November in Chicago has been nothing but normal, with 60 degree weather days (thanks to one of the strongest El Ninos on record) as we prepare ourselves for the most important food holiday of the year, Thanksgiving.

What you eat as a side dish depends greatly upon what region of the country you live, as FiveThirtyEight suggests. But despite the deviled eggs, squash, cornbread, or mac & cheese, no platter of food is more important than that of the turkey.

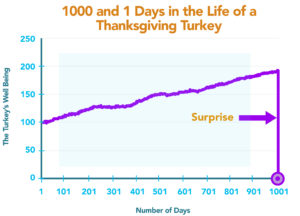

Each year, we’re reminded of the lovely chart of the life of said turkey from Nassim Taleb’s wonderful book, The Black Swan.

Taleb’s depicts “the good life” of a turkey, including round the clock care, all the food it can muster, developing a life of self-satisfaction, just so us humans can prepare the unfortunate creature for the not so pleasant surprise ending. The Turkey Surprise.

Now we’re not trying to lend advice on your eating habits, but can’t help but use this example in the investment realm. While it seems impossible to imagine this chart could be a stock market index tomorrow, next week, or next month – this chart is to remind those caught in stock market dream that anything could happen, at any moment, without notice; especially those selling volatility for a living.

Which brings us back to Mr. Turkey. The turkey sees 1000 days of small gains followed by one day of large losses, and we can’t help but think that reminds us of people who don’t do their due diligence for the right options managers in the alternative space.

The reason is option sellers are technically short volatility programs which on the whole make a living by risking a large amount to make a small amount. They have a large winning percentage where the large losses are very rare. If you’re a professional options trader, you know this sort of thing is going to happen, and prepare for it, by applying risk metrics developed to ensure that when the volatility hits, you enter a short drawdown, rather than being forced to shut down.

Now, professional option selling managers design their programs not to lose everything on a single day like the turkey; but they are betting against the occurrence of such a day, being set up to realize frequent but small gains in exchange for the risk of infrequent but very large losses (making them perhaps a distant cousin to the turkey).

In the meantime, Happy Thanksgiving to you and yours from the RCM Alternatives Team.