April 17, 2014

Attain Capital

Like

It’s the always present question mid-size and start-up funds ask themselves day in and day out. Why do investors keep plowing money into the largest of the large hedge funds when the statistics have shown time and again that those large hedge funds tend to underperform their smaller counterparts. Alternatives research and analysis firm Preqin tackles the question with some hard data in their most recent piece: “What are Investors Looking For?”, showing that the small and mid-size hedge funds outperformed the largest funds by about 1.7% in 2013:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Preqin

One answer to the large versus medium/small debate given by some institutional investors we’ve talked to, highlights the deviation in returns, not the returns themselves, as the reason to choose a ‘brand name’ Billion Dollar+ hedge fund over a smaller upstart which may provide better performance. The logic is that while they may perform a little worse in terms of return – their worst case scenario is a lot less when choosing Goliath over David. This is the same reason we reach for the Kraft Macaroni and Cheese versus the generic brand, why all else being equal we go with American Airlines instead of Spirit, and so forth. It’s not all about saving money (or making more of it in case of hedge funds), it’s about having a sense of comfort as well.

But how much of this type of “comfort” are the biggest hedge funds really delivering? To dive deeper, we took a look at Preqin’s details on how the hedge fund performance in these different size groups was dispersed.

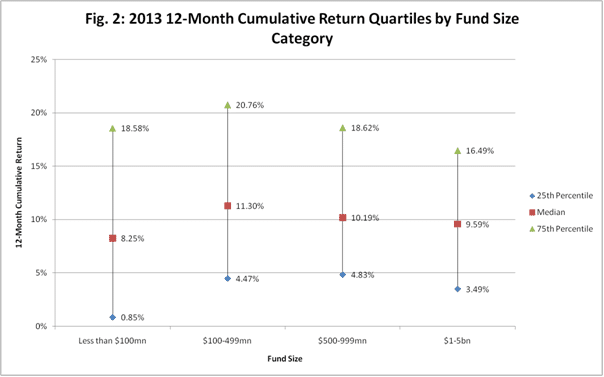

“Fig. 2 shows performance over 2013 according to the 25th percentile, median and 75th percentile values among each of the fund size categories, and the data shows that the top three-quarters of all fund groups achieved positive returns in 2013.”

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Preqin

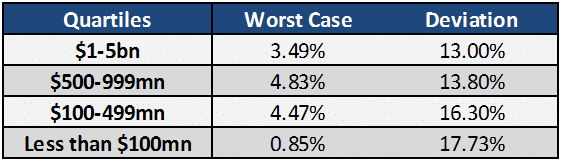

The invest with a behemoth logic would have us believe the dispersion of the small and medium size funds would be many times that of the large funds in order to make up for the underperformance of the behemoths, and that the so-called worst case scenario of the small and medium size funds would be much worse than the billion dollar big boys. But the stats show quite a different story (at least in 2013…), with the 25th percentile return for the big boys (the worst case) actually less than the 25th percentile average return for the small and medium-sized funds (the startup funds came in a distant fourth).

And what about that comfort level, the dispersion in the large hedge funds returns was indeed less, but not drastically so. Consider medium ($500-999mm) versus large funds ($1b+), where the medium had returns 1.13 times the large, yet a deviation less than that (just 1.06 times as large as the large), and a worst case scenario 1.38 times better. Now, one year doesn’t tell the whole story, and the data for the smallest hedge funds (under $100mm) support the comfort argument with higher deviation and a worse worst case scenario – but don’t throw the proverbial baby out with the bath water by lumping in small and medium-sized hedge funds with the startups. The small and medium-sized provided better returns, with similar comfort in 2013.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

PS – Preqin’s numbers got us thinking… and we’re working on a similar performance/deviation report for just the managed futures portion of the hedge fund space, look for it next week.

Disclaimer

The performance data displayed herein is compiled from various sources, including BarclayHedge, and reports directly from the advisors. These performance figures should not be relied on independent of the individual advisor's disclosure document, which has important information regarding the method of calculation used, whether or not the performance includes proprietary results, and other important footnotes on the advisor's track record.

The programs listed here are a sub-set of the full list of programs able to be accessed by subscribing to the database and reflect programs we currently work with and/or are more familiar with.

Benchmark index performance is for the constituents of that index only, and does not represent the entire universe of possible investments within that asset class. And further, that there can be limitations and biases to indices such as survivorship, self reporting, and instant history. Individuals cannot invest in the index itself, and actual rates of return may be significantly different and more volatile than those of the index.

Managed futures accounts can subject to substantial charges for management and advisory fees. The numbers within this website include all such fees, but it may be necessary for those accounts that are subject to these charges to make substantial trading profits in the future to avoid depletion or exhaustion of their assets.

Investors interested in investing with a managed futures program (excepting those programs which are offered exclusively to qualified eligible persons as that term is defined by CFTC regulation 4.7) will be required to receive and sign off on a disclosure document in compliance with certain CFT rules The disclosure documents contains a complete description of the principal risk factors and each fee to be charged to your account by the CTA, as well as the composite performance of accounts under the CTA's management over at least the most recent five years. Investor interested in investing in any of the programs on this website are urged to carefully read these disclosure documents, including, but not limited to the performance information, before investing in any such programs.

Those investors who are qualified eligible persons as that term is defined by CFTC regulation 4.7 and interested in investing in a program exempt from having to provide a disclosure document and considered by the regulations to be sophisticated enough to understand the risks and be able to interpret the accuracy and completeness of any performance information on their own.

RCM receives a portion of the commodity brokerage commissions you pay in connection with your futures trading and/or a portion of the interest income (if any) earned on an account's assets. The listed manager may also pay RCM a portion of the fees they receive from accounts introduced to them by RCM.

Limitations on RCM Quintile + Star Rankings

The Quintile Rankings and RCM Star Rankings shown here are provided for informational purposes only. RCM does not guarantee the accuracy, timeliness or completeness of this information. The ranking methodology is proprietary and the results have not been audited or verified by an independent third party. Some CTAs may employ trading programs or strategies that are riskier than others. CTAs may manage customer accounts differently than their model results shown or make different trades in actual customer accounts versus their own accounts. Different CTAs are subject to different market conditions and risks that can significantly impact actual results. RCM and its affiliates receive compensation from some of the rated CTAs. Investors should perform their own due diligence before investing with any CTA. This ranking information should not be the sole basis for any investment decision.

See the full terms of use and risk disclaimer here.

Disclaimer

The performance data displayed herein is compiled from various sources, including BarclayHedge, and reports directly from the advisors. These performance figures should not be relied on independent of the individual advisor's disclosure document, which has important information regarding the method of calculation used, whether or not the performance includes proprietary results, and other important footnotes on the advisor's track record.

The programs listed here are a sub-set of the full list of programs able to be accessed by subscribing to the database and reflect programs we currently work with and/or are more familiar with.

Benchmark index performance is for the constituents of that index only, and does not represent the entire universe of possible investments within that asset class. And further, that there can be limitations and biases to indices such as survivorship, self reporting, and instant history. Individuals cannot invest in the index itself, and actual rates of return may be significantly different and more volatile than those of the index.

Managed futures accounts can subject to substantial charges for management and advisory fees. The numbers within this website include all such fees, but it may be necessary for those accounts that are subject to these charges to make substantial trading profits in the future to avoid depletion or exhaustion of their assets.

Investors interested in investing with a managed futures program (excepting those programs which are offered exclusively to qualified eligible persons as that term is defined by CFTC regulation 4.7) will be required to receive and sign off on a disclosure document in compliance with certain CFT rules The disclosure documents contains a complete description of the principal risk factors and each fee to be charged to your account by the CTA, as well as the composite performance of accounts under the CTA's management over at least the most recent five years. Investor interested in investing in any of the programs on this website are urged to carefully read these disclosure documents, including, but not limited to the performance information, before investing in any such programs.

Those investors who are qualified eligible persons as that term is defined by CFTC regulation 4.7 and interested in investing in a program exempt from having to provide a disclosure document and considered by the regulations to be sophisticated enough to understand the risks and be able to interpret the accuracy and completeness of any performance information on their own.

RCM receives a portion of the commodity brokerage commissions you pay in connection with your futures trading and/or a portion of the interest income (if any) earned on an account's assets. The listed manager may also pay RCM a portion of the fees they receive from accounts introduced to them by RCM.

Limitations on RCM Quintile + Star Rankings

The Quintile Rankings and RCM Star Rankings shown here are provided for informational purposes only. RCM does not guarantee the accuracy, timeliness or completeness of this information. The ranking methodology is proprietary and the results have not been audited or verified by an independent third party. Some CTAs may employ trading programs or strategies that are riskier than others. CTAs may manage customer accounts differently than their model results shown or make different trades in actual customer accounts versus their own accounts. Different CTAs are subject to different market conditions and risks that can significantly impact actual results. RCM and its affiliates receive compensation from some of the rated CTAs. Investors should perform their own due diligence before investing with any CTA. This ranking information should not be the sole basis for any investment decision.

See the full terms of use and risk disclaimer here.