Apparently, the major financial media outlets decided they wanted to pretend to care about market indicators this month. We’re not talking Bollinger Bands or a Fibonacci Retracement or a Sharpe Ratio, but the most ominous market indicator out there, The Death Cross. It’s the market indicator that strikes fear into those who just heard that such an indicator exists.

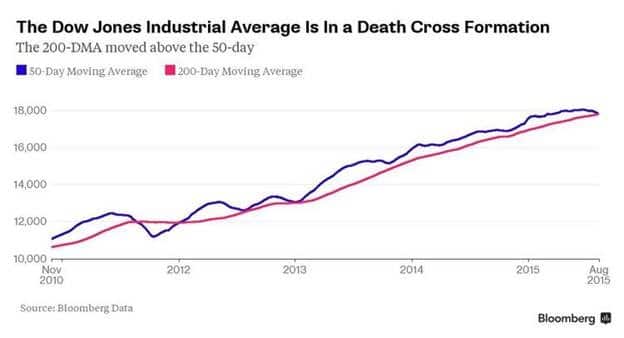

It just so happens that the Dow Jones Index crossed this fear striking indicator this month for the first time since 2011.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Bloomberg

Not to worry, stock market bulls – Guru Barry Ritholtz was hot on the job dispelling the idea that this is any reason to fear a market correction or downturn.

“Myths that become Wall Street rules of thumb have existed for as long as there have been trading desks. They are legion, they pop up regularly and most of the time they are terribly wrong. Woe to the unwary trader who relies on the urban legends to inform an outlook.”

What is the Death Cross?

Technically, it is when the average closing price of the past 50 days “crosses” below the average closing price of the past 200 days. When plotting these averages on a chart, as above, you get ‘moving averages’, which tick up and down each day when a new closing price is added to the average, and the price 51 or 201 days ago dropped from the average. The 50 day moving average moving below the 200 day moving average tells us the current environment is weaker than it has been, perhaps signaling a market top. The Golden Cross, conversely, is when the opposite happens, with the 50 day moving average crossing above the 200 day average.

Is the Death Cross a Premonition of Dark days Ahead?

Is this the moment we’ll all look back on as the time this already long in the tooth bull market ended? Is the Death Cross as deadly as its name suggests? According to Bespoke Investment Group, via Ritholtz, it turns out that this market idiom isn’t all that accurate of an indicator:

“Looking at the past 100 years, they wrote that “the index has tended to bounce back more often than not.” Shorter term (one to three months), however, these crosses have been followed by modest declines in the index.

How modest? The average decline is 0.17 percent during the next month and 1.52 percent the next three months. By comparison, Bespoke notes, during the past 100 years the Dow averages a 0.62 percent gain during all one-month periods and a 1.82 percent rise during all three-month periods.”

So it’s useless?

As a single indicator to dictate your entire asset allocation strategy, yes, it’s useless. As a tool to gauge market strength and inform your stock market exposure, it may have some value. But its real value is likely as a systematic trigger to signal the beginning of a trend, on top of which you layer risk control, position sizing, target returns, and all the rest.

How Trend Followers Use Market Indicators like the Death Cross:

Using different aspects of a market’s price relative to one another is one way to determine the start of a trend. These so called relative price models are less concerned with if a market has broken out of a range and more concerned with whether recent prices are stronger or weaker than past prices. A Simple Moving Average Cross Over method (like the Death and Golden Crosses) is the classic example of this, and it entails buying or selling when two moving averages of differing time periods (such as the 20-day and 100-day moving average, or 50/100, or 50/200) cross over one another. The shorter term moving average is used as the trigger, signaling a buy when it crosses above the longer term average, and a sell when crossing back below the average. On top of this buy and sell signal, a systematic trader will have a pre-determined percent of equity to risk on the trade, which will equate to an exit point designed to not risk more than that amount.

There’s Death Crosses (and Golden Crosses) weekly…

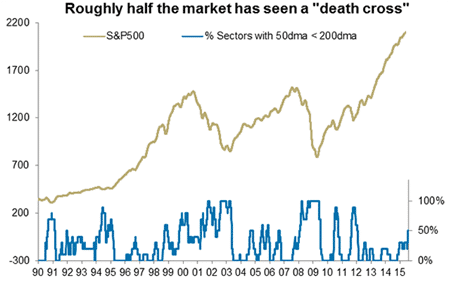

The thing the press ignores about the Death Cross is that you can apply mathematics to any market, and there are 100s of tradeable markets around the globe, meaning there are Death Crosses, and their opposite, likely any day of the week if looking across markets as varied as Cocoa, Japanese Bonds, Swiss Francs, and Crude Oil. Ritholtz sort of points this out, saying that using the Dow Jones as the overall market gauge can be dangerous as it isn’t a true presentation of the entire market; and we’ll add that it definitely isn’t a true presentation of all markets.

As proof of concept, we can see that more than half of the sectors in the S&P 500 currently have their 50 day MAs below the 200 day ones, showing there’s more than one way to find a Death Cross out there.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: AMP Capital

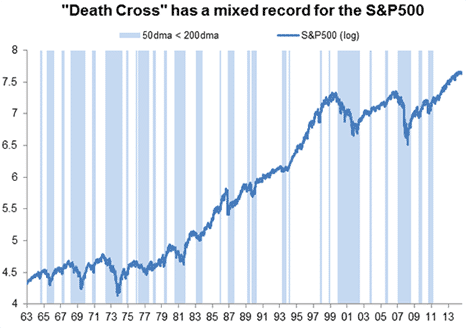

It’s not where you get in, it’s where you get out:

Which brings us to this chart showing all of the time (shaded blue) the S&P has been in a ‘death cross’, with the 50 day MA below the 200 day MA. Looks to us like about 35% of that chart is shaded blue, if not more. But more telling is where the price is when the blue changes back to white. You can see in periods like 1981 that the Death Cross was a good signal for calling a top (despite failing to call such a top in ’78 and ‘79), but that prices had come all the way back, and even above the prior level, before there was a Golden Cross telling you the trend was over…

That problem, more than anything else, is what makes the Death Cross “terribly wrong” in Ritholtz’s words. The Death Cross is ok at showing you when prices will turn lower, but give absolutely no information as to whether that turn lower will last 1 month or 4 years. It’s useless as a signal without overlaying risk control, position sizing, and a method (different than the Golden Cross) for getting out.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: AMP Capital

So, don’t go mortgaging your house to put on the mother of all short trades on this most recent Death Cross. But beware tossing it out with the bathwater as well. It has real value to systematic traders, when put to use across multiple markets and overlay other indicators and money management techniques on top of it. In the end, if you have stock exposure, you should probably, as Ritholtz suggests, just let stocks do what they’ll do, and not jump at reasons like this to lighten up. If you’re worried about the downside, the better approach is to instead look for non-correlated diversification in your portfolio, for when the Death Cross does become the next crisis.