Bloomberg’s out with a piece today showing the results from Credit Suisse’s “periodic survey of hedge fund investor sentiment.”

The headline you’ll be reading is that 84% of respondents redeemed from hedge funds in the first half of 2016. Wow, seems like a lot, until you read that only 9% don’t intend to re-deploy into hedge funds. So are they redeeming in the first place? They’ve got that covered in the below graphic, and it all boils down to that characteristic usually put onto “retail” traders – performance chasing.

62% of respondents redeemed because of performance related reasons, either with specific funds (53%) or the portfolio in general (9%). Here’s Bloomberg’s expanded look (it’s like they have a graphics department or something. 😉

Is this a Dumb move?

It seems none of these investors read Ben Carlson’s telling post on the so called “smart money” chasing performance. In his words:

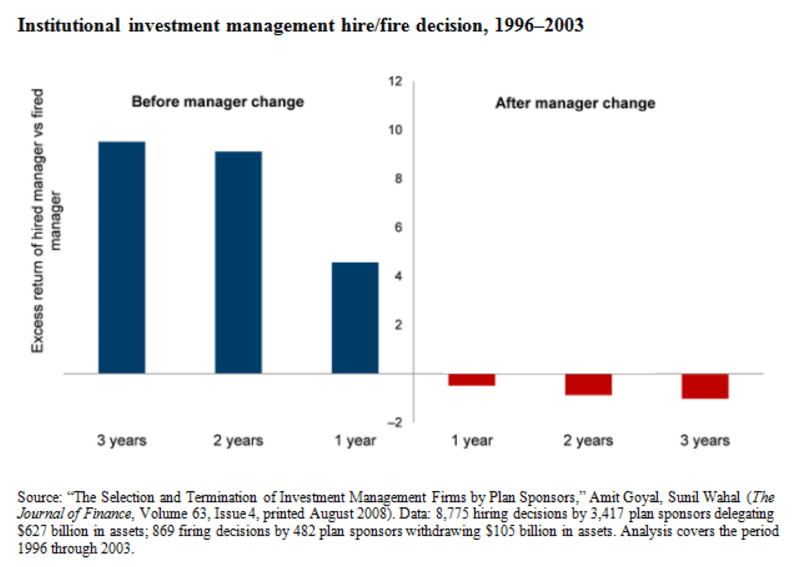

“Institutional investors are more than happy to chase performance — to their detriment — again and again.”

This chart shows how institutional investment committees continually make their investment manager decisions based on past performance, only to be disappointed by the subsequent returns once they invest. They hired managers that outperformed and fired managers that underperformed only to see those roles reverse after their investment moves were made.

The “smart” money has a nasty habit of buying winning funds after they’ve just won and selling losing funds after they’ve just lost. It’s something of an anti-value, anti-momentum approach where these large funds are always one step behind and fighting the last war.

There are plenty of great portfolio managers out there. But there probably aren’t enough asset allocators or organizations who can discern when to invest with a great portfolio manager and when it’s time to move on. This process is made even more difficult when a large committee has to come together to make group decisions.

So be careful next time you read about big fund of funds, family offices, pensions, or the like exiting a hedge fund. It’s probably not a sell signal on that fund at all. Of course past performance is not necessarily indicative of future results, but It’s probably a buy signal, given all investments proclivity to cycle between good and bad performance, and seemingly all investors habit of getting in at the highs and out at the lows.