The sinking ship that is Valeant Pharmaceuticals continues to slowly slide into the ever darker depths, with the news this week that Bill Ackman (head of the Pershing Square Hedge Fund) “parted ways” with his old college friend that introduced him to the pharmaceutical company. The drug company -15% in the last week, but that’s nothing compared the -90% loss since July of 2015 which has pushed Ackman’s “Activist” hedge fund to its worst ever YTD loss – down an estimated -74% for the year {Disclaimer: Past performance is not necessarily indicative of future results}.

So how does a successful hedge fund manager like this can get so married to a trade? That’s the hallmark sign of a bad trader – someone who doesn’t cut their losses or worse yet, add on to losing positions. Bill Ackman is doing all of that and more, publically defending his very bad trade as he increases his stake at seemingly each downturn. To quote Bill Ackman himself on Valeant:

“Valeant has become toxic… We are on the brink of a catastrophe…You have previously made the mistake of waiting while Rome was burning. There is now a conflagration… We are on the brink of a tragedy.”

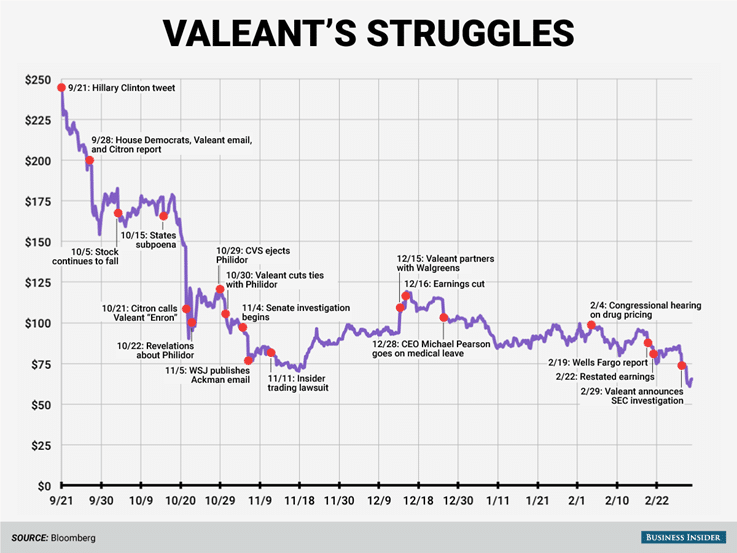

We don’t know if Valeant will ever return to the days a $250 a share, but clearly the market has a different take on Valeant than Ackman. And it may be a little troubling from a risk management standpoint to hear your manager saying we’re on the brink of tragedy. How can a hedge fund legend like Ackman look at the chart below and think I want to own Billions of dollars of this thing? How can such a successful investor become so married to a trade – to borrow an old floor trader saying.

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

Chart Courtesy: Business Insider

The answer lies in what type of investor he is. He picks the stocks he believes in. He’s a feelings investor. And when it doesn’t go his way – he goes ‘activist’ as they call it, pushing his way onto the board and pushing the company through the large ownership percentage to change this. He’s been nothing if not popular with this strategy – continuously in the news headlines. But this trade highlights the ENORMOUS differences between human based discretionary program such as Pershing Square and their systematic, computer based hedge fund brethren.

You would never see this with a well-designed systematic managed futures or global macro strategy. One, they typically don’t take big bets, instead opting for small bets on big outcomes. Two, they bend to be religious about getting out when they’re wrong. Religious is probably the wrong word, given it involves some hope and faith. It’s probably better to say they tend to be robotic about getting out of a losing trade. When market prices signal the end of whatever pattern or trend or move they were trying to capture, the rules of the system (the robot) automatically enters orders to exit the position. They don’t get “married” to the trade, they don’t do things like getting on boards to make the trade work out better. And there’s no soul searching on how great a trade it might be if you can just hold on a little longer. Nope, they just take the medicine and move on, choosing to live to fight another day.

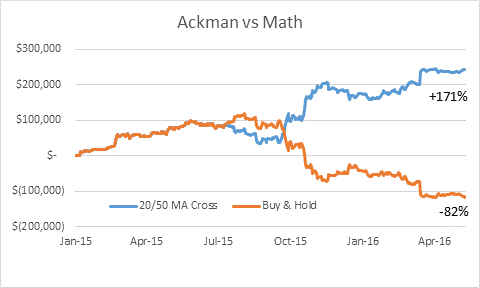

What’s more – a systematic process can bypass that biased mess between your investor ears and tell you when to go short a trade. We’re not just talking about getting out of a bad long trade, we’re talking how to make money on a falling investment, like Valeant. Here’s what the profit and loss from a super-simple trend following model looks like compared to Ackman’s buy and hold strategy with Valeant. (We used a 20/50 MA crossover, where the ‘investor’ was long the stock when the previous day’s 20 day moving average was higher than the 50 day moving average; and short the stock when the inverse was true – the 20 day MA below the 50 day MA).

(Disclaimer: Past performance is not necessarily indicative of future results)

(Disclaimer: Past performance is not necessarily indicative of future results)

The chart above is for educational and illustrative purposes only and does not represent trading in actual accounts.

Ackman’s spectacular losses on this trade will no doubt amplify the “hedge funds are bad” voices out there, but for those who care to dive into the weeds a bit – this is not a referendum on all hedge funds by any means. It is a referendum on the wisdom of entrusting a single ‘activist’ to get it right, day in and day out, without fail. It’s a referendum on going with a human instead of a human-controlled robot. Systematic programs sure have their own issues from time to time, but those pale in comparison to the risk of a manager marrying a trade.