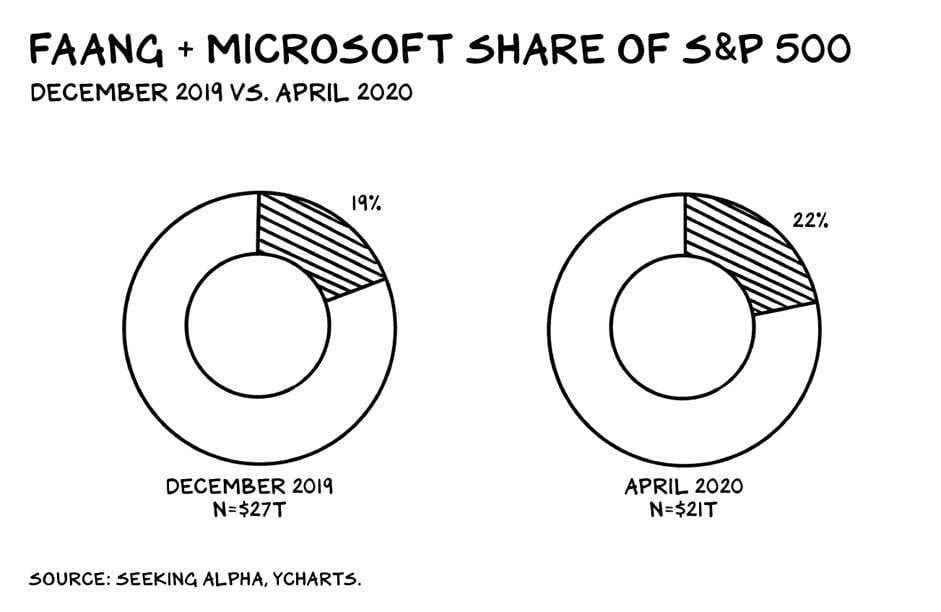

Everyone who had a betting ticket for U.S. markets back at all-time highs before lockdowns ended – please raise your hand. This was the mother of all White Moose, galloping down the stream right as everyone was screaming about Black Swans and Gray Rhinos. The move off the March 23rd lows has been nearly as sharp as the selloff that brought us down there. BUT, this is not a broad based rally. There are distinct winners, like Amazon (up 37% YTD), Netflix (+30% YTD), and Tesla (+127% YTD). Those are the YTD returns, not the returns off their lows in March. Investors are saying the new world we now occupy will be even better for these tech behemoths, as is reflected in the outperformance of the Nasdaq versus the S&P 500 (15% ish outperformance) and by large cap vs small cap (11% ish).

That’s some impressive outperformance, UNTIL… you look even closer and separate out the truly techiest of tech and biggest of the big – FAANG = Facebook, Apple, Amazon, Netflix, Google. Or, as the NYSE has ferreted out, FANG +, which also includes Alibaba, Baidu, Nvidia, Tesla, and Twitter. In the immortal words of Crocodile Dundee, FANG+ looks at the Nasdaq’s “knife” and says… that’s not a knife… THIS is a knife.

And what a “knife” it is. The FANG+ index (as represented by the ETN/ETFs here for ease of compiling the comparisons, and as of June 8th) is 16% ahead of the Nasdaq and 31% better than the S&P. Thirty-one! What is happening here? Well, part of it is the accelerated move to online shopping and digital products bought about by the Corona lockdown. Part of it is just the continued “winner take all” online economy. Could you really launch a competing product to Amazon or Twitter these days? They have the network effects and access to cheap capital and raging stock prices to call on at any point. As the FANG (he calls it the “The Four”) expert Scott Galloway puts it in a recent post:

The Four — Amazon, Apple, Facebook, and Google — are an invasive species that, over the last decade, have compromised the immunities of the retail and media sectors. Spend has rushed toward digital, where apex predators take 1 of 3 e-commerce dollars (Amazon) and 2 of 3 digital marketing dollars (Google/Facebook). Covid-19 is just finishing the job that the search and social firms started.

The only investment strategy, portfolio, or retirement planning any person needs is the following: Buy the stocks of firms that are unregulated monopolies and nothing else. I’ve followed this dictum for a decade, and it’s worked … well.

We echoed these thoughts in our 2018 Managed Futures outlook:

America has shifted its faith to a new set of “American Gods” – namely the Four (as Scott Galloway labels them in his wonderful book): Amazon, Apple, Facebook, and Google.

All of the things we once held sacred are being chipped away at and destroyed. Sometimes purposefully and sometimes just out of spite or for fun. Our faith in the conventions of American government and these institutions isn’t just fading away…it is being transferred.

…we’ve selected a new Pantheon [Apple, Facebook, Amazon, Google]. We have more faith in their ability, their capacity to learn and improve, their adaptability, than we have in the President or in Congress or in the courts.

While macro economists and traders may be looking at tensions in the middle east, policy coming out of the White House, saber rattling with North Korea, and all the rest as reasons markets may do this or that. The new truth may be that none of that matters as much as $NFLX subscriber growth, Tesla’s Model 3 production, or iPhone sales. Amazon doesn’t much care if the government shuts down, people still want their order the next day and Amazon’s servers and warehouses full of robots will get it to them. Tesla probably benefits if there’s geopolitical unrest in the Middle East. Likewise, the crazier things are in Washington – the more searches and posts of interest on Facebook and Google. And with near constant shift to passive index funds, the power of these companies in our real economy is becoming power in the markets, dictating how traders react to other influences. Put simply, it’s going to take a lot for investors in these companies to sell, much less sell in panic to drive volatility across multiple asset classes.

There’s no doubt these large tech firms are becoming an ever-larger part of our society, our stock markets, and our world as a whole. What do we do about it?

Fang+ Futures

We’re not going to tell you whether this trend will continue or start to unravel. Before the crisis, there was talk of breaking up big tech… but now, they’ve been an essential service for information, food delivery, and more; becoming even more entrenched. But the hedge funds and traders we work with won’t fall on their sword one way or the other on this trade. They’ll just look to harvest the volatility and outperformance of this group against the other benchmarks and stock index futures markets. The fact that FANG+ is equal weighted versus market cap weighted for other indices opens up some specific opportunities.

Enter FANG+ futures, which were launched in November of 2017 and have been slowly gaining steam as a legitimate futures contract, with volume up to around 1,500 contracts per day. If you like/need volatility in the markets you trade… if you need/want to hedge some Amazon/Tesla/etc risk… if you want a more capital efficient way to buy and hold these stocks…. FANG+ futures are worth a look.

Exchanges are notoriously bad at marketing their products, with often too dry materials showing contract specs and so forth; but The ICE does a pretty good job with their resources here:

Intercontinental Exchange Disclaimer

Apple® is a registered trademark of Apple, Inc. Facebook® is a registered trademark of Facebook, Inc. Amazon® is a registered trademark of Amazon Technologies, Inc. Netflix® is a registered trademark of Netflix, Inc. Google® is a registered trademark of Google, Inc. Alibaba® is a registered trademark of Alibaba Group Holding Limited. Baidu® is a registered trademark of Baidu.com, Inc. Nvidia® is a registered trademark of Nvidia Corporation. Tesla® is a registered trademark of Tesla, Inc. Twitter® is a registered trademark of Twitter, Inc. S&P 500® is a registered trademark of Standard & Poor’s Financial Services LLC. NASDAQ-100® is a registered trademark of NASDAQ, INC.

None of the foregoing entities are affiliated with, endorsed by, or sponsored by Intercontinental Exchange, Inc., or any of its subsidiaries or affiliates, and the inclusion of the entities on our web site does not evidence a relationship with those entities in connection with the Index, nor does it constitute an endorsement by those entities of the Index or NYSE.

NYSE FANG+ Index is a trademark of ICE Data Indices, LLC or its affiliates (“ICE Data”) and has been licensed for use in connection with the NYSE FANG+ Index Futures. The NYSE FANG+ Index Futures is not sponsored, endorsed, sold or promoted by ICE Data Indices, LLC. ICE Data makes no representations or warranties (i) regarding the advisability of investing in securities or futures contracts, or (ii) that any such investment based upon the performance of the NYSE FANG+ Index particularly, or the ability of the NYSE FANG+ Index will track general stock market performance