One of the many things we geek out about here at Attain, is the vast amount of opportunities available to crunch, dissect, and analyze the measure of risk each strategy offers. We’ve covered them all… Sharpe, Sortino, Mar & Calmar, Sterling (well almost all), and even reevaluated an alternative formula for Sortino. We’ve talked about ways to measure risk adjusted performance: how not all volatility is equal, and how it makes more sense to focus and care about the downside volatility more than the upside. Which led us to define and illustrate the two drawdown differences. Which leads us to perhaps one of the best named risk measurements out there: the Ulcer Index.

One of the many things we geek out about here at Attain, is the vast amount of opportunities available to crunch, dissect, and analyze the measure of risk each strategy offers. We’ve covered them all… Sharpe, Sortino, Mar & Calmar, Sterling (well almost all), and even reevaluated an alternative formula for Sortino. We’ve talked about ways to measure risk adjusted performance: how not all volatility is equal, and how it makes more sense to focus and care about the downside volatility more than the upside. Which led us to define and illustrate the two drawdown differences. Which leads us to perhaps one of the best named risk measurements out there: the Ulcer Index.

The Ulcer Index sort of pulls all of this together based on the theory that the pain an investor feels is not just how big, or how long, or how frequent losses are – but a combination of all of those factors. As such, the Ulcer Index measures the downside volatility, frequency of losses, magnitude of drawdown, and length of drawdown together into one number, measuring the overall pain an investor would have felt.

To provide a detailed explanation, we turn to Futures Magazine:

“The Ulcer Index…is calculated as the square root of the average squared drawdown number…

As can be seen by looking at the calculation, the Ulcer Index incorporates every single drawdown on every day of the history. A shallow drawdown that lasts a very long time will contribute a lot to the Ulcer Index because there will be a drawdown number for each of those days; a large drawdown will also be penalized a lot because of the squared factor…

The final number is a measure of the pain that was felt in the strategy over the period because it reflects all of the drawdown experience – not just the maximum drawdown but the frequency, magnitude and duration of drawdowns.”

Essentially, the Ulcer Index sort of normalizes the drawdown experience, where a small, but long drawdown may bring the same pain (have the same Ulcer Index number) as a big, but short drawdown. Like all such risk ratios – the numbers themselves don’t really mean anything, it’s how they relate to each other when measuring different performance profiles against one another.

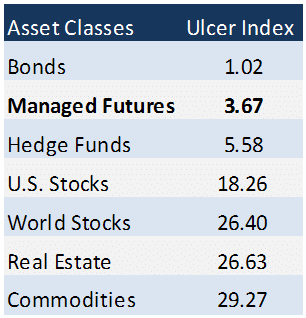

For example, we calculated the Ulcer Index for the various asset classes in our monthly asset class scoreboard over the past 10 years (Sept. 2003 – Sept. 2013) to see how each lines up in terms of investor pain.

(Disclaimer: Past performance is not necessarily indicative of futures results)

(Disclaimer: Past performance is not necessarily indicative of futures results)

Sources: Managed Futures = Barclay CTA Index, Bonds = Barclay Aggregate Bond Index

Hedge Funds =DJCS Broad Hedge Fund Index, U.S. Stocks = S&P 500,

World Stocks = MSCI ACWI ex US, Real Estate =iShares DJ Real Estate ETF (IYR)

Commodities = DJ USB Commodities Index

It’s good to see that even thought managed futures is in its worst drawdown since its inception (both length and depth), it still remains near the top of list for least amount of investor pain. Conversely, the often volatile and susceptible to huge (and long) drawdown commodity market has an Ulcer Index (a pain number) 10 times that of managed futures, while stocks and real estate aren’t that much better. So enjoy those stock market all time highs while they last, but beware the pain that comes with them.