Decisions made by international leaders rarely affect the world of managers, programs, or the managed futures space, let alone the grain markets… But that might not be the case this time… Confused?

First, we must catch ourselves up on what’s happening in eastern Europe. Understanding the happenings in Ukraine over the past week can be difficult. We don’t specialize in politics, let alone international relations, so with a quick Google search, we found a fast read by ABC to get you caught up on the Ukrainian protests. Cultural differences in Ukraine have been prevalent since the country’s inception. However, the catalyst of the conflict boiled to the surface because of a back out of a trade agreement by the President of Ukraine.

“Why are they protesting?

But they are very angry because Ukraine’s President Viktor Yanukovich backed out of a trade deal with the European Union last week. This wasn’t just about a trade deal, it was a symbolic decision about the future of the country: Would Ukraine be allied with Europe or with Russia?”

To make matters worse, just before the weekend, Russian President Putin sent forces into Ukraine, and made warnings of war. Here comes the (Ah-Hah moment). For those unaware of Russia’s and Ukraine’s agricultural history, they happen to grow and harvest around 17% of the global wheat supply, and 16% of the corn supply via Reuters.

“Wheat, corn surge as market frets over Ukraine The U.S. Department of Agriculture forecasts that Russia and Ukraine will export a total 26.5 million tonnes of wheat in the 2013/14 marketing season, or 17 percent of global shipments. In corn, Ukraine alone is forecast to export 18.5 million tonnes, or 16 percent of total exports. But analysts and traders said there were no signs so far of actual disruption to trade and that the market was reacting nervously.”

The question remains… with rising political unrest, the Ukrainian President fleeing the country, are these events halting countries from exporting grains? An ADM spokeswoman says, not at all, via the Wall Street Journal.

“Archer Daniels Midland Co. said its Black Sea grain-trading operations haven’t been affected so far by the escalating turmoil in Ukraine, though the commodities company is watching the situation closely. We haven’t seen any significant impact to business and continue to monitor the situation.”

As uncertainly continues, the two ag markets did see some grain gains today (Corn up 1.2%, Wheat up 4.5%), but nothing that couldn’t happen any other day. {past performance is not necessarily indicative of future results}.

(Disclaimer: Past performance is not necessarily indicative of future results)

Charts Courtesy: Finviz.com

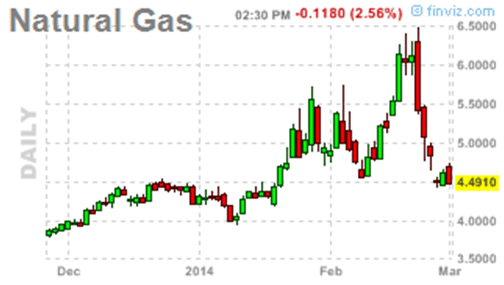

These modest gains today could easily disappear the next. Speaking of disappearing… There’s one other commodity that’s deeply rooted in this conflict… Natural Gas. The Washington Post reports that Russia supplies Ukraine with half over their natural gas needs… but after supply cuts, trade disagreements, and other emerging European suppliers, Russia is getting left in the dust.

“In December, Gazprom said it would discount the price paid by Ukraine, cutting it from about $11.50 per thousand cubic feet to $8.10. But that only brought Ukraine’s prices roughly in line with those being paid in other parts of Europe. Gazprom said it would review the price every quarter, meaning a new reset is possible at the end of March.”

As far as the futures markets go… Natural Gas has lost all of what it gained in the month of February and then some… remaining unfazed by the disagreements in Europe.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Finviz.com

Is this just the beginning? Will Russia use their physical force? Will Ukrainian protesters win out? Will this turn uglier than it already is? Will other nations get involved? While it’s fascinating to hear how commodities such as Natural Gas can play a deep role in a gripping political story in Europe, as a whole, traditional managed futures won’t pay too much of attention to Ukraine (outside of personal interest) regarding the corn, wheat, or natural gas markets. Managers pay attention to various markets indicators like moving averages, and multiple week lows.

Disclaimer

The performance data displayed herein is compiled from various sources, including BarclayHedge, and reports directly from the advisors. These performance figures should not be relied on independent of the individual advisor's disclosure document, which has important information regarding the method of calculation used, whether or not the performance includes proprietary results, and other important footnotes on the advisor's track record.

The programs listed here are a sub-set of the full list of programs able to be accessed by subscribing to the database and reflect programs we currently work with and/or are more familiar with.

Benchmark index performance is for the constituents of that index only, and does not represent the entire universe of possible investments within that asset class. And further, that there can be limitations and biases to indices such as survivorship, self reporting, and instant history. Individuals cannot invest in the index itself, and actual rates of return may be significantly different and more volatile than those of the index.

Managed futures accounts can subject to substantial charges for management and advisory fees. The numbers within this website include all such fees, but it may be necessary for those accounts that are subject to these charges to make substantial trading profits in the future to avoid depletion or exhaustion of their assets.

Investors interested in investing with a managed futures program (excepting those programs which are offered exclusively to qualified eligible persons as that term is defined by CFTC regulation 4.7) will be required to receive and sign off on a disclosure document in compliance with certain CFT rules The disclosure documents contains a complete description of the principal risk factors and each fee to be charged to your account by the CTA, as well as the composite performance of accounts under the CTA's management over at least the most recent five years. Investor interested in investing in any of the programs on this website are urged to carefully read these disclosure documents, including, but not limited to the performance information, before investing in any such programs.

Those investors who are qualified eligible persons as that term is defined by CFTC regulation 4.7 and interested in investing in a program exempt from having to provide a disclosure document and considered by the regulations to be sophisticated enough to understand the risks and be able to interpret the accuracy and completeness of any performance information on their own.

RCM receives a portion of the commodity brokerage commissions you pay in connection with your futures trading and/or a portion of the interest income (if any) earned on an account's assets. The listed manager may also pay RCM a portion of the fees they receive from accounts introduced to them by RCM.

Limitations on RCM Quintile + Star Rankings

The Quintile Rankings and RCM Star Rankings shown here are provided for informational purposes only. RCM does not guarantee the accuracy, timeliness or completeness of this information. The ranking methodology is proprietary and the results have not been audited or verified by an independent third party. Some CTAs may employ trading programs or strategies that are riskier than others. CTAs may manage customer accounts differently than their model results shown or make different trades in actual customer accounts versus their own accounts. Different CTAs are subject to different market conditions and risks that can significantly impact actual results. RCM and its affiliates receive compensation from some of the rated CTAs. Investors should perform their own due diligence before investing with any CTA. This ranking information should not be the sole basis for any investment decision.

See the full terms of use and risk disclaimer here.