By now, we in the managed futures world are used to the unwarranted assumptions about who we are and what we do. Some individuals see the word “finance,” and think stocks, then 2008 crisis; and therefore bad (which we’ve said over and over again, we have nothing to do with). Others have an idea of what futures are, but nine times out of ten that idea is ‘way too risky’.

In fact, just the other day, one of the new employees in the office recently had a conversation with their parents about investing in managed futures. As soon as the topic got brought up, a “no way in hell” guard immediately went up, and they responded, “I’ve never even considered it because I’ve always been told how risky it is.”

But the mantra ‘futures trading is risky’ isn’t just something that gets thrown about haphazardly – it’s the rules. Any futures broker registered with the National Futures Association is required to inform those they are prospecting that Futures Trading is indeed risky and that it isn’t suitable for everyone. You’ll see it all over our website as such:

“Derivative transactions, including futures, are complex and carry the risk of substantial losses. They are intended for sophisticated investors only and may not be suitable for everyone.”

So when we read Mike Dever’s Jackass Investing book with its 20 myths about investing, and came across Chapter 12 “Myth: Futures Trading is Risky”, we looked over our shoulders to see if the regulators would coming knocking on our doors. While those of us in the business of professional futures trading, aka Managed Futures, may think from time to time that futures trading is no more risky than the stock market, if done with proper risk management – we’re not about to put it in headlights as the chapter of a book!

But Mr. Dever was (respectfully) so bold… Is he in violation of the NFA rules? Is he downplaying the possibility of loss in futures trading? Is he misleading the public by saying futures trading is risky is a myth? Not in the least, in our opinion. As is often the case, the devil is in the details here:

First, Dever states right from the start that most individual futures traders…lose a lot of money.

“On average, people who trade in and out of mutual funds greatly underperform the return they would receive by leaving their money in the funds. And the more they trade, the more they lose. Compounding this losing behavior even further, the more leverage they employ, the greater their loss. And…most individual futures traders trade a lot and use a lot of leverage. The result: they lose a lot of money.”

Turns out, Dever is making a more nuanced point that futures trading is risky, but futures investing, via managed futures – need not be any more risky than the stock market or other investments. For our own regulatory protection – we’ll still tell you that there is the risk of substantial loss in both futures trading, and futures investing!

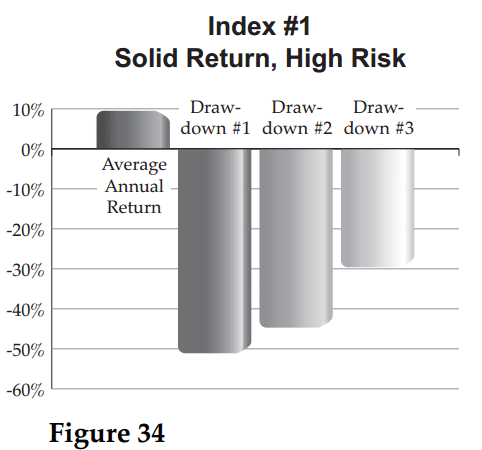

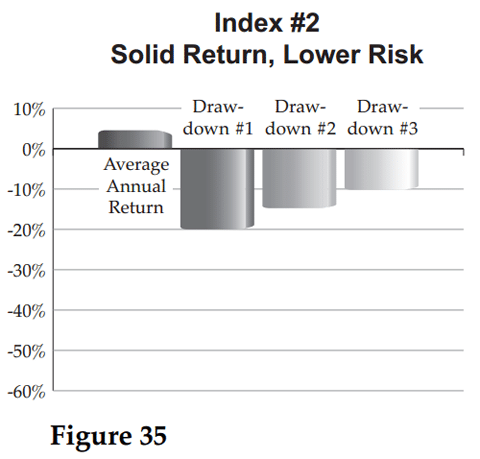

So the question the book explores isn’t really – is futures trading risky or not, but rather – is managed futures, as an asset class, more or less risky than stocks. To tackle this, Dever presents readers with a sort of blind taste test of two investment returns and risks, and asks which they would rather invest in.

(Disclaimer: Past performance is not necessarily indicative of future results)

So what’s your choice? Between 1987, and 2010, chart one had a 9.5% average annual returns, but experiencing losing periods in excess of 20%, and one losing period destroying half of the value. Chart two had the same (or a slightly higher) return, but with less exposure to risk. Who won the taste test, Coke or Pepsi? Turns out the first chart is the S&P 500, while the second chart is the BTOP 50 managed futures index.

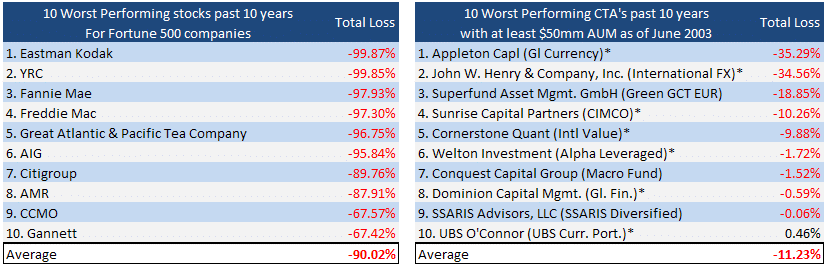

But, but, but… there may be a bigger dispersion of returns in the managed futures world versus stocks; there may be survivorship bias; there is a smoothing effect, and so on. Good points and we agree that it may be more telling to look not at the index performance over time, but compare actual managed futures investments and individual stocks. We did just that, selecting the worst 10 performing stocks in the S&P 500 over the past 10 years* to compare to the worst performing large managed futures programs (over $50 million in AUM) over the past 10 years*. If managed futures wins via the average (the indices) – what does it do in specific cases?

(Disclaimer: Past performance is not necessarily indicative of future results)

*To find the 10 worst performing stocks in the S&P 500 over the past decade (a tougher job than it seems), we gathered a list of stocks from a 2011 CNN Money article looking at the worst 20 stocks the past decade, then found the 10 worst performers from that list over the July 2003 to June 2013 period. The worst managed futures programs represent the worst performing programs which reported to the BarclayHedge datbase as of June 2003 and had over $50 million in assets at that time. It does not include any programs which came into existence after June 2003 and have since lost more than the amounts listed (when considering those results, the average of the 10 worst performers over the past 10 years, regardless of when they started is -34.39%).

* = A program stopped reporting to BarclayHedge database before 2013

There isn’t much of a comparison… Average the losses of the worst 10 stocks and we’re left with a -90.02% loss, compared to a -11.23% average loss across the worst managed futures programs over the past decade. And those were Fortune 500 companies – the biggest of the big, the blue chips, if you will.

So, yes futures trading is risky. But the point is – stocks are risky too. Very risky if you happen into one of the 10 worst performers. So are bonds. So is real estate. Investing is risky…. If there were no risk, it might be called something else (receiving?). So do your own research and ascertain for yourself what the risk looks like in the futures trading you are entertaining, and how that risk stacks up against more traditional investment methods. You may just uncover some myths of your own.

P.S. – Haven’t got your free copy of Jackass Investing yet? The author has agreed to provide a free e-book copy of the book to Attain readers.

P.P.S — Talk about putting money where his mouth is, Dever is the CEO of Brandywine Asset Management, rigorously maintaining and operating their Symphony Program which climbed an eye opening 11.27% in October {Disclaimer: Past performance is not necessarily indicative of future results}. The strength of this program lies in its multi-strategy approach with exposure to nearly all of the exchange traded futures markets that are available to US investors… a Ray Dalio of managed futures of sorts. Differentiators this month (as compared to trend followers) included long Aussie Dollar and South American Rand trades – a result of the basis arbitrage strategies; along with long lean hogs and mini NASDAQ from the fundamental strategy set. It wasn’t all roses though; Brandywine was on the wrong side of an Orange Juice trade this past month.