We covered back in November of 2012 how the reported total assets under management in the managed futures industry is a very deceiving number, based on it including the largest hedge fund in the world – $125 Billion + Bridgewater Associates. We found back then that the non-managed futures program Bridgewater represented a full 56% of the assets under management, with the largest actual managed futures program Winton representing another 8%, for a total of 64% of the reported investment in the asset class belonging to just two managers (one of which isn’t a managed futures investment).

Well – when talking about this little discrepancy in a recent conversation, the question was asked:

What does the growth look like without these two behemoths? Is the managed futures asset class even growing without considering Bridgewater and Winton? Great question!

The industry sure likes to tout the tremendous growth of assets under management (see CME here, Open Markets here); but is that growth really across the asset class, or centered on these two marvels of money raising.

It sounded like just the sort of thing we like to dig our hands into… and so we crunched the numbers in the BarclayHedge database to see what the real Ex. Winton/Bridgewater growth has looked like since the end of 2008. What did we find….

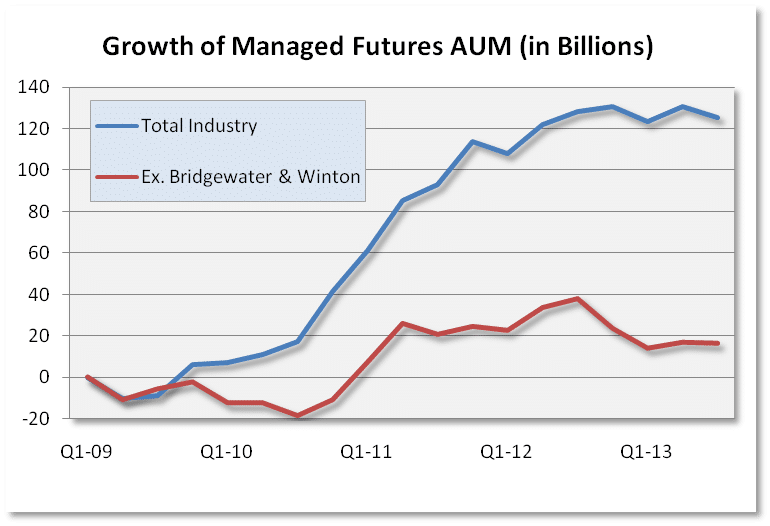

- 87% ($102b) of the $125 Billion in new money to managed futures since Dec. ’08 has come from Winton/Bridgewater.

- Just $16 Billion in new money has come into non Winton/Bridgewater managers since Dec. ’08.

- The asset class grew 60% since ’08

- The Ex- Winton/Bridgewater asset class grew just 15% since ’08

- The asset class is down -$3 Billion since June 2012

- The Ex- Winton/Bridgewater asset class is down -$24 Billion since June 2012

Managed Futures Assets Under Management Growth, both with and without Winton & Bridgewater.

(Disclaimer: Past performance is not necessarily indicative to future results)

(Disclaimer: Past performance is not necessarily indicative to future results)

Source: BarclayHedge Database

Here’s what the quarterly inflows/outflows look like if we remove Winton & Bridghewater, with a current 4 quarter average of a little more than -$5 Billion flowing out of the industry quarterly.

(Disclaimer: Past performance is not necessarily indicative to future results)

(Disclaimer: Past performance is not necessarily indicative to future results)

Source: BarclayHedge Database

Now, we’re not trying to cause (too much) trouble, but it occurs to us that those building out business plans, getting jobs in the industry, and trying to raise money would be a lot better served to see the real ex-Winton/Bridgewater numbers. We’ve met with more than a few managers who feel they are falling behind in their asset raising, but the reality is they may be doing quite well in light of $5 Billion a quarter currently moving out of managed futures.

As for that quarterly average dipping into negative territory – the contrarian in us loves to see it. We know we’ve been banging the “managed futures is due for a turn drum” for quite some time, but that has all been based on the cyclical nature of trends and those who follow them. The only thing stronger than those cycles, it seems, is investor’s penchant for getting in at the top and out at the bottom… To us, that means good things are coming for managed futures.

DISCLAIMER: The stats herein discuss the growth of assets under management both from new money invested and gains/losses on past money invested. It is not intended to portray performance of the asset class.