We came across this great post recently on the Breaking the Market Blog comparing Tiger Woods strategy on avoiding errors is just the sort of thing to apply to an investment strategy.

Golf is often pretty clear at telegraphing the penalty for misses. Water on one side is more penalizing than the open green to the other. The consequences of the misses are rarely equal.

[while counter intuitive]… you might aim away from the target — the maximum return. I explained how the error in measurements and estimates ensure you will not hit the target — the top of the return curve. The charts implied a miss left and a miss right were symmetrical around the top. But are they really? Are the impacts of errors to the “left” the same as errors to the “right”?

Are there hidden water hazards in the investment world?

There sure as heck are! Not to mentioned hidden sand traps, out of bounds, and all sorts of other penalty strokes out there waiting to be assessed. We spoke about this in our recent podcast with Corey Hoffstein (see here), with Corey labeling it a “latent risk factor that hasn’t shown up in the return stream…yet.”

Where we see this in investors who can be lured into picking a portfolio of Alts investments that are non-correlated and produce a stellar return when combined together. The trick is, those programs’ correlations to one another aren’t etched in stone somewhere. They can and do and will change, especially during a crisis period or other market event which puts stress on some aspect of the portfolio. And that error, or wayward shot to keep the golf metaphor going, can really kill your round/return expectations. Here’s @breakingthemarket again:

…the positive consequences do not counteract the negative ones.

The errors in your favor (overestimated) helped the portfolio by 1.18%. The errors not in your favor (underestimated), hurt the portfolio by 1.71%.

Errors which move the portfolio “past the peak” hurt the portfolio returns more than errors to the left.

The errors are convex in their consequences… [and] by leveraging it, we can see that leverage magnifies the estimation error.

The antidote, can often be separating the statistical correlation readings with a more “fundamental” approach which considers the return drivers of the programs you’re investing in. If you have three programs that are statistically non correlated, but that each do a flavor of momentum type volatility breakout strategy – they are apt to be more correlated at some point in the future than you bargained for. Better to plan for your errors and hit a safer shot by not putting the whole tournament on your one big assumption (that correlations will persist). Better to see what the portfolio looks like assuming an unwinding of those correlations. We do a very simple back of the napkin approach with clients at RCM for this type of reality check.

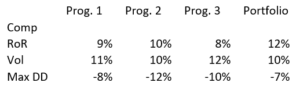

Say you have three different investment programs with the following risk/return metrics, resulting in a portfolio which is greater than the sum of its parts due to the magic of diversification (hitting the perfect shot in golf lingo).

Who wouldn’t want that power of diversification reduction in the DD? Our advice in these scenarios is a simplistic version of Tiger Wood’s strategy of strategically managing misses. We simply ADD the max drawdowns of each component manager as a sort of worst case error check. Here, if all programs hit their worst max DD at the same time – an unlikely, but greater than 0% chance of occurring event – the investor is looking at a maximum drawdown of -30%. More than 4 times the “perfect shot” drawdown of -7%. If that’s acceptable, you move on and you take the shot. If you think that may lose the tournament – you reassess the portfolio and consider reducing some exposure to make that miss more acceptable. That’s how you stay in the game with the chance of winning a major!