It’s been one amazing sell off in Crude Oil; so amazing we can’t stop writing about it. We’ve covered the long term picture of Crude, The Best Tweets from Crude’s Drop, How to Play a Bounce , and everyone else’s articles on crude. But we can’t stop staring at it… We’re the commodity focused moth to the proverbial flame.

But why is this sell off so amazing? What’s special about it?

1. The sheer velocity. How incredibly steep and unrelenting this down trend has been, for starters:

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Ed Conway

2. The numbers. If statistics are more of your thing – this highlight reel from the sell off which began last July might leave you in some technical amazement:

- Biggest Daily Drop = -10.53% on Black Friday (November 28th)

- Down 81 of 135 days since July 1 (60% of days), 41 of 71 days since Oct 1 (62% of days),

- Its average day has been down –0.60% since July 1, down -0.92% since Oct 1st.

- It’s fallen -1.78%, on average, when having a down day since July 1st, down -2.26% since Oct 1st.

- Down over -1% in a day 37% of the time (versus 22% in the previous 5 years)

- Down over -2% in a day 18% of the time (versus 9% in the previous 5 years)

- Down over -3% in a day 11% of the time (versus 3% in the previous 5 years)

- Current Price is 29% below the 50 Day Moving Average, 40% below the 100 day, 49% below the 200 day.

- Is the largest difference between current price and 100 day moving average in 6 years

3. The size of this market. Part of the amazement is because of how big of a market this is, especially in the financial world, where Oil is one of the most financialized things us humans have ever come up with, where Oil futures volume represents about 500 million barrels per day, about 5 times the 100 million barrels a day that are actually produced. Some say prices are were high because of this financialization. You be the judge on that one…

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

4. How wrong everyone was. A very, very big part of the amazement is how so many people could have completely missed this move, given how interconnected Crude is to the world economy. As a whole, the energy markets sold off big time… Crude Oil (-49%), Gasoline (-52%), and Heating Oil (-38%) in 2014. How could these markets, which account for the economies of whole countries like Russia and whole regions like the Middle East, which hundreds of billions of corporate revenues are based on, and which are traded by professional speculators, producers, and big commodity players day in and day out; lose over half their value in just six months? How could millions of people involved in Oil’s discovery, production, refining, accounting, drilling, transport, etc, etc. etc – not be waving warning flags back in June that prices were about 2x too high? How could hedge fund titans like John Paulson who correctly bet on the housing collapse in 2008 not foresee such a move in a market like Crude Oil when much smaller players were able to?

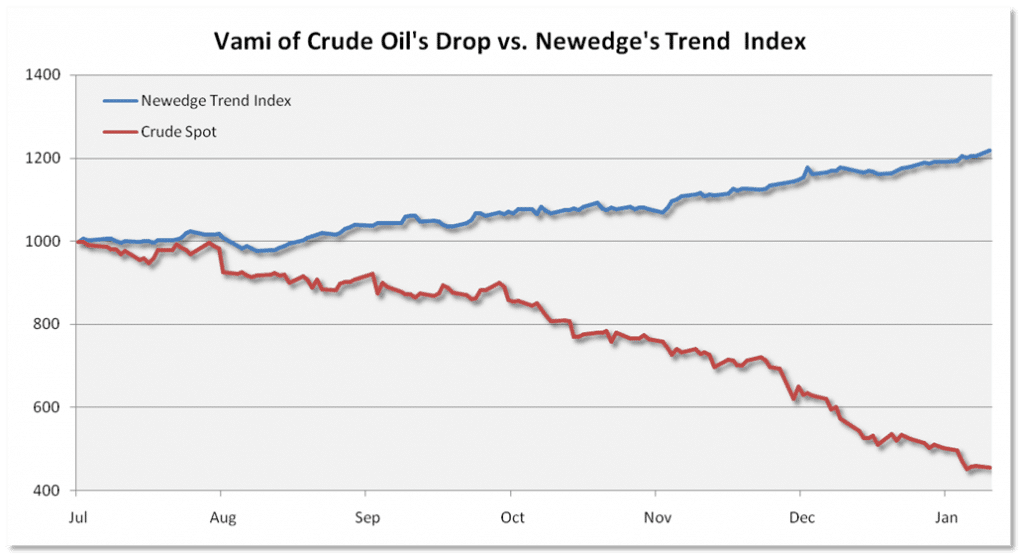

5. How not everyone was wrong. Of course, not everybody was “wrong” on Crude Oil. Systematic trend following strategies got it “right,” although the managers and quants who develop and run the models would likely never say they were wrong or right on a market. They wouldn’t boast about being right, or admit to being wrong; because they aren’t guessing or predicting where a market will go. They are following. So their success in Crude Oil wasn’t from correctly “calling” this trade over the past few months, it was from implementing a model and trading methodology which would capture such a move (in Crude, and Corn, and Euro Bunds, and dozens more) when and if it happened. It’s a little hard to wrap our heads around, but the success trend followers are enjoying right now isn’t from actions taken now – it’s from actions taken years ago. The reward isn’t from risks taken on this trade, it’s from risks taken on dozens of trades previously. Anyway, we’ll quit waxing philosophical… and show you just how similar (albeit in opposite directions) the trends in Crude and Trend Following performance has been over the past six months.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Source: Newedge

Data through Jan 12th, 2015

To learn more about Trend Followers, download our free Whitepaper of Trending Following. We break down how trend followers identify both when a trend begins and ends, and explain why not all trend followers are the same.