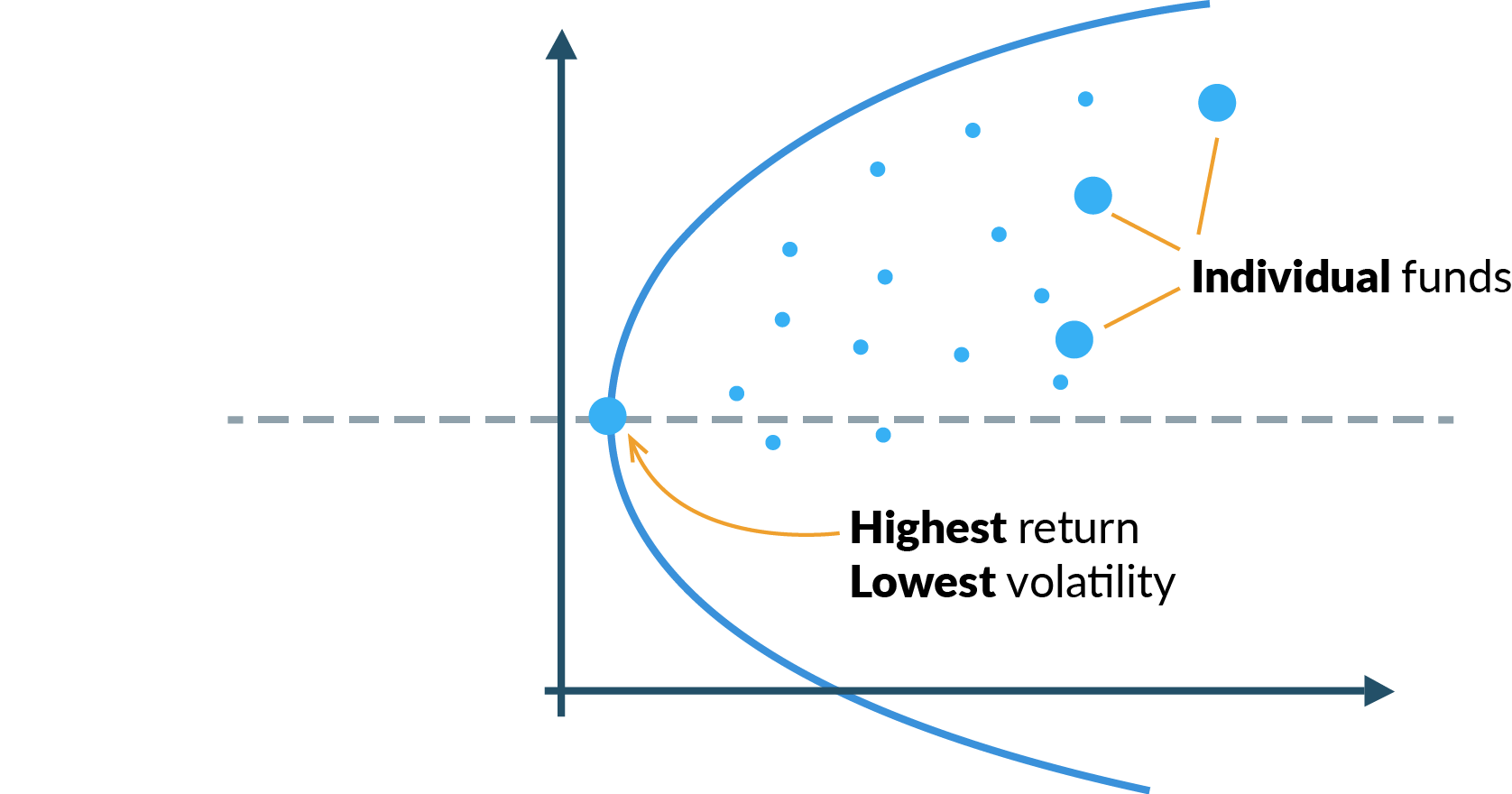

Here are some basics to insure you’re getting what you want out of your Alts allocation when putting together Alternative Investment portfolio:

1. Define the role of the Alts in the overall portfolio.

Determining the goals for the overall portfolio is the first step to Alternative Investment success. Are you looking for crisis control, an all-weather investment, something that performs well during inflation?

The classic error here is someone who needs (or wants) crisis period protection via an Alt which tends to provide negative correlation to the overall market in an extended down move, but ends up with something like a yield enhancement strategy via option selling, that ends up being positively correlated in a crisis.

Make sure to look in the mirror and ask if the portfolio needs crisis period or absolute returns. Most are tempted to say absolute returns, but then a deep understanding of how those absolute returns are generated is a must. If they are generated via a negative skew strategy that is likely to struggle/suffer when volatility spikes, it may not be exactly what is wanted out of your Alts.

It’s almost better to ignore the statistical correlation of the Alts investment you are looking at, and instead ask how it would perform during the type of traditional investment “crisis” period you are worried about.

2. Align your preferences with Alts role

Closely on the heels/heavily related to the role of Alts in the portfolio is understanding the type of program that you will have the best chance of sticking with. All too often, there is a big difference between what an investor thinks they want out of their Alts allocation, and what they are actually willing to endure.

The classic example of this is positive skew versus negative skew strategies. The former tend to have longer periods of flat to down performance interspersed with rarer periods of large outperformance. Think – buying an option. While the latter tend to have periods of small, consistent gains, interspersed with rarer periods of sharp losses.

If you are wanting your Alts to play the role of crisis performer (positive skew, rare periods of sharp gains), but used to a bond market type investment that churns out consistent yields month after month, you’re going to be disappointed and likely drop the investment before it performs the role you hired it for.

3. Think about your access point:

The classic error here is spending a ton of research time and energy to find the best talent to fill the role you want in your portfolio, only to find that you can’t afford managed account access or your custodian doesn’t have it approved on their platform, and so forth.

Successful portfolio construction requires some thought into the access points you are willing and able to accept. The ideal is a portfolio of programs accessed via managed accounts for maximum capital efficiency via cross margining. But what do you do if your ideal program might not be able to offer that – are you ready to go into privately held funds or give up the tax advantages of direct access by going through a mutual fund?

- Managed Accounts

- Benefits: Cross margining, leverage, ultimate in transparency and liquidity

- Cons: higher investment minimums, extra work setting up

- Privately Held Funds/Commodity Pools

- Benefits: taxed on performance net of all costs, allow manager max granularity

- Cons: lengthy subscription docs and process, less liquidity and transparency

- Mutual Funds

- Benefits: no subscription docs, just click to trade

- Cons: no 60/40 tax treatment pass through, watered down versions

4. Look at waaaay more than Performance

To really build a legit portfolio, you need to understand how the pieces work together. Not just how they have performed together. This includes a deep dive into just how each strategy earns or loses money via a few of the following methods, and insuring you aren’t doubled up or overexposed to any one set of factors affecting each program’s ability to earn money or threat of losing big money:

- Analysis of Core Strategy

Looking into momentum, mean-reverting, pattern recognition, and timing. - Payoff Analysis

What trade offs are being made for a model’s return. (i.e. selling weekly options = risking $50k per trade to make $500 per week) - Death Analysis

What confluence of events would have to transpire to ‘break’ the strategy? - Firm/Principal Analysis

“Disappointment with investment manager selection can be reduced by considering the tangible ‘4 P’s’ (people, process/philosophy, portfolios, and performance) and the intangible ‘4 P’s’ (passion, perspective, purpose, and progress).” (CFA Institute)

5. Be aware of fees, but not to a point where it oversteers your actions

A simple one here. Nobody wants to pay 3 & 30. But if they return 20% AFTER those fees, are you going to throw them out before even looking into what they do? Be aware of the fee level, but be careful filtering out solely on fees. This isn’t the world of Large Cap U.S. stock mutual funds where there isn’t a clear ability for any one mutual fund to outperform another – making it logical to fall back to fees as the tiebreaker. Outside of pure trend following as a beta component, programs are doing different things where choosing on fees alone could be shortsighted.

6. Pre-Define your RISK goalposts for each manager

The strategy analysis can give you a good handle on what exactly would have to happen in order for an investment program to completely break, but the truth is often more nuanced and buried than that. The questions you will face in your portfolio as it moves ahead is going to be more like what to do with a program that has been flat for years, instead of what to do when a program draws down -25%.

The worst performing portfolios we see are ones deconstructed and quickly patched back up in a knee jerk reaction based on recent performance. Investors can go a long way towards avoiding that fate by pre-defining what failure looks like for each manager in their portfolio. Should it make a minimum amount of money every xx years? No monthly losses below yy%? Volatility always less than zz%?

By defining these ‘goalposts’ before the first trade is made, you’ll have a yardage book of sorts, for all those golfers out there, to reference when you are faced with a tough choice (golf shot). If it hasn’t violated one of your rules, let it be. Let it work.

7. Determine your portfolio weights

Now that you have your perfect portfolio balanced between this strategy type and that, offsetting that model risk with this one, and so forth – the biggest choice remaining is how to weight each allocation within the portfolio.

The classic error here is to base allocations on the manager minimum investment amounts, without considering the risk of each program. Imagine two $1 million minimum programs, one with average margin to equity of 25%, and another with only 5%. One with a maximum drawdown of -50%, another with just -10%. If you create a “balanced” portfolio equally weighted with $1 million invested in each manager, you will be far from balanced on a risk basis. The former manager (25% margin to equity, 50% drawdowns) has 5x the risk profile of the latter one, and you will quickly find it dominating the performance on a day by day basis, rendering all your portfolio work a bit useless.

And what about re-balancing. Say you’ve perfectly risk balanced them, but one earns 5x more in the first year – you’ll want to re-balance at some set interval to keep the portfolio structure intact.

(7.5) Partnering for Success

Building an Alts portfolio is no small task, and at the end of the day – we recommend, as we crudely put it in a post a few years ago, to Outsource that S*&4.

RCM Alternatives specialty is building successful portfolios in the alts/managed futures/macro space. That’s been our day-to-day job in working with investors for more than a decade, with our experienced team up to the challenge of finding unique managers to fit unique needs. Contact our team to help you get started.