With each coming day, the Federal Reserve raising “rates” from the range of “0 – 0.25%” to “0.25% – 0.50%” on December 16th seems more and more probable. But those with billions of dollars on the line typically don’t like to make big bets on what seems likely. No, hedge funds, prop traders, and banks depending on the cost of money try for a bit more certainty.

Enter the Fed Funds futures contract, which allows those who care about such things to hedge their exposure to a hike in “rates.” Wait, isn’t that what 30 year bond futures are for? Or 10 yr notes? Or Eurodollars? Well, yes… But also no.

Remember, an interest rate hike comes in a few parts. Part one is the hike in the Fed Funds target rate, which is what the Fed essentially asks US banks to charge each other for borrowing money from each other through the federal reserve system. Part two is all the rest of the financial system taking that cue (either directly because the cost of their money went up, or indirectly because they can now charge more) and raising rates on the money they loan out.

Now here’s where it gets tricky, because while the financial system takes its cue from the fed funds rate, they won’t necessarily adjust all of their interest rates up/down by that same amount. Long term rates might stay the same, short term rates rise more than that or any combo in between. Which is all a very long winded way of saying there are some who need more granularity than the 30 yr bond or Eurodollars futures can offer. There’s those who need to have a direct hedge on the fed funds rate itself.

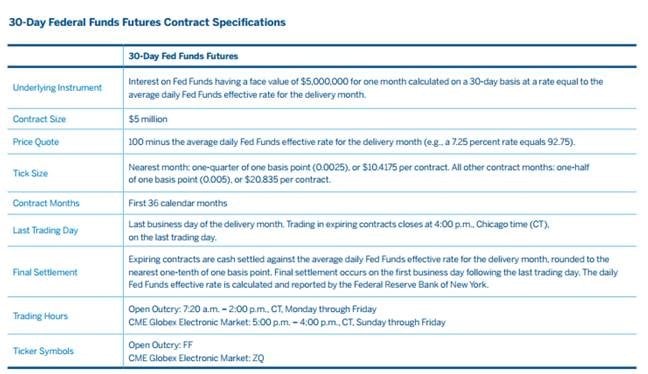

Fed Fund Futures

Here are the contract specs via the CME Group website.

Like the EuroDollar, the contract is quoted as 100 minus the interest rate, meaning the current December 2015 contract at 99.780 allows hedgers/speculators “lock in” a rate of 0.22% as if that’s was the average rate charged by banks loaning each other money through the federal reserve system.

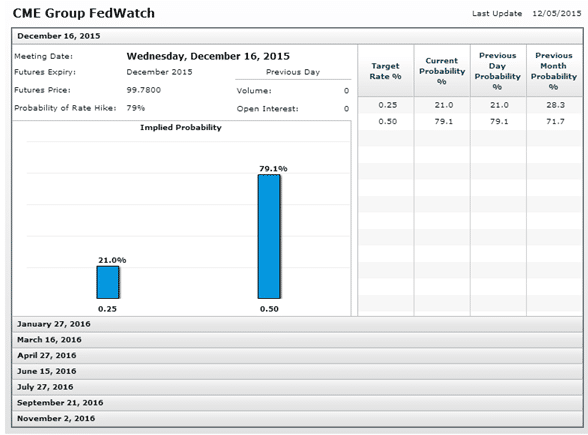

There’s a 79% chance?

Like a sports gambling system, you’ll notice in the months/weeks/days leading up to an FOMC meeting, article after article quoting a probability of the interest rates going up, like the over under of a football game. These articles aren’t actually using the price of the fed funds contract, but the CME FedWatch Tool. At the moment, the tool shows the probability of a December rate hike at 79.1%.

Chart Courtesy: CME FedWatch Tool

Chart Courtesy: CME FedWatch Tool

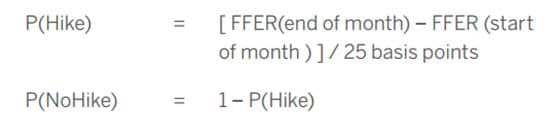

Where do they get that number from a futures price of 99.78? Behold the equation the CME uses to determine such a number in a month where there is a fed meeting.

This is more complicated than it looks – as it is really just taking the difference in the expected fed funds rate between the start and end of the month and dividing it by the assumed hike amount (25bps). For example, if the inferred rate from them fed funds futures was 1% at the start of the month and 1.25% at the end of, the difference would be 25bps (0.25%). Divide that’s by 25bps and you get 1 (25/25) or 100% chance of a 25bps rate hike.

Now, this is the inferred probability of a rate hike as expected by traders of the Fed Funds futures, but that’s a mouthful for reporters, who usually just throws out the percentage probability without providing context.

Volume

One might think that with media crazed focus on Janet Yellen, the fed, and raising interest rates, the fed funds contract would be as popular as the Emini S&P. But it turns out, it’s one of the least traded interest rate futures contracts. The Open Interest of fed funds in January stands at 203,000 whereas the 30 year note stands at around 507,000, suggesting there could be room for traders to grow in this space. With much anticipation on raising interest rates over the next couple of years, it will be interesting to see if this contract grows in interest (pun intended) as well.

Future Expectations

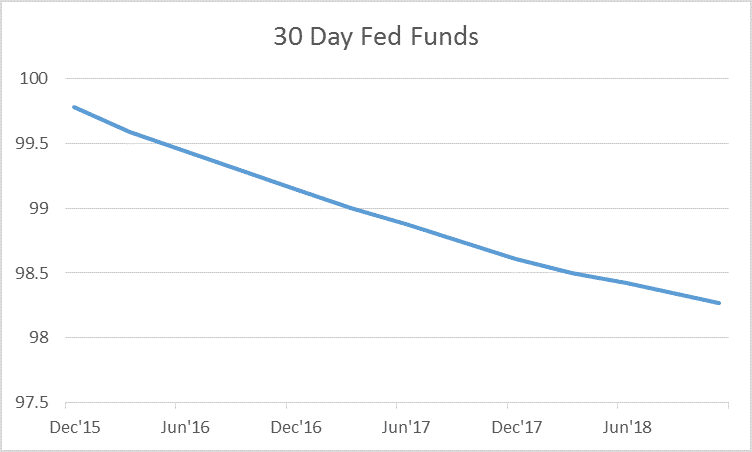

So where do traders see the Fed Funds rate going over the next few years? Up, up, and (not that far) away. You can see from the futures curve below that the price of Fed Funds futures contract is moving out over the next 36 months. Using this curve, it looks as though that by By November 2018, the rate is expected to rise to 1.73% (100 – 98.27).

Data Courtesy: Barchart

Data Courtesy: Barchart

Whether or not that happens or not is left to be seen. In the meantime, be on the lookout for an upcoming infographic on interest rates. Sign up here, to receive the latest posts and infographics delivered right to your inbox.